On September 18, 2023, the U.S. Basel III Endgame proposal was published in the Federal Register. The comment period ended on January 16, 2024, with the banking regulators (the Federal Reserve, the OCC, and the FDIC) having received hundreds of comments on the proposal. Acknowledging the many concerns raised in the comment letters, Federal Reserve Chairman Jerome Powell indicated in his March 2024 Congressional testimony that "there will be broad material changes to the proposal." On June 24, Bloomberg reported that the Federal Reserve has "shown other US regulators a three-page document of possible changes to their bank-capital overhaul that would significantly lighten the load on Wall Street lenders."

At this writing, it remains unclear whether (or when) the banking regulators will adopt a final rule or, one hopes, issue a re-proposal. The banking regulators have been faced with the daunting task of analyzing the many technical and substantive concerns raised in the comment letters. Several other factors are contributing to the uncertainty surrounding the timing and nature of the banking regulators' next step, including:

- Joint Rulemaking. All three banking regulators must agree on any changes to the Basel III Endgame proposal. Reaching agreement on the "broad material changes" promised by Chairman Powell could take considerable time and effort, particularly given the differing perspectives of the three banking regulators.

- FDIC Leadership Transition. On May 20, 2024, FDIC Chairman Martin J. Gruenberg announced that he would step down from his position once a successor is confirmed. This transition could have the effect of causing a delay (g., FDIC may be reluctant to act until a new chair is in place) or an acceleration (e.g., FDIC may seek to issue a final rule before Chairman Gruenberg steps down) of the rulemaking process.

- CRA/November Elections. Congressional Review Act ("CRA") considerations could motivate the banking regulators to move quickly to adopt a final rule. Under the CRA, Congress can overturn a regulatory agency's final rule if a joint resolution of disapproval is (1) introduced within 60 legislative days following the date the final rule, (2) approved by both houses of Congress, and (3) signed by the President (or vetoed by the President, followed by a Congressional override). By moving quickly to adopt a final rule, the banking regulators could attempt to ensure that the 60-day CRA window closes before the new Congress is seated (and, perhaps, the new President takes office) following the November 2024 elections.

- Supreme Court Decision on Agency Rulemaking. The U.S. Supreme Court's imminent decision in Loper Bright Enterprises v. Raimondo is likely to significantly limit the degree to which courts must defer to regulatory agencies under the long-standing Chevron Many of the comment letters assert that the Basel III Endgame proposal and related rulemaking process do not comply with requirements of the Administrative Procedure Act and existing caselaw construing such requirements. The Loper case could increase the susceptibility of any final rule to legal challenge, thus potentially encouraging the banking regulators to issue a re-proposal that is less susceptible to challenge.

Securitization Framework

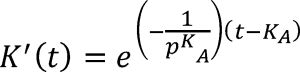

As a reminder, the Basel III Endgame proposal includes significant changes to the mathematical model that assigns credit risk weights to securitization exposures. Both the existing "simplified supervisory formula approach" ("SSFA") and the proposed "securitization standardized approach" ("SEC-SA") incorporate a formula, referred to as

and

respectively, that calculates the average value of the marginal risk weighting function

over the interval t = A to t = D. Under this function, A and D are the attachment and detachment points, respectively, of a securitization exposure, p is the supervisory calibration parameter (the p-factor), and KA is the capital requirement of the underlying exposures, adjusted for defaults.

Of particular concern is the increase in the p-factor from 0.5 (under SSFA) to 1.0 (under the proposed SEC-SA). As the Structured Finance Association's ("SFA") comment letter explains, the increase in the p-factor from 0.5 to 1.0 effectively doubles the securitization capital surcharge and creates a host of anomalies. These points were emphasized by the SFA in a later meeting with the staffs of the banking regulators (pages 18-28 of the meeting summary contain helpful illustrations).

We note that p-factor value is a topic of concern not only in the U.S., but also on the UK and the EU. See, e.g., The UK's PRA Discusses Securitisation Capital Requirements and Basel 3.1, by Alix Prentice, a partner in our London office.

Securitization market participants who are interested in the next stage of the Basel III Endgame rulemaking should consider joining SFA's Basel III Task Force, which is led by W. Scott Frame, the Chief Economist & Head of Policy at the SFA. Scott recently authored De-Risking Banks through Synthetic Securitization and Credit-Linked Note Issuance, which is an excellent overview of bank credit risk transfer ("CRT") transactions. CRT transactions would be significantly affected if the Basel III Endgame proposal is adopted in its current form.

We also bring to your attention the Basel III Endgame Blog Series, by Dr. Guowei Zhang and Dr. Peter Ryan of the Securities Industry and Financial Markets Association ("SIFMA"). Part X ("How the Basel III Endgame Could Impair Securitization Markets and Harm US Businesses and Consumers") is particularly insightful.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.