- within Compliance, International Law and Employment and HR topic(s)

- with Senior Company Executives, HR and Inhouse Counsel

- with readers working within the Business & Consumer Services, Media & Information and Metals & Mining industries

Michael Bacina, Steven Pettigrove, Jake Huang, Luke Higgins & Luke Misthos of the Piper Alderman Blockchain Group bring you the latest legal, regulatory and project updates in Blockchain and Digital Law.

Bitcoin ETFs growing on Australian markets

After the US Securities and Exchange Commission approved a raft of spot bitcoin exchange traded fund (ETF) and gave the greenlight to key regulatory filings for several spot Ether ETF, the trend has finally made its way to down under. This week, the Australian Securities Exchange (ASX) approved its first-ever Bitcoin ETF, following a successful Bitcoin ETF listing at rival exchange Cboe Australia earlier this month.

The VanEck Bitcoin ETF will list on the ASX under the ticker VBTC this week, making it the first ETF on the exchange that tracks the price of Bitcoin. VanEck' Asia Pacific managing director, Arian Neiron, expressed his confidence in the fund, saying that Bitcoin is an

emerging asset class that many advisers and investors want.

Neiron also mentioned the benefits of investing in Bitcoin via a regulated vehicle such as VBTC,

We have developed a robust offering that we believe provides an opportunity for bitcoin exposure using a regulated, transparent and familiar investment vehicle.

VanEck's website also posted a blog that says

we consider the ETF vehicle is the optimal delivery mechanism for an asset class like bitcoin.

It is reported that VBTC will primarily act as a 'feeder fund' that employs a passive management strategy, and provide Australian investors exposure to Bitcoin by investing in its US sister ETF – the VanEck Bitcoin Trust (ticker HODL).

Earlier this month, Australia-based Monochrome Asset Management won approval from Cboe Australia to list its Monochrome Bitcoin ETF (ticker IBTC). Unlike VBTC, Monochrome's IBTC is the first and only ETF that holds Bitcoin directly in Australia. Monochrome now joins Global X's 21Shares Bitcoin ETF, which has operated on Cboe since 2022 and was the best-performing listed ETF in Australia in the 12 months to March 31, with a whopping 153.4% return.

Michael Bacina, Partner of this firm and Chair of Blockchain Australia (recently rebranded as 'DECA' during the annual Blockchain Week) commented:

A Bitcoin ETF being available on major Australian stock exchanges is a great movement forward for the crypto-space...

He also added that:

It's important to note the key differences between the products, as only one of the ETFs has direct Bitcoin holdings and can offer holders a redemption in Bitcoin.

The approval of Bitcoin ETFs in Australia has taken years to materialise. They arrive almost six months after the SEC approved 9 Bitcoin ETFs in the US. The US listing has reportedly helped draw in a new wave of institutional investors, including several global hedge fund giants. Many Tradfi and banking giants have also jumped on the Bitcoin ETF band wagon. It is reported that iShare's Bitcoin Trust, the most popular US Bitcoin ETF, holds about USD$19.5 billion in digital assets.

Given Australia's robust regulatory and exchange framework, it is no small feat to secure approvals from the regulators and exchanges to list any ETF, including one referencin a novel and emerging asset class. With the popularity of US issued Bitcoin and Ether ETF exceeding expectations, we expect to see more of them coming to the market in Australia in the coming years.

ASIC appeals Block Earner penalty decision

The Australian Securities and Investments Commission (ASIC) has lodged a Notice of Appeal against the Federal Court's decision to relieve Block Earner from liability to pay civil penalties for contravening the Corporations Act 2001 (Cth) (Corporations Act).

On 4 June 2024, his Honour Justice Jackman of the Federal Court found that Block Earner would be relieved from pecuniary penalties after breaching the Corporations Act by providing unlicensed financial services in the form of its Earner product.

ASIC's appeal

ASIC's notice of appeal outlines three grounds of appeal, which contests both the factual findings and legal analyses of Justice Jackman's 4 June 2024 decision. In summary, ASIC is seeking to overturn nearly all of Justice Jackman's penalty decision, other than the order that the parties bear their own costs for the main proceedings, meaning ASIC cannot recover any of the costs they incurred in suing Block Earner.

Ground One

The first ground of appeal is a contention that Justice Jackman entirely erred in finding that section 1317S of the Corporations Act, in all the circumstances considered by the Federal Court, should relieve Block Earner from liability.

As we set out in our article on Justice Jackman's earlier judgment, section 1317S of the Corporations Act acts as a safety net for those that have breached the civil penalty provisions of the Corporations Act but otherwise acted with honesty.

ASIC contends that Justice Jackman was in error to apply the relief as the circumstances when considered as a whole indicated otherwise.

Ground Two

This ground of appeal is split across four sub-grounds. First, ASIC contends Justice Jackman erred by inferring that Block Earner had relied on legal advice to reasonably form the view that there was no identified risk the Earner product would breach relevant provisions of the Corporations Act as no evidence put forward by Block Earner to that effect. ASIC also contends that Justice Jackman erred by drawing favourable inferences to Block Earner in relation to the legal advice obtained by Block Earner in circumstances where Block Earner did not tender the document due to legal professional privilege.

This is an interesting point as privilege was not waived over the legal advice, so neither Justice Jackman, nor ASIC, has seen the contents of the advice.

Second, ASIC argues that Justice Jackman erred by providing relief to Block Earner in circumstances where Block Earner profited from the unlicensed offering of Earner. This is despite his Honour's finding that the relatively small profit of Block Earner, being $21,306.90, was not a matter of "substantial weight" to his finding.

Third, ASIC contends Justice Jackman erred by considering the uncertain regulatory environment as a relevant consideration in circumstances where Block Earner perceived said uncertainty but nonetheless engaged in contravening conduct to make a profit. Given the absence of any clear guidance from ASIC on crypto-assets and the numerous consultations which have been undertaken by Treasury, it will be interesting to see how this ground of appeal is addressed.

In its fourth ground of appeal, ASIC is doubling-down on the issues concerning their press release, which Justice Jackman found was unfair and misleading.

Ground Three

Finally, ASIC contends that Justice Jackman erred in finding that he would not have imposed a penalty even if all the facts available under section 1317S of the Corporations Act were not present.

Penalty sought

ASIC is still pressing for the Full Federal Court to impose "a pecuniary penalty in the amount of $350,000 or such other amount the Court sees fit". This was the amount originally sought by ASIC and rejected by Justice Jackson.

Conclusion

ASIC's appeal has caused concern in the Australian crypto-community signaling an aggressive enforcement posture against those who seek to develop innovative product offerings in an uncertain and shifting regulatory environment.

ASIC is likely to face a number of challenges in their appeal, including that appeals from discretionary matters such as penalty decisions are difficult to challenge, and ASIC's decision not to challenge evidence from Block Earner, noting that there are 9 references to "unchallenged evidence" in the judgment concerning matters argued by Block Earner.

Beneath the legal matters arising from this appeal lies a far more important macro issue, that regulation, sought by the industry for years, is finally starting to be formed, and that regulation by enforcement is a very inefficient means to make rules, as has been seen in the USA, and often court decisions can raise more questions than they answer.

In a regulatory environment that has been judicially recognised as unclear and "tangled mess", the question of how precious public funds are spent and what outcomes are being achieved from that spending is an important question that needs to be considered. Setting clear rules of the road and a viable pathway for licensing for crypto-asset products, to the extent it is required to manage real risks (such as custody), would appear an outcome more consistent with traditional notions of rule of law and one better reached by consultation and rule/law-making by parliament.

Australian Blockchain Week quotes

With Blockchain Australia transitioning to the Digital Economy Council of Australia, Blockchain Week 2024 was a huge event for the organisation, and a great opportunity to share industry insights as we move towards a licensing regime and clearer rules of the road for the blockchain industry.

Day 1 of the festivities focused on builders and innovators in the industry and began with Sean White from XDC Network stating it's time for TradFi to meet Web3 halfway:

TradFi is at the point now where it can meet us halfway as an industry with what we're doing in the digital economy space.

This continued with a tax discussion from Shane Brunette from Crypto Tax Calculator who gave a stern warning to those hoping to skirt tax laws:

The industry needs to empower individuals to report accurately. Otherwise the government will be forced to do so.

ASIC's Jonathan Hatch, a senior advisor in ASIC's Innovation Hub, mentioned the industry's growth in his keynote speech:

In the past 10 years we were talking about historically what was happening. Now we are talking about the solutions and how we will help people. Now you are starting to see the maturity of the industry.

Day 2, titled 'Digital Assets: Anchoring the Digital Economy' saw an appearance from Dr Rhys Bollen, the lead of ASIC's digital assets team, who warned the industry to consult legal professionals in light of recent ASIC "test cases" and "evolved" thinking:

When did you last review the tokens that you list on your platform? When was the last time you reviewed the products and services that you are making available? How recently have you consulted with your lawyers about where the law currently sees the most current understanding based on cases over the last six months or so. If you haven't done that in the last four months you need to consider where you are,

Although Dr Bollen stated the keen interest of industry participants to be regulated:

We have a number of crypto and digital asset businesses in our ecosystem and we have many going through the application process.

Day 3's Adaption and Evolution discussions considered, among other things, scams in the industry with a warning from Charis Chan from Chainalysis:

Scammers are seizing opportunities. In a bull market, we do see more scam activity because there is more profit to be made in those times.

Ms Chan also alerted the audience to the scourge of industrial scam farms, including the notorious KK Park in Myanmar.

In addition, CSIRO's Mark Staples raised interesting points regarding Central Bank Digital Currencies:

We haven't seen a lot of use cases which are general retail use like buying coffee. A lot of people are worried that the government will force us to use CBDCs, but actually it might be that Australians won't be allowed to use CBDCs in that way.

And Dr Andrzej Gwidalski from WAWEB3 and ACS says there needs to be careful planning when considering the use of any new form of digital money in the market:

It is more complex when you want to do a deal and trade, and the money needs to speak to each other across borders.

Chris Adamek, director of the Australian Treasury's digital asset policy unit spoke on the upcoming exposure draft:

The digital asset platform reforms have been allocated a drafting spot with The Office of Parliamentary Council (responsible for drafting and publishing Australian laws) that would see the exposure draft released before the end of this year.

Chris Chen of Backpack outlined the regulatory clarity in other jurisdictions:

The EU provides very clear guidance on what is needed, and many of the obligations are not friendly to those with a small budget but it comes down to what you want to do.

Dr Stephanie Bazley from Possible Ventures echoed this sentiment:

I've seen a lot of crypto projects choosing a jurisdiction to be able to hire better and reach customers faster because of a better reputation of blockchain in that jurisdiction.

The final day of Blockchain Week 2024 saw the Blockchain Fringe Festival take flight and the latest meeting of the Blockchain Lawyers Forum at our Sydney office with Dr Bollen again representing ASIC, this time for a Chatham House discussion on a range of policy and regulatory issues affecting the crypto industry.

Another successful Blockchain Week in the books featuring a range of high quality discussions and broad engagement across the industry. As Blockchain Australia celebrated its 10th year and transitions to DECA, the industry looks set for another year of rapid change as the technology becomes increasingly integrated with our digital future.

Stand with Crypto UK policy proposals: also useful for Australia?

Coinbase has rolled out its "Stand With Crypto" policy recommendations ahead of the upcoming election in the United Kingdom (UK). This strategic initiative underscores Coinbase's commitment to advocating for a more robust and forward-thinking crypto regulatory framework in the United Kingdom.

In a self described manifesto, Coinbase said the next government should focus on promoting Web3 in the UK and establish a hub for growth and development.

We believe the next Government should take meaningful steps to position the UK as a global hub of digital assets, tokenization and fintech.

The policy matters raised in this document are worthy of Australia taking note, covering several critical recommendations aimed at fostering a more conducive environment for the crypto industry. These include:

- Global Hub Promotion: Establish the UK as a leader in Web3 and tokenisation, highlighting openness for fintech and crypto businesses through a government-industry task force.

- Comprehensive Regulatory Framework: Implement clear regulations for crypto assets, ensuring consumer protection and industry standards. Legislate fiat-backed stablecoins to encourage competition.

- Staking Clarity: Introduce legislation recognising staking as a regulated activity, preserving retail participation vital for proof-of-stake blockchains.

- Promote Decentralisation Benefits: Conduct detailed policy work on the unique advantages of decentralisation, impacting sectors like education, healthcare, and energy.

- Blockchain Strategy: Develop a cross-government strategy led by the Department for Science, Innovation and Technology (DSIT) to harness blockchain technology for efficiency across public services.

- Tokenisation Strategy: Overturn the prohibition on retail access to crypto Exchange Traded Notes (ETNs) and promote tokenisation innovation through sandbox environments.

- Legal Framework Update: Update UK laws based on Law Commission recommendations to ensure certainty on digital property rights and establish a crypto collateral regime.

Coinbase's move to release these recommendations just before the UK election appears a calculated effort to inform and influence policymakers and try to shape the future regulatory landscape in the UK. The company is leveraging its position as a leading crypto exchange to advocate for a regulatory framework that promotes growth, innovation, and consumer protection in the digital asset space.

As the UK gears up for its next election, Coinbase's "Stand With Crypto" policy highlights the growing importance of regulatory clarity and supportive policies in the crypto industry. By taking a proactive stance, Coinbase aims to ensure that the UK remains at the forefront of the global crypto market, fostering an environment that encourages innovation while protecting consumers. Australian policymakers, currently drafting licensing laws, could learn from these principles as we see our framework emerging, if they too wish Australia to benefit from this foundational technology.

Out of the Ether: SEC closes file on Ethereum 2.0

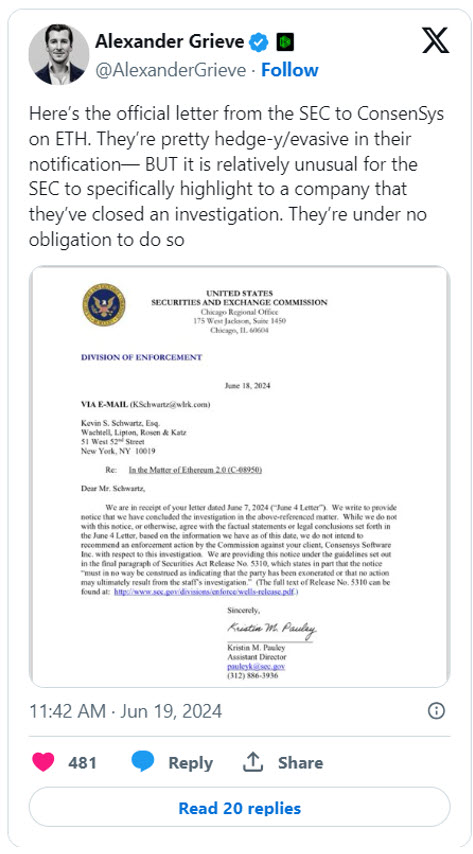

Leading Ethereum developer Consensys has announced via a blog post that the Securities and Exchange Commission (SEC) has closed its investigation into the firm only two months after issuing a Wells Notice in relation to its popular MetaMask swaps and staking product. While the SEC's confirmation was carefully caveated, this decision suggests that the SEC has finally determined not to pursue allegations that the cryptocurrency ETH (the post-merge proof of stake based Ethereum) is a security after months of prevarication by the SEC Chair Gary Gensler.

Way back in June 2018, Director of the Corporation Finance division of the SEC William Hinman declared in a speech that ETH, the native cryptocurrency of the Ethereum network, was not a security. By 2023 however, it appeared that SEC was again seeking to claim jurisdiction over ETH, initiating a sweeping investigation that Consensys argued was a violation of basic due process and would have a chilling effect on innovation.

As the largest Ethereum-based blockchain developer, Consensys decided to bite back by filing a lawsuit against the SEC in April of this year. The lawsuit sought a court order to halt the SEC's investigation, arguing that ETH is a commodity and thus outside the SEC's jurisdiction.

According to the blog post, the legal action sparked a wave of concern among policymakers, including members of Congress, and the public at large. Earlier this month Consensys requested the SEC to confirm that the approval of ETH exchange traded funds in May 2024, which was based on the premise of ETH being a commodity, would lead to the closure of its Ethereum 2.0 investigation. The SEC's Enforcement Division responded affirmatively, notifying Consensys that it is closing its investigation into Ethereum 2.0 and will not pursue an enforcement action against the company.

Alexander Grieve, Government Affairs Lead of Paradigm, noted the unusual nature of the SEC's behaviour in a post on X:

Consensys for its part has indicated its intention to continue to pursue its claim for declaratory relief from securities law violations relating to its swap and staking products.

While this decision is a significant victory for Consensys and the broader Ethereum community, it also underscores the urgent need for clear and consistent regulatory guidelines for the crypto industry in the US and the rest of the world. The SEC's approach of "regulation by enforcement" has been widely criticised for its lack of transparency and predictability, creating an environment of uncertainty that stifles innovation.

While the SEC's decision to close its investigation into Ethereum 2.0 is indeed positive, it is merely a temporary reprieve that underscores the precarious nature of innovation in an industry that is still grappling with significant uncertainty. Here is hoping that this development marks the beginning of a new path forward, which as Consensys has argued gives much-needed regulatory clarity for an industry that serves as the backbone to countless new technologies and innovations.

One hat, two hat, white hat, black hat

Kraken, a leading international crypto-exchange, has been the subject of intense dispute recently over a critical vulnerability exposed by a security group which provides a lesson in how not to conduct "white hat hacking".

"White hat hacking" involves using hacking tools for ethical purposes, and is a valuable part of information technology and crypto-assets and blockchain. Many projects offer bug bounties to encourage white hats to try and hack their systems and then report vulnerabilities so that they may be patched. Over time this should result in stronger and more resilient systems. White hats are contrasted against "black hat" hackers who hack for personal gain and profit or otherwise act maliciously. Kevin Mitnick is probably the most famous black hat hacker who broke into over 40 US government systems and ultimately went to jail and became a cybersecurity consultant.

"Grey hat" hackers sit between the white and black, often hacking without the invitation of a project owner, looking for vulnerabilities in systems and then approaching the owner, asking for a fee to assist in fixing the problem.

The Hack

Kraken's Chief Security Officer took to X (formerly Twitter) yesterday to announce that:

- On 9 June, a bug bounty submission was received claiming to have found an 'extremely critical' bug allowing artificial account balance inflation (i.e. creating free money);

- A flag in a recent interface change was found and fixed within a matter of hours.

- 3 accounts were identified which had leveraged the bug, one of those accounts took USD$4 in value and the other 2 accounts took USD$3M from Kraken.

- One of the three accounts had know-your-customer information from a person who claimed to be a security researcher.

- The security researcher declined to co-operate to provide information on the bug and demanded a call with their "business development team" and refused to return any of the USD$3M until a fee was agreed.

Mr Percoco said

This is not white-hat hacking, it is extortion!

Kraken did not identify the "security researcher" but indicated it was now a police matter:

Within a matter of hours, Certik posted on X to out themselves as having identified a critical vulnerability in Kraken and claimed they were threatened by Kraken and demanded to pay a "mismatched amount of crypto in an unreasonable time even without providing repayment addresses".

They asserted the tokens created were "minted out of thin air" prompting a smart reply from user CryptoFinally:

Certik also asserted:

The real question should be why Kraken's in-depth defense systems failed to detect so many test transactions. Continuous large withdrawals from different testing accounts was a part of our testing.

This position was roundly ridiculed by many users on X including the following gems:

The final nail in the coffin was uncovered courtesy of block explorers showing that the funds taken from Kraken were put through tornado cash.

The Take-away

Leading security researchers such as the Security Alliance are developing governance frameworks such as the SEAL 911 emergency helpline to facilitate safe disclosure of critical vulnerabilities and the SEAL Whitehat Safe Harbor to give white hat hackers clear guardrails to operate in circumstances where it may be necessary to take and return substantial sums of crypto-assets to protect them from an attacker.

The Kraken situation provides a lesson in the pretty clear line between white/grey and black hat hacking. It seems implausible that a true white hat hacker would engage in more than the minimum number of transactions necessary to demonstrate a flaw prior to informing the owner and giving all necessary information to fix the problem, and withholding funds for reasons such as "mismatched" amounts or "unreasonable timeframes" given the simplicity of requesting and verifying blockchain addresses will lead to the swift involvement of law enforcement.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.