In this edition of the Executive Pay Memo we summarise our key learnings supporting FTSE clients this AGM season.

Over the past 20+ years we have seen UK executive pay design converge, as FTSE organisations have looked to pay practice in other UK public limited companies when designing remuneration policies and have been discouraged from diverging from the accepted UK norm, be it in terms substantive changes to policy, or changes at the margin, or somewhere in between.

At WTW we are proud to be working with key stakeholders, influential bodies such as CMIT and organisations who have brought the debate into sharp focus over the last 18 months. The key areas driving the debate include:

- Unlocking the ability to compete in a global talent

pool

The Boards of the UK's largest organisations have become more diverse. Global organisations rightly seek experience from individuals with global careers and these organisations are consistently struggling to attract and retain the best global talent. The impact is being felt at executive level as well as reporting levels below this due to pay compression challenges, particularly if a company has a large US presence. - Increasing the flexibility on how executive pay is

designed

To be able to compete in different markets does not necessarily mean organisations need to pay more, but potentially, to pay differently. Divergence from the "FTSE norm" of an annual bonus + Performance Share Plans (PSP) should not be a reason to vote against a Remuneration Policy if there is a clear business and talent need to adopt alternative pay models. - Changing the binary "comply or else" approach

to governance

The number of "shareholder friendly" governance features that exist in executive packages is unprecedented compared to other markets (e.g. bonus deferral, LTI holding periods, post-cessation shareholding guidelines, malus and clawback etc.) which has unnecessarily reduced the perceived value of pay. In response to this, this AGM season several organisations have softened their deferral such as reducing the portion of mandatory deferral once the shareholding guideline has been met or partially met. - The need for a level playing field from proxy voting

agencies

UK listed organisations are subject to a more stringent set of proxy guidance than US or European peers. The current diversity in proxy voting policies across regions has the unintended and arbitrary side effect of reducing the competitiveness in some geographies. We previously discussed this in our article - Is executive pay a factor in the decline of London share listings?.

Our learnings from the 2024 AGM season

This AGM season we have supported some of the largest global listed organisations in putting bold remuneration policy proposals in front of investors, based on the priority needs of the business and cognizant of, but not led by, corporate governance expectations. But what have we learned?

01

Establish your fact pattern of competition and performance

Global organisations rightly seek experience from directors with global careers. There has been a general cynicism as to the existence of a genuine global talent market, with some observers questioning whether UK executives would really leave for higher paid roles elsewhere and point to there being sufficient talent in the UK to fill boardrooms without the need to pay a premium hiring from a different market.

Shareholders are more likely to support bold policy changes if an organisation has performed well and returned value to shareholders.

On this basis, a key first input is to clearly establish who your key competitors are from both a business and a talent perspective as this will form the foundation of the rationale to justify bold changes to policy. WTW can perform analysis of senior talent flows using publicly available data to demonstrate where senior talent is recruited from and lost to.

02

Articulate a compelling performance and talent story

We know that shareholders are more likely to support bold policy changes if an organisation has performed well and returned value to shareholders. We have helped our clients tell this story by quantifiably demonstrating that their global footprint has evolved, or quantifying the total value returned to shareholders over a defined period.

Articulating a compelling talent story is equally as important. For instance, by demonstrating how many recent executive hires or departures have been from international markets organisations can demonstrate the pressing talent need to evolve pay at board level. Pay compression can also be visually represented by presenting typical market relativities to the CEO against the reality of pay compression in the company.

Shareholders are more likely to accept increases in board level pay if commensurate changes are made elsewhere in the organisation.

03

Put the changes in the context of wider workforce pay

Executive pay does not exist in a vacuum and shareholders are increasingly focused on fairness relative to the wider workforce and broader stakeholder groups (e.g. consumers and suppliers). We know that shareholders are more likely to accept increases in board level pay if commensurate changes are made elsewhere in the organisation. Articulating the wider workforce pay story has been especially critical against the backdrop of a cost-of-living challenge.

04

Tailor the approach for your shareholder base

Shareholders hold more diverse views than ever and it is key that the views of all are understood and shareholders feel like they are being listened to. We collect investor perspectives from our own outreach and during our clients' consultations, giving us deep insight into the views of investors. Depending on the scale of change, we advise organisations how to approach the consultation process from the means and frequency of outreach, who should attend the meetings, how to "test the water", and how deeply to consult in the shareholder base.

05

Actively solicit shareholder votes post proxy recommendations

Use the short window available to comment on draft proxy reports to re-present your case, and request your response is included. Following the publication of the proxy recommendations, follow up with individual shareholders. Ensure the portfolio and corporate governance teams are aligned and they understand your response to any proxy agency recommendations. It helps to tailor the messaging between those who have been consulted and those who may not have due to their small shareholding.

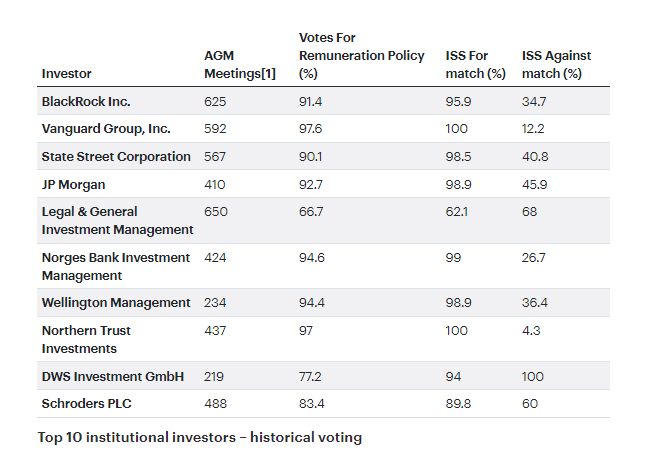

Knowing how your investors have voted in the past, along with their alignment with Institutional Shareholder Services (ISS) recommendations, can help determine the most appropriate engagement strategy.

Below we present the voting history of the largest institutional investors as determined by assets under management. The 'Votes For Remuneration Policy' column is the prevalence the investor has supported the binding resolution to approve the remuneration policy. The 'ISS For / Against' match columns represent the correlation between the investor's voting outcome and the relevant ISS recommendation:

[1] Data represents FTSE 350 AGM's between 01/01/19 – 30/06/24. Note that due to the lag in reporting, data may not reflect all AGM's within this period

Analysis of historical voting patterns can be used to determine the engagement strategy post proxy recommendations. For example, if an investor has a high degree of correlation with an ISS 'Against' recommendation – they should be prioritised in the follow up in the event of such a recommendation from ISS.

06

Create detailed and robust disclosure in your DRR

Proxy agencies make recommendations based only on what is disclosed in the Directors' Remuneration Report. Given their influence on voting out-turns, consider the questions received during consultation and proactively address them in the report. The Chairman's Statement is your opportunity to make a compelling case. Be clear on the constituents of the benchmarking peer groups you use, and why they are the right ones, to avoid broad brush comparison to less relevant peers.

What next?

We expect the UK pay market to continue to evolve at pace. We are continuing to support our clients in addressing business and talent issues through changes to executive pay policy of varying scale. This includes changes at the margin to more substantive changes such as aligning pay policy with US/global peers from a quantum or structure perspective, or both.

The evolution of pay within the FTSE will have consequences for all organisations, not just those making the change. Significant increases in pay levels over time will impact pay positioning of all organisations relative to the FTSE market and experience tells us that change at the top of the FTSE will eventually flow downwards. As such, Remuneration Committees will need to pay even closer attention to the external landscape to ensure their organisation is not out of step with the pay market.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.