The Corporate Sustainability Due Diligence Directive ("CSDDD") applies to certain European Union ("EU") companies and non-EU companies operating in the EU. It aims to improve corporate governance by integrating human rights and environmental risk management, including those arising from value chains, and mitigation processes with corporate strategies. This will require companies to adopt a risk-based due diligence policy to identify and assess existing or potentially adverse human rights and environmental impacts. Accordingly, significant financial penalties and civil liabilities are envisaged for companies that do not comply with obligations under the CSDDD. Applicable companies will also be required to adopt and implement a climate transition plan to limit global warming to 1.5 °C in line with the Paris Agreement and EU 2050 climate neutrality targets. Direct business partners of applicable companies, or those in their value chain, may also be affected by CSDDD obligations and asked for due diligence information.

Legislative Process for the Adoption of the CSDDD

The first draft of the CSDDD proposal was published by the European Commission in February 2022. After almost two years of negotiations, its revised text was provisionally adopted in December 2023. It was adopted by the Council of the European Union ("Council of the EU") in March 2024 and by the European Parliament on 24 April 2024. It is expected to enter into force 20 days after its publication in the Official Journal of the EU.

Which companies are affected?

The CSDDD applies to EU and non-EU companies that meet a certain threshold of turnover and number of employees.

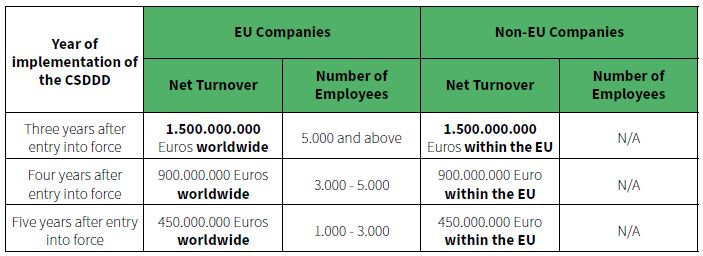

Implementation will be phased, with obligations arising between three to five years (dependant on company turnover, number of employees, and establishment in the EU) from the date the CSDDD enters into force.

For EU Companies with a worldwide net turnover above a certain threshold and a certain number of employees, the time when the CSDDD will enter into force differs. For Non-EU Companies, the net turnover within the EU is taken into account in this respect. For these Companies, the time of implementation of the CSDDD is explained in the table below.

(There is no minimum employee number threshold for non-EU companies.)

A parent company may apply for exemption from CCDDD obligations where:

- It can show it does not participate in managerial, operational or financial decisions affecting the Group or its operational subsidiaries.

- It designates an EU subsidiary to comply with CSDDD requirements on its behalf,

Obligations of Companies within the Scope of the CSDDD

(i) Human Rights and Environmental Due Diligence

Negative human rights and environmental impacts include forced labour, pollution and loss of biodiversity. The company must assess its own and its subsidiaries' activities (as well as those of business partners in its operational chain). This assessment should map chains of operations and evaluate where negative impacts are most likely to occur (consultations with shareholders will therefore play a critical role).

The CSDDD requires applicable companies to identify and, where necessary, prioritise, prevent, mitigate, reduce, cease, minimise and remediate actual and potentially adverse human rights and environmental impacts. Companies establish a risk-based due diligence policy by:

- Describing their due diligence approach.

- Defining the rules and principles to be followed by affiliates and business partners.

- Describing the processes in place to implement due diligence measures.

(ii) Climate Transition Plans

The CSDDD is responsible for ensuring that all applicable companies:

- Limit global warming to 1.5 °C in line with the Paris Agreement.

- Achieve zero greenhouse gas (GHG) emissions by 2050 (inclusive of the EU's 2030 and 2040 interim targets).

- Transition to a sustainable economy by achievement of said targets.

The transition plan will be updated annually and describe the company's progress towards meeting its targets.

(iii) Sanctions

- Fines: Non-complying companies may be fined up to 5% of their global turnover (enforced by individual EU Member States).

- Civil liability: Civil liability will arise where companies intentionally or negligently fail to prevent, mitigate, cease or minimise adverse human rights impacts. This liability is subject to a five-year limitation period.

- Exclusion from public procurement: EU Member States may consider CSDDD compliance as a factor in the award of public contracts and concessions (and as an environmental or social condition for the performance of these contracts).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.