On 22 May, the Prime Minister made a statement confirming a UK general election on 4 July. The Conservative Party and the Labour Party (along with a number of the UK's other political parties) have now published their election manifestos. The manifestos contain few surprises, with most (if not all) policies having been well-trailed in recent weeks and months.

The Conservative manifesto commits to a number of tax cuts, including a further 2% reduction to employee national insurance rates and the abolition of self-employed national insurance entirely, as well as a proposal to protect the state pension from income tax by increasing the personal allowance of pensioners, with such cuts being funded by savings on welfare spending and revenue raised from tackling tax avoidance and evasion. Increases to income tax, VAT, capital gains tax, SDLT and corporation tax rates are also ruled out.

The Labour manifesto emphasises the Party's commitment not to "increase taxes on working people", with a pledge not to raise national insurance, income tax, VAT or corporation tax rates. Funding for schools and the NHS is to be found from implementing Labour's well-publicised policies, including the abolition of the "non-dom" regime, the imposition of VAT on private school fees and the closure of the carried interest "loophole", with the manifesto pledging to "begin to put these policies in place from day one of a Labour government". The topic of capital gains tax is conspicuously absent from the Labour manifesto – since its publication, Sir Keir Starmer has ruled out imposing capital gains tax on individuals' main homes; however, entrepreneurs and investors may remain concerned about other reforms to this tax.

We comment below in further detail on the key proposals affecting private clients.

Income tax

The current position

Income and dividend tax rates for the 2024/25 tax year are as follows.

In his 2022 Autumn Statement, the Chancellor announced the freezing or reduction of certain income tax thresholds and allowances. These plans were unchanged by subsequent fiscal events, meaning that:

- the income tax personal allowance (the amount of income an individual can receive free of tax – tapered for individuals with income above £100,000 and not available for non-UK domiciled individuals claiming the remittance basis of taxation) is fixed at its current level of £12,570 until April 2028;

- the higher rate threshold (the level of income above which the higher rate of 40% is charged – currently £37,700 plus the personal allowance, if available) is also fixed at its current level until April 2028;

- the additional rate threshold (the level of income at which the 45% rate starts to apply) will remain at £125,140 until April 2028; and

- the dividend allowance (the tax-free allowance for dividend income) was halved from £1,000 to £500 from April 2024.

What might a new government do?

In its 2019 manifesto, the Labour Party (led at that time by Jeremy Corbyn) promised to increase income tax rates for those earning more than £80,000 to 45%, and to introduce a new "super-rich" rate of 50% for those with an income of more than £125,000. One of Sir Keir Starmer's key pledges in his 2020 leadership campaign was also to "increase income tax for the top 5% of earners". More recently, however, the Labour Party has moved away from this policy. The Party's 2024 manifesto acknowledges that the tax burden is at "a 70-year high" and promises to ensure that "taxes on working people are kept as low as possible", with a commitment not to "increase...the basic, higher, or additional rates of income tax..."

In the run-up to the 2024 Spring Budget, it was rumoured that the Government would announce a cut to the basic rate of income tax or raise the higher rate threshold. However, no income tax changes were announced and, as set out above, the basic rate currently remains at 20% and the higher rate threshold remains frozen. The Conservative Party's 2024 manifesto does not contain any promises to cut income tax rates; however, it does confirm that the Conservative Party will "not raise the rate of income tax". It also proposes a new "Triple Lock Plus" for pensions, whereby both the state pension and the income tax personal allowance for pensioners will always rise with the highest of inflation, earnings or 2.5% (thereby ensuring that the state pension does not become subject to income tax).

Note, however, that other revenue-raising measures such as, for example, lowering the additional rate threshold again to bring more taxpayers into the 45% rate, have not been ruled out by either Party and therefore remain possible.

National insurance

The current position

Both the 2023 Autumn Statement and the 2024 Spring Budget announced cuts to national insurance rates. This means that, from 6 April 2024:

- the main rate of employee primary class 1 NICs dropped to 8%;

- the main rate of self-employed class 4 NICs fell to 6%; and

- compulsory class 2 NICs were abolished.

What might a new government do?

Having confirmed its support for the 2024 Spring Budget's national insurance rate cuts, it is perhaps unsurprising that Labour's manifesto includes a commitment not to raise national insurance rates. Since the publication of the Labour manifesto, a dossier, setting out a number of proposals for tax rises and produced by the party's Tribune group – of which Sir Keir Starmer is a member – was leaked to the media, and it is reported to include proposals to extend national insurance to all sources of income and to working pensioners; however, Labour have stated that "none of this is Labour policy" and that the document had been rejected.

The Conservative manifesto notes the Conservative Party's "long-term ambition...to keep cutting National Insurance until it's gone" and, as a first step towards this, commits to reducing employee NICs by a further 2% (to 6%) by April 2027, as well as abolishing self-employed class 4 NICs entirely by the end of the next Parliament.

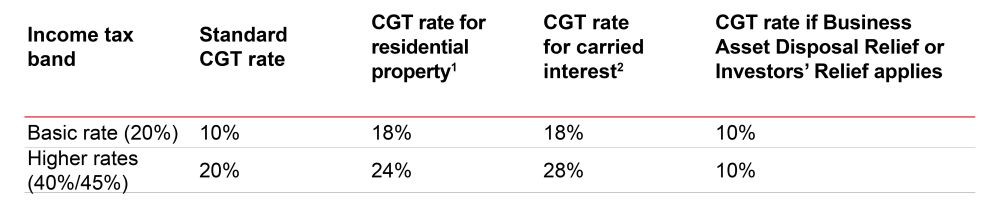

Capital gains tax

The current position

Currently, there are different rates of capital gains tax which depend on the income tax status of the taxpayer and the type of asset being disposed of. All capital gains tax rates are lower than the equivalent income tax rates.

1Note that the higher CGT rate on residential property gains was reduced from 28% to 24% by the 2024 Spring Budget in respect of gains arising on residential property disposals that exchange on or after 6 April 2024. Note also that, where the conditions for principal private residence relief are met, the gain arising on the disposal of an individual's main residence is exempt from capital gains tax.

2Note that the Labour Party has proposed reforming the taxation of carried interest, as mentioned below in the "carried interest" section of this article.

It was announced in the 2022 Autumn Statement that the capital gains tax annual exempt amount (the level of chargeable gains which can be received free of tax in a tax year) would be reduced to £3,000 (for individuals and personal representatives) or £1,500 (for trustees) from April 2024. This was confirmed in the 2024 Spring Budget.

What might a new government do?

The discrepancy between income and capital gains tax rates has been the subject of much discussion in recent years. In November 2020, a report published by the Office of Tax Simplification recommended that the government should consider more closely aligning capital gains tax rates with income tax rates (albeit in conjunction with reintroducing a form of relief for inflationary gains). This report also suggested replacing Business Asset Disposal Relief (BADR, previously Entrepreneurs' Relief) with a relief more focused on retirement, and abolishing Investors' Relief.

However, the current Government has not moved forward with these suggestions and the Conservative manifesto confirms that, if re-elected, capital gains tax rates will not be increased and BADR would be retained. It also pledges to maintain principal private residence relief "so that people's homes are protected from Capital Gains Tax", and to introduce a two-year temporary capital gains tax relief for landlords who sell to their existing tenants.

Although Labour's deputy leader Angela Rayner has previously highlighted the gap between income and capital gains tax rates, Rachel Reeves has sought to distance herself from these comments, confirming on a number of occasions that she has "no plans" to equalise income and capital gains tax rates. The shadow chancellor had also committed to a major review of tax reliefs in her 2021 conference speech, and media reports last year suggested that scrapping or limiting BADR were options being considered by the Labour Party; however, the FT reported in November 2023 that, although all reliefs were kept "under review", Labour had "no plans" to make changes to this relief. Notwithstanding this, the topic of capital gains tax (outside of the context of carried interest) is absent from Labour's manifesto, and concerns were sparked in the run up to its publication by various senior Labour figures refusing to rule out a rise in capital gains tax rates, repeating instead that "nothing in our plan requires additional tax to be raised".

Since the publication of the Labour manifesto, Sir Keir Starmer has ruled out imposing capital gains tax on individuals' main homes. However, the Tribune dossier, leaked to the media this week, is reported to include a proposal to align capital gains tax rates with income tax rates. As mentioned above, Labour have stated that "none of this is Labour policy" and that the document had been rejected; however, entrepreneurs and investors may well remain concerned about reforms to capital gains tax in the event that a new Labour Government requires additional funding.

In this context, it is worth noting that manifestos for both the Liberal Democrat Party and the Green Party include commitments to reform capital gains tax "to close loopholes exploited by the super wealthy" and to align "the rates paid by taxpayers on income and taxable gains", so any future proposals by a new government to introduce reforms to capital gains tax may receive support from other political parties.

Inheritance tax

The current position

Currently, an individual's liability to inheritance tax depends on their domicile status and the location of the asset in question. However, the Government announced in the 2024 Spring Budget that it intends to move to a residence-based regime for inheritance tax from 6 April 2025, with an individual's worldwide assets falling within the scope of UK inheritance tax once such an individual has been UK resident for ten years (with a ten-year "tail" applying after the individual ceases UK residence). In respect of assets held in trust structures, the Government has said that existing rules (whereby non-UK assets, held in trust structures established by non-UK domiciled individuals before they become deemed domiciled in the UK, are outside the scope of UK inheritance tax, even after the individual becomes deemed domiciled in the UK) will remain in place for assets settled into trust before 6 April 2025. The Government has confirmed that there will be a technical consultation before full details of the new inheritance tax regime are finalised.

The 2024 Spring Budget did not announce any changes to inheritance tax rates and it was also confirmed that the inheritance tax nil rate band amount (last increased in April 2009) would remain at £325,000 until April 2028. Although minor changes to the scope of agricultural property relief were announced, the Spring Budget did not propose any major reforms to inheritance tax reliefs.

What might a new government do?

The topic of inheritance tax has been relatively prominent in the media in recent months, with calls from a number of senior Conservative Party backbenchers to abolish the tax, and rumours that this might be included as a Conservative Party manifesto commitment.

A number of recent reports by the Institute of Fiscal Studies (IFS) have also examined the possibility of inheritance tax reforms. A report published by the IFS on 7 September 2023 suggests that there is "significant scope for reforming the base for inheritance tax. Examples of ways in which this could be done include reducing or even eliminating many of the inheritance tax exemptions that exist currently." A further report, published on 27 September 2023, suggests that "abolishing agricultural and business reliefs and bringing pension pots within the scope of inheritance tax could raise up to around £1.5 billion a year", and these claims are repeated in a more recent report, published on 18 April 2024.

However, the Conservative manifesto steered almost entirely clear of the topic of inheritance tax, other than to confirm that agricultural and business property reliefs would be retained. It must, however, be assumed that if the Conservative Party is re-elected, the Government will proceed with implementing its proposed wholesale reform of the inheritance tax regime insofar as it currently applies to non-UK domiciliaries.

Following the announcements regarding inheritance tax reform in conjunction with the abolition of tax benefits for non-UK domiciliaries in the Spring Budget, the Labour Party confirmed that it broadly supports the proposals, but voiced concerns regarding the "major loophole" that would remain if existing rules continue to apply to assets settled into non-UK trusts before 6 April 2025. The Labour Party proposed instead that where a trust's settlor is also a long term UK resident "Labour will include all foreign assets held in a trust within UK inheritance tax, whenever they were settled, so that nobody living here permanently can avoid paying UK inheritance tax on their worldwide estates". Accordingly, although the Labour manifesto was relatively silent on inheritance tax, it specifically confirmed that "we will end the use of offshore trusts to avoid inheritance tax so that everyone who makes their home here in the UK pays their taxes here". This is a very significant point for those UK resident settlors who are not currently within the scope of inheritance tax in relation to trust assets. However, the interaction of inheritance tax and trusts is an extremely complex area. If the Labour Party win the election, we would hope that a technical consultation would still be held on this area of the reforms and so the final outcome remains uncertain.

The Labour manifesto also did not contain any references to inheritance tax reliefs. Media reports have previously suggested that agricultural and business property reliefs were areas that were being examined by the Labour Party for possible reform; however, the FT reported in November 2023 that, although all reliefs were kept "under review", Labour had "no plans" to make changes to agricultural or business property reliefs. It has been reported that the Tribune dossier, leaked to the media this week (and referred to in our national insurance and capital gains tax sections above), includes proposals to abolish agricultural and business property reliefs and to bring pension pots within the scope of inheritance tax. However, as noted above, a party spokesman has stated that the dossier does not represent Labour policy.

Property taxes

The current position

In recent years, a number of significant changes have been made to the taxation of UK property, many of which have been targeted at non-UK resident or non-UK domiciled property owners. A detailed discussion of these reforms is beyond the scope of this note, but have included:

- the introduction of the Annual Tax on Enveloped Dwellings (ATED) regime, applying to "high-value residential property" held by "non-natural persons";

- the extension of capital gains tax to disposals of UK real estate by non-UK residents;

- the removal of inheritance tax advantages for non-UK domiciliaries using non-UK corporate structures to hold UK residential property; and

- the introduction of higher rates of stamp duty land tax (SDLT), both for non-UK resident purchasers and property buyers who already own a property (and will hold more than one property following the purchase).

More recently, the 2024 Spring Budget announced a number of changes relating to the taxation of property disposals, the most significant of which was to reduce the higher capital gains tax rate applying to residential property gains (assuming such gains do not qualify for principal private residence relief – which applies to a disposal of an individual's main residence) from 28% to 24% in respect of residential property disposals that exchange on or after 6 April 2024.

What might a new government do?

The Conservative manifesto makes a number of commitments in respect of property taxes. In particular, the Conservative Party have confirmed that they:

- will not increase SDLT rates;

- will not increase the number of council tax bands, undertake a council tax revaluation or cut council tax discounts;

- will maintain principal private residence relief "so that people's homes are protected from Capital Gains Tax"; and

- introduce a two-year temporary capital gains tax relief for landlords who sell to their existing tenants.

In May 2023, it was reported that the Labour Party intended to:

- accompany support for first-time buyers with measures to redistribute demand away from those looking to purely speculate on house prices; and

- raise SDLT paid by foreign individuals, trusts and companies when they buy UK residential property.

The Labour manifesto confirms its commitment to the second of these policies, pledging to "support local authorities by funding additional planning officers, through increasing the rate of the stamp duty surcharge paid by non-UK residents." The manifesto's policy costings suggest that this increase would be 1%, meaning that the top rate of SDLT applying to non-UK residents would increase from 17% to 18%.

The Labour manifesto contains no other references to property taxation. In particular, as noted in our section on capital gains tax above, the topic of capital gains tax is largely absent from Labour's manifesto. However, following the manifesto's publication, Sir Keir Starmer has ruled out imposing capital gains tax on individuals' main homes, so property owners should be reassured that principal private residence relief should remain in place. Notwithstanding this, a Labour government could introduce other reforms to property taxation, including for example an increase to the capital gains tax rate applying on the disposal of properties which do not qualify for principal private residence relief.

Non-doms

The current position

The UK's "non-dom" regime currently enables UK-resident, non-UK domiciled individuals to:

- elect to be taxed under the favourable "remittance basis" of taxation during their first 15 years of UK tax residence (whereby, in broad terms, qualifying individuals are subject to UK tax only on UK source income and gains, and any non-UK source income and gains which they "remit" to the UK);

- be liable to UK inheritance tax only in respect of UK situs assets during their first 15 years of UK tax residence (and, potentially, for a longer period within a trust structure); and

- benefit from advantageous tax treatment in relation to trusts (even after the initial 15 years of UK tax residence).

However, in a surprise move on 6 March, pre-empting Labour's well-publicised plans in this area, the Conservative Government announced the abolition of the non-dom regime, to be replaced with a new four-year residence-based regime, taking effect from 6 April 2025. Details of the proposed reforms are set out in our separate note.

What might a new government do?

On 6 March, the Treasury published a technical note which fleshed out (in a relatively high-level manner) the Government's non-dom proposals and confirmed that draft legislation would be published "later in the year for technical comments". At the time of the election announcement, various "listening events" were underway, giving interested parties an opportunity to comment on the proposed reforms; however, as soon as the election was announced, all remaining listening events were cancelled and (we assume) work stopped in relation to the drafting of legislation. The Conservative manifesto contains no references to the non-dom regime; however, if the Conservative Party is re-elected, it must be assumed that work will re-commence on the proposals in their current form.

As mentioned above, the Labour Party have been open about their intention to abolish the non-dom regime for many years. A paper published by Rachel Reeves in May 2023, A new business model for Britain, confirms Labour's commitment to "abolishing the non-dom tax status to fund one of the largest expansions of the NHS workforce in its history". The Labour manifesto repeats this commitment, stating that a Labour government would "abolish non-dom status once and for all, replacing it with a modern scheme for people genuinely in the country for a short period".

The extent to which a Labour government would deviate from the Government's existing proposals in this area remains to be seen. However, the Labour Party's initial response to the 6 March announcements has revealed the following points.

- Labour "supports most aspects of the proposed replacement to the non-dom rules", suggesting that any new regime implemented by a Labour government would not be markedly different from existing proposals.

- As noted in our inheritance tax section above, Labour is concerned that current proposals to retain existing rules for the inheritance tax treatment of assets settled into non-UK trusts before April 2025 constitute a "major loophole". Accordingly, the Labour manifesto confirms that the Party "will end the use of offshore trusts to avoid inheritance tax so that everyone who makes their home here in the UK pays their taxes here".

- Current proposals to introduce a number of transitional provisions for existing non-UK domiciliaries (including in particular a proposed 50% reduction to tax on non-UK income for the 2025/26 tax year) may well not materialise.

- Other favourable provisions, for example, a UK investment incentive for individuals qualifying for the new four-year regime, and concessions to encourage former remittance basis users to remit their foreign income and gains, may be introduced.

It seems unlikely that further details will emerge until after the election, perhaps not before the first Budget of a new government, and so there will be continued uncertainty for non-UK domiciled individuals for a further period.

In terms of implementation, the Labour manifesto includes a general statement (relating to all of the policies included in the manifesto) that Labour would "begin to put these policies in place from day one of a Labour government". Given the complexity of this area (and the fact that the current Government has committed to holding a consultation on the inheritance tax aspects of the reforms, something we would hope a Labour government would also honour), a firm timetable may not emerge immediately following the election; however, it is clear that Labour wish to "get to work" on their policies as soon as possible.

Fee-paying schools

The current position

Many private schools are registered as charities and, for such schools, there are a number of tax advantages associated with this, including:

- an exemption from VAT on their fees;

- an entitlement to business rates relief;

- the availability of gift aid on donations made to them; and

- specific exemptions from various forms of income and gains.

Private schools that are not registered as charities are unable to take advantage of all of the above tax reliefs and exemptions; however, since the provision of educational services is exempt from VAT, all private schools currently benefit from not charging VAT on their fees, whether or not they are charities.

What might a new government do?

For quite some time, the Labour Party have been clear about their intention to remove tax exemptions from private schools. Initially, there were suggestions that charitable status would be removed entirely from private schools; however, in recent months, it has become clear that this is no longer their approach and, instead, the Labour Party intend to focus on introducing VAT on fees, as well as ending business rates relief. The Labour manifesto confirms this, stating that "Labour will end the VAT exemption and business rates relief for private schools to invest in our state schools", with such measures estimated to raise over £1.5bn (a figure which accords with a forecast made by the IFS, in a July 2023 report, that such reforms to the taxation of private schools would raise approximately £1.6bn per year in extra revenue). In terms of timing, as noted above, the Labour manifesto simply states the Party's intention to "begin to put these policies in place from day one of a Labour government". In theory, it is possible that such changes could take effect from election day; however, given that it is unlikely that a new government's first Budget will be held before September 2024, it is also possible that the reforms will apply from the date of the Budget (or, potentially, the start of the next tax year – 6 April 2025).

The Conservative Party has always been opposed to any proposal to remove tax reliefs from private schools – in September 2023, the prime minister said that the Labour Party's policy on private schools "illustrates that they don't understand the aspiration of families like my parents who were working really hard". It is therefore unsurprising that the Conservative manifesto contains no references to the taxation of private schools.

Carried interest

The current position

The UK currently taxes carried interest (broadly, the share of investment fund profits which arise to fund managers if a fund performs well) as capital gains rather than income, where certain requirements are met. This means that such profits are subject to UK capital gains tax at a maximum rate of 28%, rather than income tax at a maximum rate of 45%.

What might a new government do?

For quite some time, the Labour Party have been clear about their intention to close the carried interest "loophole". Few details of the policy have been articulated, but the Labour manifesto notes that "private equity is the only industry where performance-related pay is treated as capital gains" and confirms that "Labour will close this loophole". Rachel Reeves has this week been quoted in the Financial Times as saying "I don't think it is right that...what is essentially a bonus is taxed at a lower rate than employment income, when you're not putting your own capital at risk". It therefore seems likely that Labour would limit the availability of capital gains tax treatment to situations where fund managers are putting more than what Rachel Reeves refers to as a "tiny" sum of their own capital at risk.

However, no further details are provided as to how this might be achieved, and the costings in the Labour manifesto show this policy raising additional revenues of £565m per annum by 2028-29. We therefore expect that a Labour government would need to work with Treasury officials to design reforms which maximise revenues and help to continue to grow the UK private capital industry.

The Conservative manifesto contains no references to the taxation of carried interest and so it can be assumed that, in the event of a Conservative victory in the election, no changes to the taxation of carried interest will be implemented.

Wealth tax

The current position

The UK has never had either a one-off or an annual wealth tax. However, there are examples of both internationally, with several jurisdictions introducing new wealth tax measures in the aftermath of the Covid-19 pandemic. In December 2020, a group of academics and tax professionals, known as the "Wealth Tax Commission", published a report of their study into the possibility of a UK wealth tax. The report endorsed the introduction of a one-off wealth tax to help cover the fiscal costs of Covid-19.

What might a new government do?

The Wealth Tax Commission's recommendation has not been adopted by the current Government, and neither the Conservative nor the Labour manifesto contain any suggestions that a wealth tax is being considered by either Party.

In the past, there have been suggestions that a Labour government might be keen to introduce some form of a wealth tax. Indeed, in September 2021, Rachel Reeves remarked that "people who get their income through wealth should have to pay more". However, more recently, she has distanced herself from these comments and, in interviews last year, ruled out the introduction of a wealth tax, instead emphasising the view that the path to prosperity is through economic growth rather than increased taxation. It has been reported that the leaked Tribune dossier (referred to above) proposes the introduction of a "jackpot tax" on "extreme wealth" in order to raise £10bn per year; however, as noted above, Labour have emphasised that the contents of the dossier do not reflect Labour policy.

The Green Party's manifesto confirms its support for a wealth tax, proposing to "tax the wealth of individual taxpayers with assets above £10 million at 1% and assets above £1 billion at 2% annually".

Tax avoidance and reducing the tax gap

The current position

In HMRC's latest published data, for the 2021-22 tax year, the tax gap (i.e. the difference between the amount of tax that is owed and the amount of tax that is actually collected by HMRC) was recorded as £35.8bn, equivalent to 4.8% of total theoretical tax liabilities. The tax gap as a percentage of theoretical tax liabilities has gradually fallen since 2013/14, when it stood at 7%. In recent years, various legislative provisions have been introduced in an attempt to tackle tax avoidance and evasion, and to reduce the tax gap.

What might a new government do?

The Conservative manifesto notes that "...since 2010, Conservative Governments have introduced over 200 measures to tackle tax non-compliance...raising...£6.7 billion for each year" and commits to raising "at least a further £6 billion a year from tackling tax avoidance and evasion by the end of the Parliament". However, no detail is provided on any new policies which might be implemented in order to achieve this target.

The Labour manifesto also promises to address tax avoidance and reduce the tax gap through modernisation of and investment in HMRC, alongside changes to the law. Again, little detail is included in the manifesto; however, Labour's "plan to close the tax gap", published in April this year, provides further information, as set out in our separate article.

Whatever the outcome of the election, any new government will require significant funds to be raised from measures to reduce the tax gap in order to fund their manifesto pledges, so taxpayers should expect an increased focus on compliance.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.