Victorian State Revenue Office Updates

Commercial and industrial properties in Victoria will no longer be subject to upfront stamp duty (land transfer duty) from July 1, 2024.

On 21 May 2024 the Commercial and Industrial Property Tax Reform Act received Royal Assent, following the Victorian Government's earlier announcement of the new scheme.

The tax reform is designed to boost economic activity by encouraging businesses to invest in Victoria and generate further job opportunities through the reduction in the initial cost of purchasing commercial and industrial properties.

Key Dates

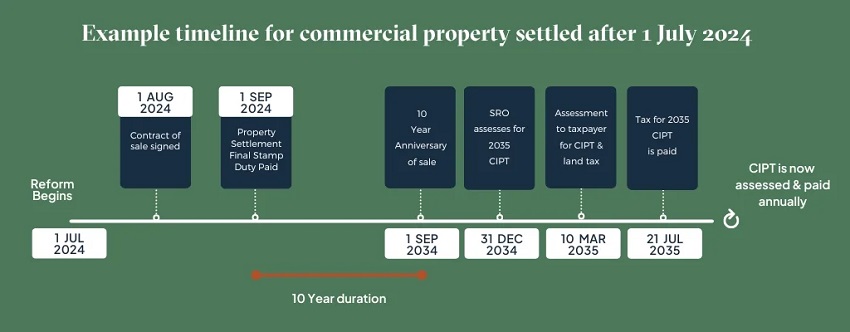

The new Commercial and Industrial Property Tax (C&IP Tax) will apply to commercial and industrial property (C&I) transactions with both a contract and settlement dated on or after 1 July 2024.

Under the new system, commercial and industrial property transactions will trigger stamp duty for the last time and the C&IP Tax will be payable 10 years after the final stamp duty payment. Crucially, once a property is subject to this new tax, stamp duty will no longer apply, even if the property changes ownership, as long as it continues to be used for commercial or industrial purposes.

An stylised example of the entry into the new tax system is diagrammatically depicted below:

Key Features of the CIPT

The key features of the new tax is summarised below:

- A single flat rate of one (1) percent of a property's unimproved land value.

- Exemptions that apply to land tax will also apply.

- Streamlined administration similar to arrangements for land tax.

- Existing stamp duty concessions for commercial and industrial properties, including the regional concession, will remain available.

- Information for whether a property has entered the new tax system will be included on the Property Clearance Certificate issued by the State Revenue Office.

- If a property that is in the reform is subdivided, the child lots will be exempt from stamp duty if they transact and only subjected to the C&IP tax 10 years after the initial transaction of the parent property.

- Where a less than 100% interest but minimum of 50% interest in the property is transacted on or after 1 July 2024, a subsequent transaction which relates to a different interest in the land may be chargeable with land transfer duty for a 3-year period or until full duty has been assessed on the land (whichever is earlier).

Transitional Loan

Eligible purchasers will also have the option to access a government-facilitated transition loan. This loan, provided by the Treasury Corporation of Victoria on commercial terms with a fixed interest rate, will enable businesses to fund their last stamp duty payment, thereby freeing up capital for expansion or hiring more workers.

Additional details on the transition loan, including eligibility criteria and terms, will be communicated by the Victorian Government before July 1, 2024.

Foreign owners will not be eligible to apply for the transitional loan.

Properties That Are Not Part of The Reform

These reforms will not affect the following properties used for:

- Residential purposes;

- Primary production;

- Community services, sport, heritage, or cultural purposes;

- Transfers which are stamp duty exempt (eg. purchaser is a charity, transfer to a deceased estate etc);

- Commercial and industrial property purchased prior to 1 July 2024 (unless 50% or more of the property is transacted after this date).

C&IP Tax Separate to Land Tax

It is important to note that the C&IP Tax, while of similar flavour to land tax, will be separate to land tax. That is, the C&IP Tax does not infringe or amend any land tax liabilities, concessions or exemptions that apply to a particular commercial and industrial property.

Mixed Used Properties – Sole or Primary Use Test

Properties that will have a mixed use will only enter into the new C&IP Tax regime based on the sole or primary use test.

Under the sole or primary use test, if it shows that a particular property is qualifying, then the C&IP Tax will apply to the entire property.

The sole and primary use test is to be determined with reference to factors such as land or floor area of each use, relative intensity, economic and financial significance of each use, length of time of each use and other factors.

Note: Student accommodation will be included as a qualifying use for the purpose of the reform. Land which is solely or primarily used as commercial residential premises and that is used solely or primarily for providing accommodation to tertiary students will be considered commercial property.

Change of Use

The application of the new C&IP Tax to properties which have a change of use are broadly summarised below:

- Qualifying use converted to non-qualifying Use – Not liable for C&IP Tax if non-qualifying use continues as at the taxing liability date.

- Qualifying use sold second or subsequent time and then converted to non-qualifying use – Change of use duty may apply

Change-of-use-duty is intended to apply where no stamp duty was paid on a recent property transaction(s) and when the property is converted to a non-qualifying use such that no C&IP Tax would apply.

Providing Expert Advice on Tax Matters

If you are unsure about how these changes will impact your investment or business, we can provide clear and reliable advice.

Our experienced taxation lawyers have deep knowledge of tax law and practical experience in handling matters with the State Revenue Offices across Australia and the Australian Taxation Office.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.