Read our latest insights into the U.S. private equity market. We cover monthly deal activity and size, fundraising, exits, leveraged loans, and a look ahead.

Key Takeaways from June

- Deal Activity: In the first half of 2024, deal count is tracking down ~13% compared to H1 2023, but it is up 6% compared to the same period last year. Deal count and value both fell in the second quarter compared to Q1, while June deal activity fell to the lowest monthly levels since mid-2020.

- Valuations: The average LBO purchase price multiple ticked up to 11.1x in H1 2024, but it remains below historical averages.

- Dealmaking Outlook: Deal pipelines are starting to refill and dealmakers are expecting a rebound in deal activity to continue throughout the second half of the year.

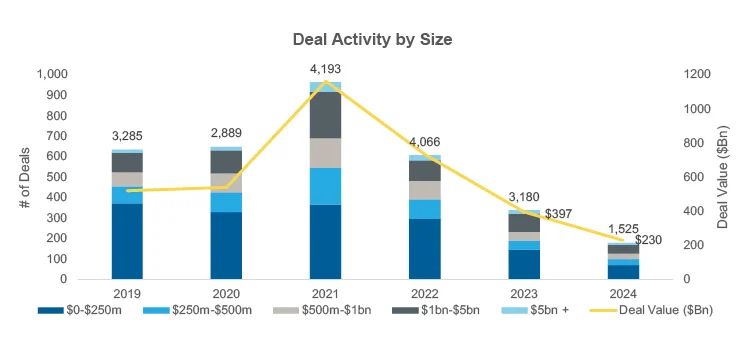

U.S. PE Deal Activity

- Decrease in activity: Q2 2024 U.S. PE deal activity dropped by ~22% QoQ and ~19% compared to Q2 2023. June deal activity fell by ~18% MoM and had the lowest number of deals in a month since May 2020

- Deal count and value diverge: H1 '24 deal count is tracking down 13% compared to H1 '23, while deal value increased by ~9% as average PE deal sizes are increasing

- Dealmakers are optimistic: Dealmakers expect strong M&A activity throughout the second half of the year, with H1 '24 deal counts up 6% compared to H2 '23

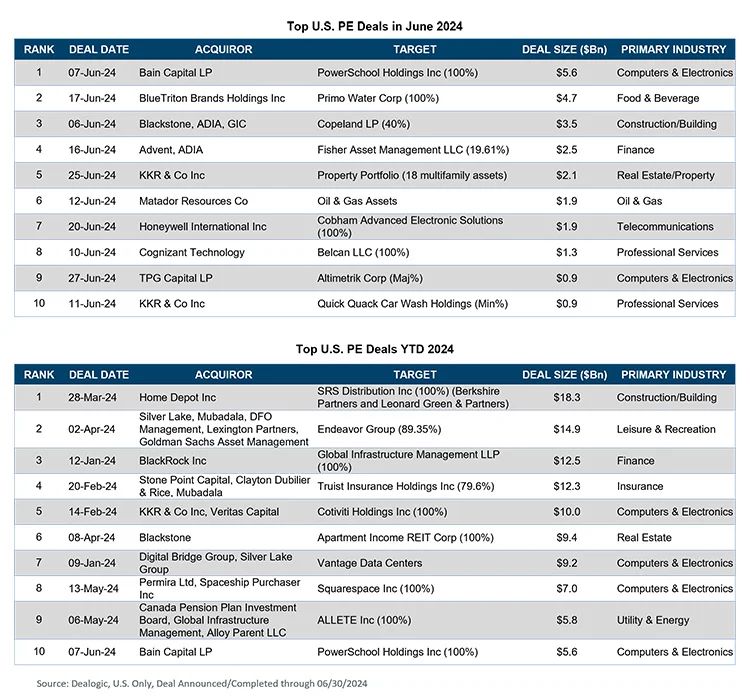

Top U.S. PE Deals by Deal Size

- Largest June 2024 deal: Bain Capital's $5.6 billion take private of PowerSchool was the largest deal in June and 10th largest deal YTD

- YTD stats: There have been 53 deals of $1

billion+ in 2024, down 4% from the same period in 2023, and 11

deals of $5 billion+, outpacing the same period last year by

22%

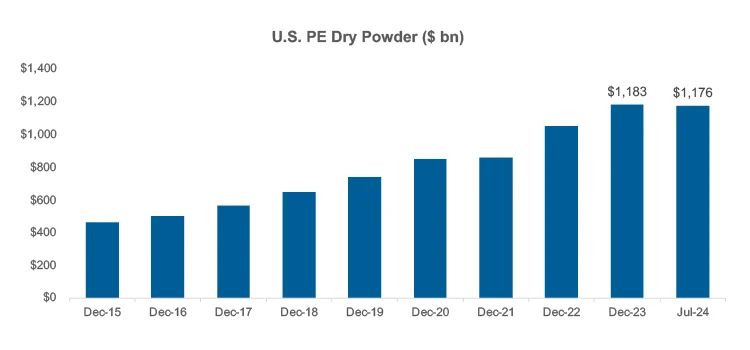

PE Dry Powder & Fundraising Trends

- Elevated dry powder: Dry powder has inched down over the last two months but remains over $1.1 trillion

- Weak fundraising: Q2 2024 saw a slight uptick in the number of funds closed and capital raised compared to the historically low levels seen in Q1, but 2024 is tracking far below 2023 levels

- Fundraising dynamics: A decreasing number of funds are closing as LPs are focusing new commitments on a subset of large and established managers

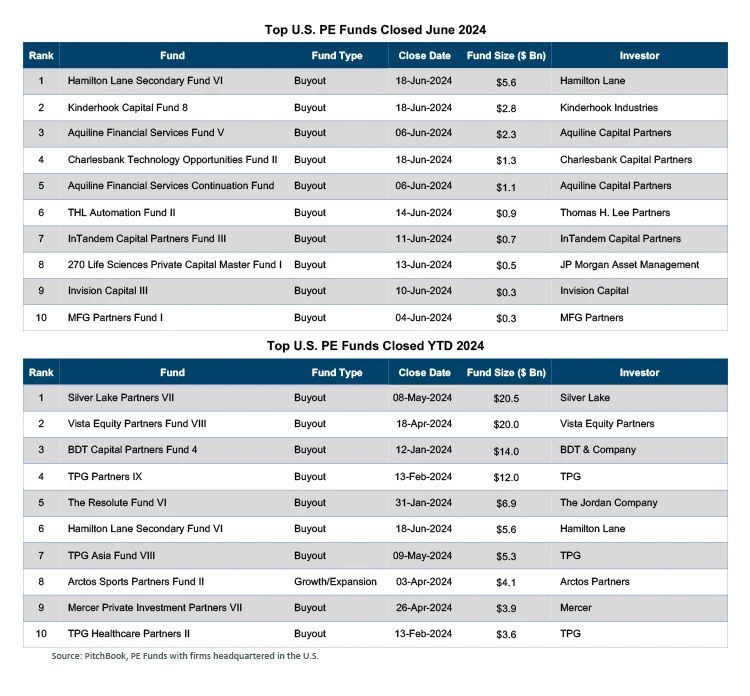

Top U.S. PE Funds Raised by Size

- Largest June 2024 fund: Hamilton Lane closed its largest secondary fund to date at $5.6 billion, exceeding its $5 billion target—secondaries remain an attractive strategy for investors

- Total June fund stats: 15 funds of $100 million+ and 8 funds of $500 million+ closed in June

PE Deal Multiples & Exit Activity

- LBO purchase price multiples tick up: The average EV / EBITDA multiple for LBO deals ticked up to 11.1x in H1 2024, but remains below the five-year average of 11.4x

- Exit activity shows signs of recovery: H1 2024

saw a pickup in exit activity compared to both H2 2023 and H1 2023,

indicating a positive sign for the industry

- Pressure to exit: Firms continue to face

pressure to return investor capital; the industry may see more

forced selling if deal activity doesn't naturally drive up

exits in the coming months

U.S. Leveraged Loan Issuance

- Strong quarterly issuance levels: $404 billion of leveraged loans were issued in Q2 2024, up 83% from $221 billion issued in Q2 2023; H1 2024 issuance was up 71% compared to H1 2023

- High institutional volume: Q2 2024 issuance was split between $145 billion of pro-rata volume, down 9% YoY, and $259 billion of institutional volume, up 316% YoY

A Look Ahead

- Midyear check-in: Many of the macroeconomic and market trends from 2023 have carried over through the first half of this year, and the private equity industry continues to work through the challenges created by the ongoing disrupted flow of capital

- Dealmaking recovery: Signs are creating optimism around a rebound in deal activity throughout the second half of year, including stable macroeconomic conditions, high levels of dry powder and an expected rate cut

- Opportune time for investors in secondaries:

The current exit environment continues to provide secondaries

investors the opportunity to step in and provide much needed

liquidity solutions

- There remains a large disparity between capital available for GP-led secondaries and the amount needed to support expected distributions, leaving firms with capital to invest in secondary solutions in a strong position

- Getting creative with distributions: Firms are relying on alternative methods to distribute capital back to investors, while traditional exit activity remains muted, such as partial asset sales, continuation funds, dividend recaps and NAV loans

- Stabilizing valuations: While gaps persist

between bid and ask prices and multiples remain below historical

averages, entry multiples are not expected to drop materially

lower

- Lower entry multiples may act as a headwind for future returns as it is more difficult for firms to achieve multiple expansion in high interest rate environments

- IPO market falls short of expectations: The strong growth experienced by public equities this year has not translated into the large IPO comeback investors were hoping for

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.