Navigating Divergent Consumer Needs in a Challenging Economic Landscape

As the Back-to-School (BTS) shopping season of 2024 unfolds, it is set against a backdrop of economic uncertainty and consumer caution. Inflation and rising living costs are significantly shaping consumer sentiment and spending habits. Our recent BTS shopper survey, detailed in the Ankura Back-to-School Shopping Report 2024, sheds light on how these economic factors are influencing BTS shoppers, highlighting the bifurcated consumer sentiment that presents both challenges and opportunities for retailers.

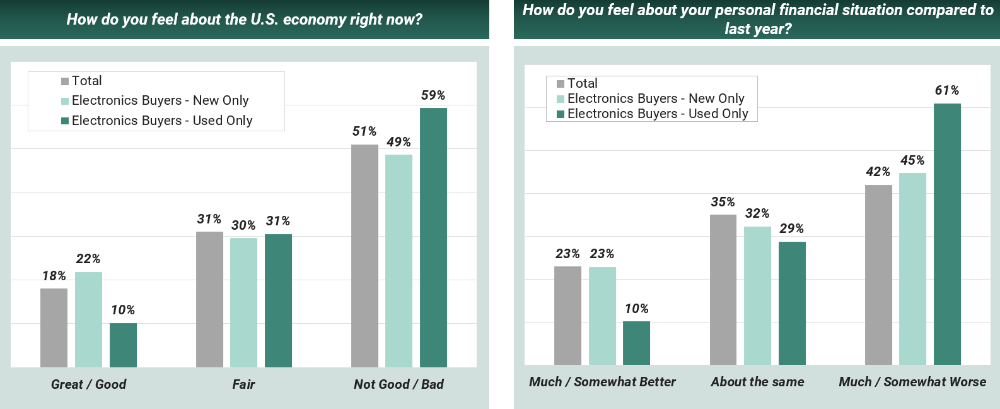

Inflation, both actual and perceived, remains a top concern for consumers. Our survey indicates that 51% of BTS shoppers hold negative feelings towards the U.S. economy, reflecting broader economic indicators that suggest ongoing financial strain for many households.

In this three-part series focusing on our survey, we will delve into detailed insights, exploring the key challenges retailers face not only during the BTS season but throughout the remainder of 2024.

A Bifurcated Consumer Pool: A Key Impact on Shopping Intent

Consumer sentiment is bifurcated, with optimism about personal finances and the U.S. economy on one side, and continued pessimism on the other. This dual outlook influences shopping intent significantly:

Considering this continued pessimistic economic sentiment by a large percentage of our BTS respondents, retailers hoping those who have sat on the sidelines would return for BTS will be disappointed. Instead, retailers should focus energy on coddling their existing customer base with personalized discounts and promotions, loyalty rewards, and merchandised assortments.

Optimism vs. Pessimism: Current Sentiment Drives Future Outlook

Our survey reveals a complex interplay of macroeconomic concerns and individual financial realities:

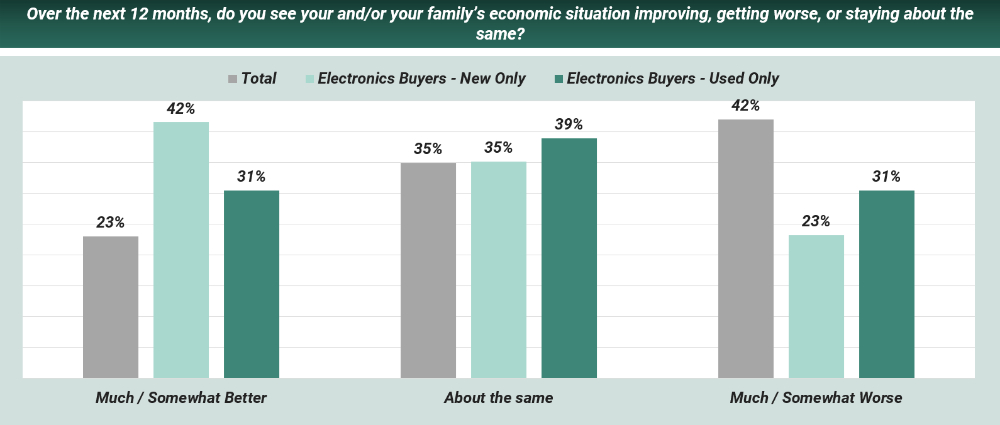

For those whose economic fortunes improved year-over-year, 78% believe that things will only get better over the next 12 months.

For those who are in an economic funk (e.g., experienced year-over-year worsening):

- 44% feel that things will get even worse over the next 12 months, more than 2X the survey average

- 35% expect no improvement

- And only 21% see things getting better in the next 12 months

In summary, the gloomy clouds of economic uncertainty and household financial pain are not expected to clear over the next 12 months for a majority of our BTS respondents.

Beyond the Big-Box: Alternative Retailers in the BTS Landscape

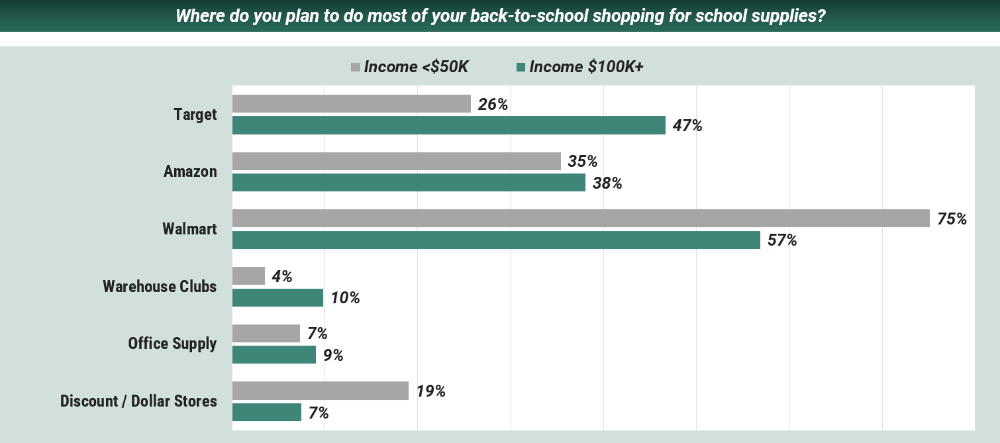

Although economic uncertainty lingers in the minds of most BTS shoppers, household income significantly influences their choice of shopping destinations. That said, virtually all BTS survey respondents plan to visit Walmart, either in-person or online. Joining Walmart, albeit at less frequency, are Target and Amazon. While these retailers top the "go-to" list for most shoppers, we highlight some additional destinations that may turn the ordinary BTS checklist into a multi-store and format journey.

Lower-Income Shoppers

Those with a household income of <$50K have an overwhelming preference for Walmart for both BTS supplies (75% of respondents) and for clothing, accessories, and footwear (48%). Outside of the big boxes, respondents also look to Discount and Dollar stores for school supplies (19%), and thrift stores for clothing, accessories, and footwear (11%) which is not as prevalent in higher-income respondents.

Walmart's strong positioning may be rooted in their broad, multi-category assortment. According to DriveResearch, 56% of shoppers turn to mass merchandisers for their groceries (about 60% of Walmart's sales according to the last 10-Q), so it is understandable why busy parents may elect to pick up new pencils and trendy shoes at their one-stop-shop during this time of year.

Higher-Income Shoppers

While Walmart is still on the go-to list for those with

household incomes >$100K, other retailers prove important. In

shopping for clothing, accessories, and footwear, higher-income

shoppers look to Target (35%), Amazon (31%), and Walmart (30%) to

fill their carts, along with a high penetration of shoppers looking

to Specialty stores (26%) and Department stores (24%). In the hunt

for school supplies, while the majority look to Walmart (57%), we

see strong competition from Target (47%) and Amazon (38%), as well

as a higher preference for Warehouse Clubs than that of

lower-income households.

Along with big-box Goliaths, it is important to not overlook the niche specialty and department store experiences that higher-income consumers value this time of year. According to our survey, 79% of all respondents are likely to compare prices across multiple retailers before making a BTS purchase, reflected in the wide net that we see shoppers cast for their BTS shopping journey.

Our survey highlighted a growing popularity of Warehouse Clubs for school supplies and clothing. This traffic growth underscores how financial uncertainty is impacting consumer preferences, and the hunt for value, price, and convenience presents opportunities for all retailers. While online giants are cited frequently, a trip to a physical store remains an important stop along the BTS shopping journey.

|

BTS Electronics Shoppers: A Case Study in Consumer Sentiment and Pricing The sentiments of electronics shoppers mirror the broader population but present interesting nuance based on current attitudes and sentiments regarding the economy. Approximately 20% of our survey respondents plan on purchasing electronics for BTS. Among these shoppers:

|

Our survey respondents who are opting to purchase used/Certified Pre-Owned electronics in 2024 are markedly more pessimistic about both the U.S. economy and their personal financial situations. They are also less optimistic about improvement over the next 12 months

Making the Most of a Landscape Where Consumers Do Not Expect Economic Fortunes to Change Over the Next 12 Months

The 2024 BTS shopping season presents a multifaceted picture of economic resilience and consumer adaptation amidst challenging economic conditions. To navigate this landscape effectively, retailers must understand and respond to the evolving needs of consumers by prioritizing competitive pricing and promotional strategies. Given the heightened sensitivity to inflation and living costs, competitive pricing and strategic promotions are crucial. Retailers should:

- Offer discounts and deals that cater to budget-conscious shoppers

- Implement loyalty programs / systematically pull promotional levers on existing programs to retain customers and encourage repeat purchases

- Developing targeted marketing campaigns that address the specific concerns and aspirations of different consumer segments

- Leverage social media and digital marketing to engage with consumers and drive traffic to both physical and online stores

- Tailor promotions based on consumer purchasing behaviors and preferences across the bifurcated landscape

Conclusion

As we conclude this initial exploration of our BTS shopping survey findings, it is clear that navigating the current economic landscape requires more than just traditional strategies. Looking ahead, we will delve into how the drive for personalization and the concept that "loyalty begins with the retailer, not the shopper" can redefine consumer relationships and drive success in this shifting market. Stay tuned as we explore these emerging themes and their implications for retailers in our upcoming updates.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.