- within Family and Matrimonial, Government, Public Sector and Insolvency/Bankruptcy/Re-Structuring topic(s)

This article discusses the critical role of show cause notices ('SCNs') in India's Goods and Service Tax ('GST') framework, particularly how they notify individuals and businesses about potential tax issues and prompt them to explain or rectify these concerns. It explains that these notices are not just bureaucratic procedures but are essential tools for ensuring fairness in tax assessments. The introduction also explores the legal basis for issuing SCNs, particularly under scenarios where tax evasion is suspected, emphasizing their importance in maintaining the integrity of the tax system. By delving into these notices' procedural roles, the abstract sets the stage for a deeper discussion on pre-notice consultations, enhancing transparency and cooperation between tax authorities and taxpayers.

I. Introduction

Notice is a form of communication by government authorities to remind/caution the person to whom it has been addressed/issued about a legal proceeding. A notice may be defined as a legal notification required by law or agreement or imparted by operation of law as a result of some fact. A person can be said to have notice of a fact or condition if that person (i) has actual knowledge of it, (ii) has received information about it, (iii) has reason to know about it, or (iv) knows about a related fact, or (v) is considered as having been able to ascertain it by checking an official filing or recording1. More specifically, a show-cause notice ('SCN') is a notice that requires the recipient person to establish reasons (or to show the cause) as to why a certain legal consequence should not arise unto him.

The practice of issuing SCNs is prevalent in tax proceedings initiated by/before the Income Tax department, the Customs and Excise department, the GST department, inter alia, several other departments, which are primarily tasked with collecting and recovering taxes. Under the indirect taxation system, i.e., the GST regime, the GST department is statutorily empowered to issue SCNs against any person/business liable to pay tax under the Goods and Services Tax Act, 2017 ('Act').

Under the Act, the SCN, if not based on the assumption that the assessee has wilfully and voluntarily evaded tax, is issued under s. 73(1) of the Act. However, a tax demand emanating from a reasonable assumption that the assessee has wilfully resorted to tax evasion by reason of (i) fraud, (ii) wilful misstatement, or (iii) suppression of facts shall invoke the issuance of demand under the provisions of s. 74(1) of the Act.

Issuing an SCN before assessment and recovery of demand is a procedural mandate. However, this essay delves into the stage prior to an SCN and tries to analyse the meaning and purpose of a Pre-SCN, as outlined in the Central Goods and Services Tax Rules, 2017 (CGST Rules).

II. Background: Is it essential to consult the assessee before SCN?

Tax discrepancies identified by tax authorities, based on documentary or other evidence available to them, may or may not be accurate and sustainable. Sometimes, even a simple conversation with the assessee may resolve the issue on either side. Thus, the short answer to the above question is in the affirmative. A Pre-SCN consultation, if conducted and concluded in its essence and spirit, would have the following benefits:

- Increased tax recovery – Pre-SCN consultation, undertaken in true spirit, would promote the parties (i.e., the proper officer, the assessee, and maybe third parties also incidentally involved in the matter) primarily facing the tax dispute to have a direct and upfront dialogue furthered towards resolution. The quick resolution of disputes would result in increased recovery and better tax collection.

- Quick resolution of impending cases – to reiterate, promoting a dialogue between the aggrieved parties would lead to a resolution in most instances, especially if such dialogue is conducted in its earnest capacity. A single round of consultation could free the revenue department as well as the assessee of multiple years of tedious and never-ending litigation, which could otherwise depreciate the economies of the government exchequer.

- Avoiding litigation – the process helps avoid unnecessary litigation and saves time and resources for the assessee as well as revenue. It is well known that tax litigation, which goes through the Commissioner (Appeals), the Appellate Tribunal, the High Courts, and thereafter the Supreme Court, is one of the lengthiest and costliest litigations.

- Clarification of inadvertent mistakes – the assessee has an opportunity to clarify their position, bring in evidence and explanations, and rectify any inadvertent factual or legal mistake made by the proper officer.

In light of the above advantages, the procedural inconvenience and the lack of a forum or opportunity for the assessee before an SCN is issued against him, the Tax Administrative Reform Committee ('TARC'), under the leadership of Dr. Parthasarathi Shome, recommended providing for Pre-SCN consultation, besides other collaborative and solution-oriented mechanisms, for the amicable resolution of taxation issues. The purpose of such consultation was limited to bringing the revenue department and the assessee to a common, logical and legally profound agreement to settle the dispute and avoid unwarranted delays. The recommendations made by the TARC were implemented and made mandatory for all cases wherein the duty demand exceeded Rs. 50 lakhs or more, by the Central Board of Indirect Taxes and Customs ('CBIC'), vide circular dt. 21.12.2015.

Notably, though the Pre-SCN consultation requirement was embodied in indirect tax laws through an administrative circular/instruction issued by CBIC, it was not made a part of the law when the CGST Act was enacted, or the rules thereunder were notified. The Act and its rules only contemplated the department identifying a tax discrepancy, which would immediately lead to the issuance of an SCN without consultation with the assessee.

III. Consultation: Whether mandatory or discretionary?

The procedure for issuance of SCNs, tax demands and recovery of dues is enumerated under r. 142 of CGST Rules. CBIC's notification dt. 09.10.20192 amended this rule to insert a new sub-rule (1A), making 'pre-notice consultation' mandatory. The provision read as follows:

(1A) The proper officer shall, before service of notice to the person chargeable with tax, interest and penalty, under sub-section (1) of Section 73 or sub-section (1) of Section 74, as the case may be, shall communicate the details of any tax, interest and penalty as ascertained by the said officer, in Part A of Form GST DRC-01A.

However, the aforementioned mandatory provision was made discretionary by the CGST (Twelfth Amendment) Rules, 2020, notified vide Notification dt. 15.10.20203, whereby the word 'shall' be substituted with 'may'. Thus, by virtue of the twelfth amendment, a proper officer under GST is no longer mandated to undertake pre-notice consultation. The present provision reads as follows:

(1A) The proper officer may, before service of notice to the person chargeable with tax, interest and penalty, under sub-section (1) of Section 73 or sub-section (1) of Section 74, as the case may be, communicate the details of any tax, interest and penalty as ascertained by the said officer, in Part A of Form GST DRC-01A.

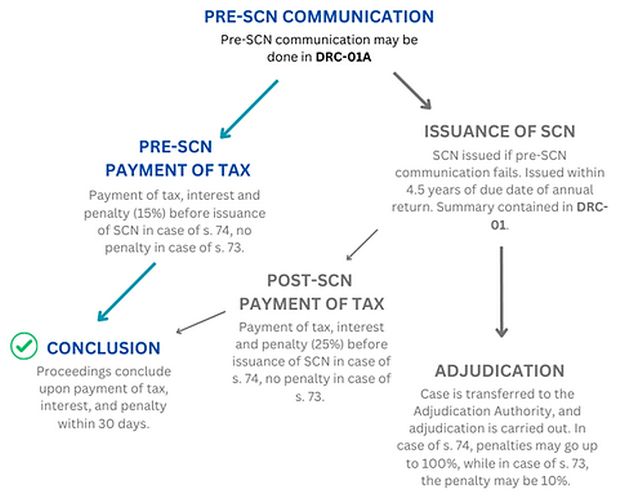

In cases where the Pre-SCN consultation is given to the assessee, a Form DRC-01A is issued by the proper officer, which contains details of the tax, interest, and penalty demanded. Most often, this form does not contain detailed allegations, the basis on which the tax, interest, and penalty are being demanded or the details about the evidence that the proper officer possesses against the assessee. Thus, this form can be called a brief demand and recovery notice issued by the proper officer. An assessee may choose to deposit the tax, interest, and penalty demanded from him vide this form, and the SCN would not be issued. The procedure is briefly diagrammed as follows:

IV. Pre-Notice Consultation in other laws

Notably, the above legal developments need to be chronologically contrasted with other pari materia taxing statutes, such as the Income-tax Act, 1961 ('IT Act') and the Customs Act, 1962 ('Customs Act'), which have also recently been amended to provide for similar pre-notice consultations.

S. 148A of the IT Act, inserted vide Finance Act, 2021, mandates upon the assessing officer ('AO') to conduct a preliminary enquiry and provide the assessee with an opportunity to be heard prior to issuing a notice under s. 148 of the IT Act. Subsequent upon the assessee having made his submissions under s. 148A of the IT Act, if unconvinced with the submissions made thereon, the AO may rightly initiate reassessment proceedings against the assessee. However, this requirement of pre-notice consultation is not required in serious circumstances such as search, seizure, or requisition of documents.

Similarly, under the Customs Act, Pre-SCN consultation was made mandatory by the Finance Act, 2018, which inserted a proviso to such effect. 28(1) of the Customs Act. The detailed provisions regarding such consultation were notified vide notification dt. 02.04.20184, whereby a proper officer issued a recovery notice under s. 28(1)(a) of the Customs Act was, as per the proviso appended to 28(1)(a), mandated to hold a pre-notice consultation with the assessee chargeable to pay duty. The aforementioned notification also provides a step-by-step procedure for conducting pre-notice consultation in a proper, time-bound manner to maximise its potential and output.

Thus, the general bend of the legislation is to provide for pre-notice consultations under various tax laws. However, in cases involving serious circumstances, these laws do not mandate such consultation, and the respective department may proceed to reopen the case or issue SCN immediately.

V. Practical consequences of making the process discretionary

Keeping in mind that in serious circumstances, it seems undesirable to the legislature to grant prior consultation, it would be apposite to analyse the amendment made to r. 142(1A) of the CGST Rules and appreciate if making the process discretionary has any practical consequence.

For cases involving serious circumstances (e.g., fraud, wilful misstatement, or suppression of facts under GST law), the opportunity for pre-notice consultation seems undesired by the legislature. Thus, the amendment to CGST Rules making the consultation discretionary is aligned with this thought. However, even in such cases, the proper officer may grant a pre-notice consultation.

For non-serious cases, however, the opportunity for pre-notice consultation is desirable, as is the case under other tax laws. Making the consultation discretionary in such cases also under GST law seems misaligned. However, it is to be noted that in such non-serious cases, the legal procedure under s. 73 of the CGST Act provides adequate opportunities without exposing the assessee to increased penalties or liabilities. Upon receipt of the SCN, the assessee may opt to pay the demand without any penalty levy. Subsequently, the assessee may also engage with the proper officer and pay the tax demand without any levy of penalty. Thus, on this basis, the amendment made to r. 142(1A) can be pragmatically justified.

It is pertinent to note that though the process has been made discretionary, courts have often reprimanded the revenue for not granting Pre-SCN consultation. For instance, in cases wherein the demand has been raised at the instance of an intelligence report, the department is not mandated to conduct a Pre-SCN consultation. However, in the case of Larsen & Turbo5, the Gujarat High Court held that Pre-SCN consultation cannot be denied to the assessee only on this basis. For this conclusion, the courts often rely on the purposive interpretation of the provisions, thus favouring the first principles of natural justice.

VI. Legal and practical issues

Ideologically, honest compliance with the Pre-SCN consultation procedure would have invariably proven to be mutually beneficial for both the assessee and the revenue, wherein the former would have been freed from years of departmental and procedural entanglement (by complying). The latter would have generated and recovered multitudes of revenue without exerting phenomenal effort (by not issuing SCNs and following the litigation thereafter). Such would have been an ideal set-up whereby the CBIC would have perfectly balanced out the interest of the revenue and the assessee. However, the scenario is contrary.

Often, the consultations are conducted as a mere formality. The Gujarat High Court has rightly pointed out in Dharamshil Agencies v. Union of India6 that the revenue officers are carrying out Pre-SCN consultations in an 'illusionary' manner. The issuance of notices is being done as a mere formality, whereby the proper officer is issuing SCNs after rejecting the prima facie evidence and submissions made by the assessee.

At times, Pre-SCN consultation notices are being sent to the assessee without really providing an adequate opportunity and granting a very short time to attend and respond. For instance, in the case of Dharamshil Agencies (supra), the Gujarat High Court, in furtherance of safeguarding the interest of the assessee, quashed the SCN issued by the department after the assessee failed to appear for a pre-notice consultation on a 14-hour notice. The Court reprimanded the revenue for conducting such flimsy and illusory pre-notice consultation, which utterly disregards its defined objective and purpose.

Next, the high-pitched nature of the tax, interest, and penalty amounts proposed in the Form DRC-01A forms being issued as a part of the Pre-SCN consultation procedure also defeats the very purpose of such consultation. The demands are high-pitched because of reasons including (i) lack of understanding on the part of the proper officer of the issue or contravention involved, (ii) the legal nature of the dispute, where the proper officer would take an interpretational stand that is completely pro-revenue, or (iii) lack of information or inadequate information about the correctness of the stand taken by the assessee, besides other reasons. Where the Pre-SCN consultation demand is high-pitched, it would seldom be agreeable to the assessee, resulting in complete failure of the process.

Besides the above, the Pre-SCN consultation process under the Indian GST law faces the following recurring and substantive issues:

- The law does not prescribe a standardized procedure for consultation (unlike other laws, such as customs and income-tax laws).

- The proper officer does not usually provide sufficient bases, documentation, and Form DRC-01A. This is because the officer wishes to keep the evidence unknown to the assessee, hedging for the scenario where the assessee does not opt into the consultation and rather chooses to litigate.

- The assessee does not always have adequate awareness about the consultation process and treats the Form DRC-01A notice as a demand notice without appreciating the benefits of penal consequences arising from opting into the consultation and settling the issue amicably.

VII. Conclusion

The Pre-SCN consultation process under GST law in India is a crucial mechanism designed to foster early resolution of tax disputes and reduce litigation. Despite its potential benefits, including increased tax recovery, quicker case resolution, and avoidance of lengthy legal battles, the process faces significant challenges. These challenges range from a lack of standardised procedures and inadequate communication from tax authorities to insufficient documentation and high-pitched demands that deter taxpayers from settling disputes amicably.

GST authorities can draw inspiration from other allied laws and make the process more restricted and controlled by not conducting pre-notice consultation in cases where the allegations are serious or grave in nature and/or the department has unwavering evidence establishing tax evasion by the assessee. Instead of the proper officer having blanket discretion regarding conducting a pre-notice consultation, the GST law can be molded to include certain exemptions under which conducting a Pre-SCN consultation would not be necessary.

For the Pre-SCN consultation process to achieve its intended objectives, it is imperative that both tax authorities and taxpayers engage in genuine dialogue. Authorities must provide clear, detailed notices and adequate time for taxpayers to respond, while taxpayers should be well-informed about the consultation process and its benefits. Addressing these issues will not only streamline the tax recovery process but also build greater trust and cooperation between the revenue department and taxpayers, ultimately contributing to a more efficient and fair tax system.

Footnotes

1. Black's Law Dictionary, 8th Ed., 2004, pp. 3368-3369.

2. Central Board of Indirect Taxes and Customs, Notification No. 49/2019 – Central Tax, dt. 09.10.2019 https://img-www.gstzen.in/pdfs/gst/notifications/cgst/2019/Notification-049-2019.pdf?_gl=1*sygtry*_ga*MTYzNzE1ODg5OS4xNzE5MDQyODEx*_ga_GB7WWP66TH*MTcxOTA0MjgxMS4xLjEuMTcxOTA0MzkzMC4wLjAuMA.

3. Central Board of Indirect Taxes and Customs, Notification No. 79/2020 – Central Tax, dt. 15.10.2020. https://img-www.gstzen.in/pdfs/gst/notifications/cgst/2020/Notification-079-2020.pdf?_gl=1*cus6od*_ga*MTYzNzE1ODg5OS4xNzE5MDQyODEx*_ga_GB7WWP66TH*MTcxOTA0NjIyMi4yLjEuMTcxOTA0NjI5MS4wLjAuMA.

4. Notification No. 29/2018 – Customs (N.T.) dt. 2nd April 2018.

5. L & T Hydrocarbon Engineering Ltd v. Union of India, 2022 TAXSCAN (HC) 246.

6. 2021 SCC OnLine Guj 3130.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.