The Federal Ministry of Finance (FMoF) has issued the Deduction of Tax at Source (Withholding) Regulations 2024 (hereafter referred to as "the Regulations"). The Regulations are aimed at providing clarity on the rules for the deduction of tax from payments made to taxable persons under these Acts: the Companies Income Tax Act (CITA), Capital Gains Tax Act (CGTA), Personal Income Tax Act (PITA), and Petroleum Profits Tax Act (PPTA).

The other key objectives of the Regulations are to reduce Withholding Tax (WHT) rates applicable to low-margin businesses, promote ease of tax compliance and administration, reduce arbitrage between corporate and noncorporate structures, reflect emerging issues and leverage global best practices. The Regulations complement the applicable statutory provisions and replace all prior rules regarding deductions at source, except for Pay-As-You-Earn (PAYE) tax.

The Regulations became effective from 1 July, 2024.

Key Highlights of the Regulations

1. Tax to be Deducted at Source

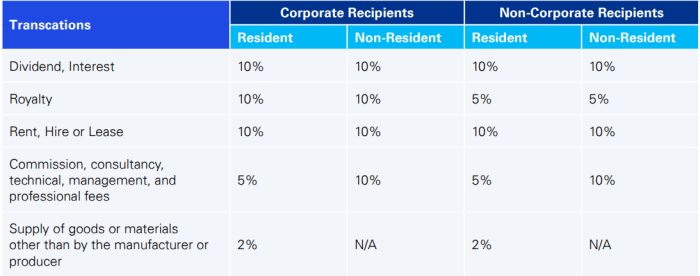

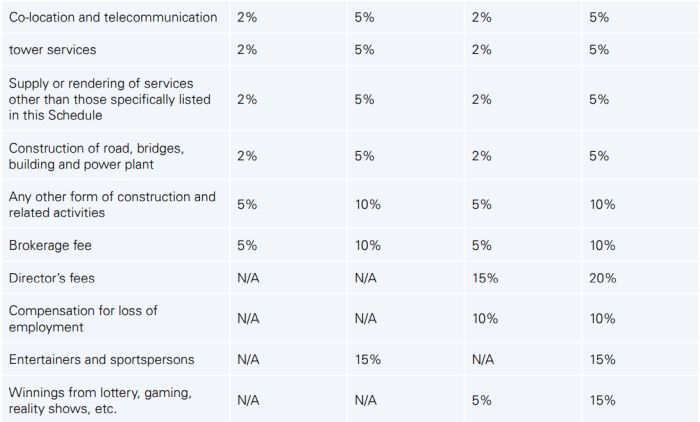

The Regulations establish new rates for the deduction of tax at source on various types of payments. Specifically, the first schedule to the Regulations stipulates the eligible transactions and applicable rates at which deductions should be made. It also specifies a distinct rate for corporate and non-corporate recipients, who are either residents or non-residents. Such transactions include dividend, interest, royalty, rent, co-location and telecommunication tower services, any form of construction and related activities, brokerage, winnings from lottery, gaming, and reality tv shows (effective 1 October 2024), compensation for loss of employment etc.

The applicable rates for eligible transactions are as follows:

However, reduced rates for avoidance of double taxation will continue to apply to an eligible recipient resident in a treaty country to the extent that the rates are contained in the treaty or protocol duly ratified by the National Assembly.

The Regulations also highlight the importance of having a Tax Identification Number (TIN). For transactions involving non-passive income, the applicable withholding rate will be doubled if the recipient does not possess a TIN.

2. Persons Required to make Deduction at Source

The Regulations specify the entities obligated to deduct tax at source. These entities include:

- A body, corporate or unincorporate, apart from an individual

- A Government, government ministry, department, or agency

- A statutory body

- A public authority

- Any other institution, organisation, establishment, or enterprise including those exempt from tax

- A payment agent on behalf of any person aforementioned

The Regulations, however, provide an exemption for small companies (those with annual turnover of less than N25m) from these deductions, provided that the relevant supplier has a valid TIN and the transaction value is ₦2,000,000 (two million naira) or less during the relevant calendar month.

3. Timing of Liability

The Regulations specify that the obligation to deduct tax at source on qualifying transactions will arise either when payment is made or when the amount due is otherwise settled. However, for related parties, the deduction will arise at the earlier of the time of payment or the recognition of the liability.

For non-resident persons, the amount deducted shall be the final tax on the transaction unless such non-resident persons have a taxable presence in Nigeria.

4. Remittance of Deductions at Source

Payments to the Federal Inland Revenue Service (FIRS) shall be made on or before the 21st day of the following month. For payments to States Internal Revenue Service (SIRs), the CGT and PAYE payments must be made by the 10th day of the following month, while other deductions must be paid by the 30th day following the month of payment.

Persons making the deductions are now required to submit returns to the relevant tax authority, using the template specified in the second schedule of the Regulations. Upon payment of the tax, the party making the deductions must issue receipts and a statement containing the information stipulated in Regulation 6. The template for receipts is provided in the third schedule to the Regulations.

5. Deductions to be Receipted

The Regulations provide that any entity making a tax deduction from a payment is now required to issue a receipt and a statement of remittance to the relevant tax authority. The statement must include the name, address, and TIN of the person from whom the deduction was made, the nature of the transaction, the gross amount payable, the amount deducted, and the month to which the payment relates.

The recipient of the deduction will need to submit the receipt to the relevant tax authority to claim the related tax credit. Where a receipt is issued but the deducted amount is not remitted, the beneficiary is entitled to a credit of the amount issued from the relevant tax authority. The unremitted amount will be treated as a liability of the deducting party and will be subject to applicable penalty and interest.

6. Penalties for Non-compliance

The Regulations state that anyone required to make a deduction at source, who either fails to do so or having deducted, fails to pay to the relevant tax authority on time, will face penalties as provided by Section 40 of the FIRS Establishment Act or Section 74 of PITA.

If the required deduction is not made but the amount is paid to the recipient, only an administrative penalty and one-off annual interest on the amount not deducted is due and payable. However, if an amount is deducted but not remitted, the deducted amount, along with an administrative penalty and annual interest, must be paid in accordance with the applicable legislation.

7. Exemptions

The Regulations provide for several exemptions from deduction at source. These exemptions include transactions such as across the counter transactions, payments to Real Estate Investment Trusts, specific securities transactions, manufactured goods, winnings from a game of chance or reality show designed to promote entrepreneurship, academics, technological or scientific innovations and specific fuel supplies. It is important to note that these exemptions do not constitute an exemption from the relevant income tax except as provided in the enabling law.

Commentaries

The issuance of the Regulations by the FMoF marks a significant step towards improving tax compliance and administration in Nigeria. By providing clear guidelines on tax deductions, the Regulations should simplify the tax process for businesses and promote the ease of doing business amidst the present economic realities. Through the clarity provided, the Regulations will also help reduce the possibility of unintentional noncompliance. This clarity is crucial for fostering a businessfriendly environment and ensuring that Nigeria remains competitive in the global market.

The Regulations emphasize the importance of having a TIN and set forth stringent penalties for non-compliance. This focus on TINs is expected to improve the accuracy of tax records and enhance the ability of tax authorities to track and collect taxes. By doubling the deduction rate for non-passive income if the recipient does not have a TIN, the Regulations incentivize businesses to ensure all deductions at source are properly documented and reported.

Most importantly, the Regulations provide the muchneeded clarity on the ambiguities surrounding the applicability of WHT to certain transactions, such as:

- where the taxpayer fails to deduct the tax due but has paid the supplier in full, it will not be required to account for the tax due again. However, such taxpayer will only pay the administrative penalty and one-off annual interest charge.

- where the beneficiary of the payment has the power to deduct the amount due, such as interest payable to banks by way of direct debit and commission payable to brokerage firms. Such transactions are specifically exempt.

- the obligation to deduct WHT, particularly for transactions not involving related parties, arises at the earlier of when the payment is made or when the liability due is otherwise settled. However, it is important to note that a payment will be considered otherwise settled when paid or resolved through means other than the original payment terms, such as forgiveness.

- domestic sale of crude oil and gas will be exempt from the WHT regime as these activities will constitute production of energy, which is classified as manufacturing under the Regulations.

- over the counter transactions that require payment to be made instantly by cash or through electronic means are exempt.

- the applicable WHT rate on commission, technical, management consultancy and professional fees is 5% for both resident corporates and non-corporates while it is 10% for non-resident corporates and noncorporates.

While the Regulations represent some progress towards simplifying the tax rules, there are still areas that could potentially discourage compliance. Some of these areas are discussed below:

- The success of any tax policy depends on many factors. One of these factors is public consultation and transparency. It is always important that governments engage with stakeholders in a transparent and constructive manner to obtain broad perspectives on issues, address their concerns and seek feedback to improve tax governance and accountability. Such engagements will help to manage expectations and gain support for the policy. Surprisingly, there was no such engagement with respect to these important Regulations.

- One key objective of the Regulations is to simplify tax rules, processes and enhance voluntary compliance. It then begs the question why the person obligated to withhold the tax is now required to issue a receipt for the amount withheld. In our opinion, this requirement is unnecessary as it introduces administrative inconvenience, bureaucratic processes and red tape. All that is required for the beneficiary to claim the related tax credit is to show evidence that a deduction has been made from the payment due, irrespective of whether the deduction has been remitted to the relevant tax authorities.

- We note the intention of government to apply different WHT rates to residents and non-residents. In as much as this practice is common in many countries, the application in some instances may cause unnecessary ambiguity and confusion. For instance, there is a different WHT rate for construction of roads, bridges, buildings, power plants and other forms of construction. However, the question is how can a non-resident taxpayer be involved in such activities without triggering tax residence in the country? Such activities, by their nature, will trigger fixed base in Nigeria and make the contractor resident for tax purposes. Furthermore, Regulation 8 (1) (l) provides that 'winnings from a game of chance or reality show with contents designed exclusively to promote entrepreneurship, academics, technological or scientific innovation' are exempt from the WHT regime. This suggests that any reality show that does not meet any of the four specified criteria would be subject to WHT. A reality show, like Big Brother, will fall under the latter category as it only provides a platform for participants to showcase their personalities, strategies and survival skills. There is nothing entrepreneurial, academic or scientific about the show. The question is whether this is the intention of the Regulation. We do not think so and, therefore, suggest that the aspect of the Regulation after 'reality show' be deleted to ensure clarity.

Overall, the Regulations are a welcome development as they align with leading practices and address some of the key issues in Nigeria's WHT compliance space. However, it is important that the Regulations be gazetted to provide the necessary legal framework. It, therefore, becomes incumbent upon government to issue a clarification that the Regulations will only become effective three (3) months after being gazetted to give taxpayers the opportunity to adapt their accounting /reporting systems, train personnel and establish new procedures. Moreover, it will provide ample room for government to correct and address the concerns discussed above.

The opinion expressed in this article is solely personal and does not represent the views of any organization or association to which the authors belong.