Understanding what happens in a balance-sheet dispute—how to prepare for—and navigate the process.

In my prior article demystifying post-closing statements, I introduced the concept of the post-closing balance sheet adjustment and highlighted key deal characteristics that can increase the likelihood of potential disagreements after closing. Once the ink on the deal is dry, it's time for the parties to work through the agreement and determine the amount of any purchase price adjustments. In this article, we'll go deeper into this phase.

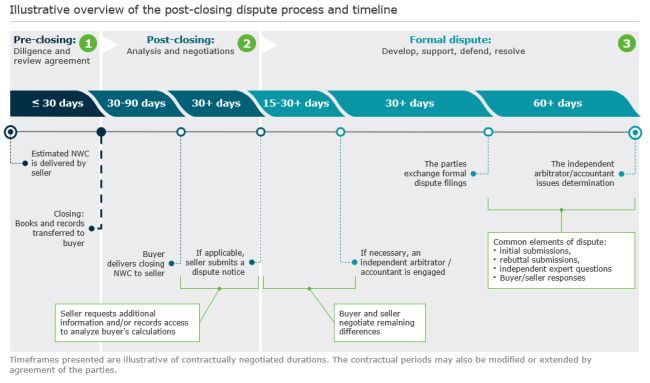

What does the post-closing process look like?

While purchase agreements and their related post-closing language are unique, the process to determine the final net working capital ("NWC") adjustment—sometimes referred to as a "true-up"—follows a common pattern and cadence.

The process typically begins (1) a few days prior to closing, when the seller provides a final estimate of the closing balance sheet. For example, if a deal is closing on December 31, the purchase agreement may require the seller to deliver an estimated closing statement on approximately December 28. The balance sheet will contain details for items like net working capital, cash on hand, transaction expenses, and debt, depending on the relevant deal metrics.

After closing (2), the buyer typically takes ownership of the accounting records. Purchase agreements frequently provide the buyer with a discrete amount of time (usually between 30 and 90 days) to examine business records and deliver a calculation of the final balance sheet at the closing date.

Following the buyer's submission of the closing balance sheet, the seller is provided with a set amount of time to review the buyer's calculations (again, often 30 days or longer). Depending on the purchase agreement terms, the seller is sometimes also able to request additional information or access to more detailed accounting records. If the seller does not identify any discrepancies (or does not respond within the allotted timeframe), the parties will confirm the final deal price and the post-closing balance sheet process will conclude at this stage.

However, the seller can also respond with a formal counter to the buyer's closing balance sheet (a "dispute notice"), which results in a fresh round of negotiations.

Resolving a post-closing balance sheet dispute

If the parties cannot agree upon the final closing balance sheet, the purchase agreement consideration remains up in the air. It's time to buckle up for round two of negotiations (3), which is likely to be more contentious as nerves fray, pressure mounts, and the risk of miscommunication and distrust increases.

Purchase agreements are highly bespoke and heavily negotiated agreements, and the language related to the resolution of post-closing accounting disputes is no exception. The following sections cover common elements for coming to an ultimate resolution.

Use of private arbitration and a neutral expert to resolve the dispute

A central characteristic of a post-closing balance sheet dispute is the selection of, and reliance upon, a neutral expert to decide the outcome of the parties' disagreements. The nomenclature used to describe this role in a purchase agreement varies (possible terms include independent accountant, accounting firm, accounting expert, arbitration firm, neutral accountant, etc.). These roles function in the same general capacity, though there are certain legal distinctions not addressed here.

Because balance-sheet disputes often revolve around complex and/or nuanced technical accounting issues, the neutral role is not usually filled by a judge, jury, or panel of attorneys. Rather, the parties negotiate to agree on a partner or firm with accounting and financial expertise to resolve the remaining disputed issues between the parties.

The selection of the neutral expert may itself represent a new negotiation. While some purchase agreements specify a certain firm to serve in this role, parties often find the selection more difficult in practice when parties uncover previously unknown or potential conflicts of interest between the named firm and either the buyer or the seller. For this reason, the buyer and seller should come prepared with a list of experts with requisite experience to confidently select a neutral for resolving their post-closing disputes.

Iterative exchange of positions and timing

Selecting the neutral expert is the first step, as the buyer and seller also need to lay out the structure of the process for resolving post-closing balance sheet differences. This step frequently occurs in tandem with the appointment of the neutral expert and specifies the format and structure the parties are expected to provide in support of their respective calculations.

During this process, the buyer, seller, and neutral expert will set out the following areas:

- The overall timelines for the dispute. This includes details such as when the process will start and how much time will elapse between the parties' various submissions to the neutral expert.

- The format of information to be provided to the neutral expert. For example, the parties may file letters, briefs, and/or expert reports in connection with accounting analyses or the process may include oral arguments and interviews.

- The number and cadence of the submissions. Commonly, both the buyer and seller can provide two position statements (whether an initial statement, response, or rebuttal to the other side's position statement). The parties may decide to provide their submission sequentially (i.e., one party first, then the other) or simultaneously.

- Whether an in-person hearing will take place or not and, if so, the format and parameters for the hearing.

The process of selecting a neutral expert and outlining the dispute framework can be time-consuming and result in a negotiated proceeding as unique as the purchase agreement itself.

Start the process before the sale

Typically, neither buyers nor sellers look forward to a post-closing dispute during deal negotiations. However, starting early with the right team—while keeping an eye toward the potential post-closing application of the purchase agreement—can maximize the value of deal diligence and preparation. This preparatory work will help you avoid a protracted conflict at the worst possible time or, should one occur, put you in the best possible position to charter your way through it.

Solid preparation means starting discussions early on. To get under the hood and really understand the relevant accounting practices, parties should allow time for robust due diligence. Before the sale, parties need to determine key accounts, and establish agreed-upon measurements and clear definitions that align with strategic priorities. For example, does one party prefer certainty of value at the expense of potential upside? This may be reflected in the decision to use a "target" or "peg" value, as opposed to a figure derived from interim or estimated financial statements.

Assemble your dream team. This is when the team who will take the company through closing negotiations should take shape. That means bringing on accounting advisors with dispute experience alongside existing deal teams, finance and accounting professionals and legal teams.

Documentation is worth its weight in gold. Potential red flags can be identified, along with the nuts and bolts of the transaction that could later become contentious. Some of the specifics to capture include:

- Listing the financial statement accounts to be included or excluded from the calculation of the closing balance sheet and relevant net working capital calculations—address the nuance and relationship (or lack thereof) within the target amount and post-closing balance sheet. This may include the use of an example calculation or a detailed exhibit outlining the format, contents, and trial balance-level accounts to be included in the calculation.

- The methodology for estimating key accounts (significant estimates or assumptions).

- The hierarchy of accounting frameworks when sorting through how to treat certain transactions or practices. Importantly, the language should address the priority between generally accepted accounting principles (GAAP)/International Financial Reporting Standards (IFRS) and the consistent application of accounting practices used by the target prior to closing.

- The format, structure, and timing of the buyer's closing balance sheet and the seller's dispute notice communications—address the level of support to be provided and the detail in which potential adjustments need to be disclosed.

- Guidance on how disputed calculations are to be decided by the neutral expert—should the decision be limited to only a decision between the buyer or seller positions (often referred to as "baseball arbitration"), is the neutral expert able to determine an amount within the range of the buyer and seller positions, or is the neutral expert able to calculate any number deemed to be correct under the purchase agreement?

Consistency is key. Aim for consistency between closing mechanisms, if applicable (i.e., net debt and net working capital), and with other provisions, such as indemnifications provided under the purchase agreement.

The team charged with preparing for and managing deal negotiations will track all the moving pieces that generate value and liability. Having these keys top of mind during the early legwork on closing statement language provides solid ground from which to adjust the framework for calculating the final balance sheet. In the end, effective preparation and diligence will keep you from spinning your wheels in place and get the deal moving.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.