TDS and TCS are widely used by the Government as a mechanism to collect taxes as and when transactions occur. This serves twofold purposes: On the one hand, taxes are recovered on a real-time basis as and when transactions occur, and on the other hand, it helps in tracking a person's various income streams.

Budget 2024 has brought some key changes to rules relating to tax deductions at source (TDS) and tax collection at source (TCS). The new norms are directed towards easing compliance provisions for businesses and aiming to ease the procedure of tax payments by taxpayers.

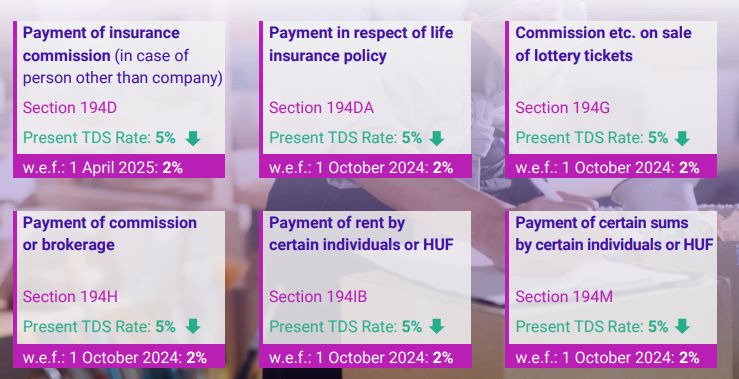

Amendments to TDS provisions

TDS on payment of certain sums by the e-commerce operator to the e-commerce participant

Currently, TDS is required to be done by an e-commerce operator while making payments to an e-commerce participant on the sale of goods at 1%. Sale or purchase of goods otherwise than on an e-commerce platform attracts TDS at 0.1% under Section 194Q. To align TDS on online sale of goods with physical sale/purchase of goods, it is proposed to reduce the TDS rate required by an e-commerce operator while making payments to an e-commerce participant to 0.1%.

TDS on payment of salary, remuneration, interest, bonus, or commission by partnership firm to partners

Presently, there is no provision for tax deduction at the source (TDS) on payment of salary, remuneration, interest, bonus, or commission to partners by the partnership firm. Budget 2024 has proposed to insert a new TDS Section 194T for payments to the partners by the partnership firm on aggregate amounts of more than INR 20,000 in the financial year. The applicable TDS rate will be 10%

The provisions of Section 194T of the Act will take effect from the 1 April 2025.

Amendment of provisions of TDS on sale of immovable property

Any person buying immovable property other than agricultural land from a resident should, at the time of credit or payment of such sum to the resident, deduct an amount equal to 1% of the sum or the stamp duty value of such property, whichever is higher

No deduction is required where the consideration and the stamp duty value are less than INR 5 million.

A tax position was adopted such that the term consideration mentioned in the section refers to each buyer's payment rather than the total consideration paid for the immovable property. No TDS was done if such individual payments were less than INR 5 million.

It has now been clarified that consideration refers to the total aggregate consideration for the property. If the same exceeds INR 5 million, TDS shall apply.

The amendments will take effect on 1 October 2024.

Excluding sums paid under Section 194J from Section 194C

It is clarified that any sum covered under the provisions of Section 194J – TDS on payment for professional fees and fees for technical services are excluded from Section 194C – TDS on Payments to contractors.

The amendment will take effect from 1 October 2024.

Amendments to TCS provisions

TCS under sub-section (1F) of Section 206C on notified goods

A seller of a motor vehicle on sale of motor vehicle exceeding INR 1 million is required to collect from the buyer a sum equal to 1% of the sale consideration. However, it has been observed that people with high net worth have increased expenditure on luxury goods. For proper tracking of such expenses and to widen and deepen the tax net, it is proposed to levy TCS on any other goods of value exceeding INR 1 million, as may be notified by the Central Government on this behalf. Such goods would be luxury goods.

The amendment will take effect from 1 January 2025.

Ease in claiming credit for TCS collected/TDS deducted by salaried employees

Section 192 of the Act provides for tax deduction at source on salary income.

Last year, the Government expanded the scope of TCS on many transactions, including LRS, tour packages, etc. TCS was not considered a tax credit while computing the TDS on salary income and was claimed as a tax refund in the income tax return. This also resulted in cash flow issues for individuals.

To avoid cash flow issues for the employees, the budget has proposed considering TCS while computing the TDS liability under salary itself.

Claiming credit for TCS of minor in the hands of parents

It has been proposed that the TCS of the minor shall only be allowed where the income of the minor is being clubbed with the parent.

The amendment will take effect from the 1 January 2025.

Procedural amendments

Alignment of interest rates for late payment to Government account of TCS

In case of late deduction of TDS, interest at the rate of 1% per month is levied, and in case of late payment/deposit of TDS to the Government, a higher interest rate of 1.5% is applicable.

However, it was noted that the rate of interest applicable for late collection/late deposit of TCS is not aligned with provisions of late deduction/ deposit of TDS. Thus, to align the rate of simple interest charged on failure to pay to the Government account after collection of tax, it is proposed to specify that simple interest for non-payment of tax collected at source to the Government account is to be increased from 1% to 1.5% for every month or part thereof on the amount of such tax from the date on which such tax was collected to the date on which such tax is actually paid.

The amendment will take effect from the 1 April 2025.

Extending the scope for lower deduction/ collection certificate of tax at source

There are instances where taxpayers incur losses, and due to tax deducted under Section 194Q of the Act, their funds are blocked. Moreover, the tax deducted has to be refunded in such cases. It is also stated that there is additional compliance as a seller liable for TCS needs to verify whether the buyer has deducted tax or not.

Therefore, to facilitate ease of doing business, it is proposed that a lower deduction certificate/ certificate for collection of taxes relating to TDS on the purchase of goods and TCS on the sale of goods may be obtained.

The amendments will take effect from the 1 October 2024.

Time limit to revise TDS returns and TDS assessments

There was no time limit specified to revise TDS returns earlier. It is proposed that TDS returns may now be revised with six years.

Likewise, it is proposed that TDS assessment under Section 201 shall be made within six years.

These proposed amendments are welcome as they give more clarity and certainty to assessments.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.