The Financial Crimes Enforcement Network and the Internal Revenue Service recently issued three notices, FinCEN Notices 2011-1 and 2011-2 and IRS Notice 2011-54, granting an extension of the filing deadline for the Report of Foreign Bank and Financial Accounts (FBAR), IRS Form TD-F 90-22.1 to different groups of individuals with signature or other authority over certain foreign financial accounts for various filing years.

The Financial Crimes Enforcement Network (FinCEN), a division of the U.S. Treasury Department, and the Internal Revenue Service (IRS), recently issued three notices, FinCEN Notices 2011-1 and 2011-2 and IRS Notice 2011-54. Each notice granted an extension of the filing deadline for the Report of Foreign Bank and Financial Accounts (FBAR), IRS Form TD-F 90-22.1 to different groups of individuals with signature or other authority over certain foreign financial accounts for various filing years. Refer to our previous On the Subject for a discussion of whether an individual has signature or other authority over a foreign financial account.While the extensions provide welcome relief, some June 30, 2011 filing obligations still remain.

FinCEN Notice 2011-1

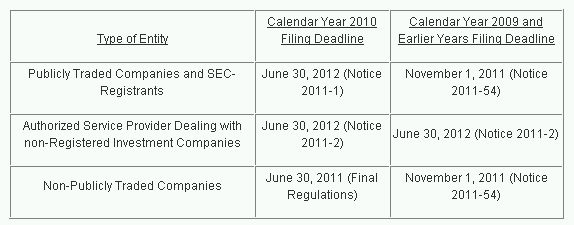

On May 31, 2011, FinCEN issued Notice 2011-1 (subsequently clarified on June 6, 2011), which grants a one-year extension of the filing deadline for the FBAR for the 2010 tax year, from June 30, 2011 to June 30, 2012, to some individuals with signature or other authority over certain foreign financial accounts.

The one-year extension relief provided in FinCEN Notice 2011-1 is limited to certain employees and officers of a publicly traded company or U.S. Securities and Exchange Commission (SEC) registrant who have signature or other authority over, but no financial interest in, a foreign financial account. The relief does not apply to an employee or officer of an entity that is not a publicly traded company or of a non-SEC registrant that has signature or other authority, but no financial interest in, a foreign financial account.

IRS Notice 2011-54

On June 16, 2011, the IRS issued IRS Notice 2011-54, granting additional relief to persons with signature or other authority over, but no financial interest in, a foreign financial account held during calendar year 2009 or earlier calendar years. Previously, the IRS extended the FBAR filing deadline to June 30, 2011 for persons with signature or other authority over, but no financial interest in, a foreign financial account for 2009 and earlier calendar years. The IRS issued IRS Notice 2011-54 in reaction to concerns that individuals with signature authority over, but no financial interest in, a foreign financial account were encountering difficulty compiling the data necessary to complete the FBAR for 2009 and earlier calendar years.

IRS Notice 2011-54 extends the FBAR filing deadline from June 30, 2011 until November 1, 2011 for all persons with signature authority over, but no financial interest in, a foreign financial account in 2009 or earlier calendar years. The deadline for the 2010 calendar year remains June 30, 2011.

FinCEN Notice 2011-2

On June 17, 2011, FinCEN issued FinCEN Notice 2011-2, which grants a one-year extension of the FBAR filing deadline, from June 30, 2011 to June 30, 2012, to officers and employees of investment advisors registered with the SEC with signature or other authority over, but no financial interest in, the foreign financial accounts of an investment company that is not registered with the SEC. The relief applies to FBARs for calendar year 2010 as well as FBARs for calendar year 2009 and earlier years.

The following chart summarizes the FBAR filing deadlines as modified by FinCEN Notice 2011-1, IRS Notice 2011-54, and FinCEN Notice 2011-2. McDermott will provide additional updates to the FBAR filing requirements as guidance is published.

SUMMARY OF THE FILING OBLIGATIONS FOR PARTIES WITH SIGNATURE AUTHORITY OVER, BUT NO FINANCIAL INTEREST IN, FOREIGN FINANCIAL ACCOUNTS

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

We operate a free-to-view policy, asking only that you register in order to read all of our content. Please login or register to view the rest of this article.