Diversifying strategies – lessons from success on the football pitch

Constructing a well-rounded portfolio is like assembling a winning football team: it means selecting the right combination of individual talents and then managing them to meet the challenges of the day.

Today, investors are need to think harder about their starting line-up. On one hand, they face more global market risks and uncertainties than ever before. On the other, diversifiers such as the once-reliable negative correlation between bonds and equities can no longer be taken for granted.

In our view, liquid diversifiers play a crucial role in building a portfolio that can help navigate uncertain markets via a variety of strategies with unique characteristics. Investors require a team of these strategies, each playing their individual role to create a robust and resilient portfolio.

Liquid diversifiers offer a range of strategies that seek to provide returns that are uncorrelated with equities and bonds.

A team with complementary skill sets

We believe a well-rounded diversified portfolio needs a strong defense to provide stability in market downturns; an agile midfield that can respond decisively to changing market conditions; a proactive offense to add above-market returns and — bringing these elements together—an experienced team manager who is able to direct and rotate tactically in order to get the best out of the individual components of the team. An allocation to liquid diversifier strategies can achieve success in each of these areas, with the main aims being to mitigate risk, increase diversification and, importantly, generate alpha.

Defensive strategies help protect long-term return goals

Strategies that are negatively correlated with traditional asset markets can be a key line of defense in protecting a portfolio's return goal, providing a shield at times of uncertainty or market volatility. During market drawdowns, these strategies step up to provide positive return potential, helping to preserve capital and creating the ability to rebalance. In our view, their ability to navigate and capitalize on market dislocations can help investors maintain a more stable and consistent performance across changing market environments (Figure 2).

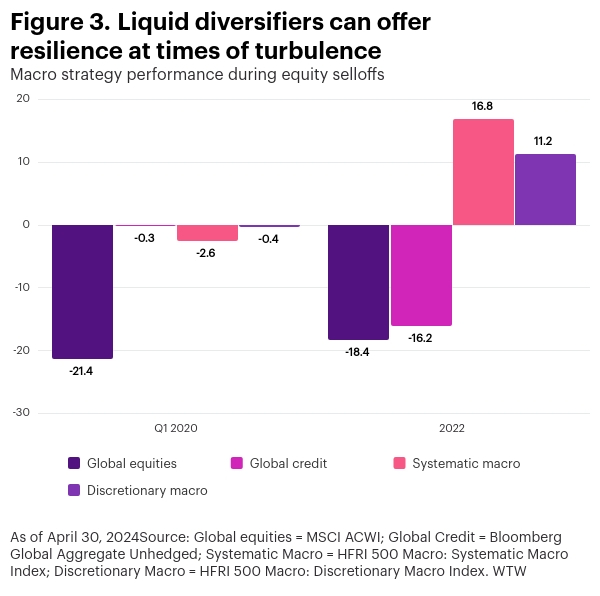

Figure 2. The defense lineup

| Systematic macro | Discretionary macro |

|---|---|

| Uses computer algorithms and quantitative models to make automated decisions based on predefined rules and macro data analysis. | Makes investment decisions based on macroeconomic analysis and manager views. Key elements include macro analysis, a top-down approach, flexible portfolio allocation and discretionary decision making and risk management. |

| Typically performs well when economies and markets are trending strongly. | Typically performs well at times of increased market volatility and economic turning points such as elections, policy uncertainty and heightened geopolitical risk. |

Figure 3 shows the historical resilience of macro strategies during the Covid-19 shock in the first quarter of 2020 and again during the simultaneous equity and bond market selloffs in 2022. Over both periods, the liquid diversifier strategies were able to generate alpha and provide significant downside protection (Figure 3).

'Midfield' strategies can add versatility

Midfield players are versatile and adaptable. They may hold their ground in the center of the field or follow the flow of the game from end to end. You could argue that uncorrelated liquid diversifying strategies are the midfield players of the alternatives world. For example, insurance-linked securities typically hold their ground, collecting premia to deliver returns while the market moves around them. By contrast, alternative beta strategies act as the fast-moving "winger," following the flow of markets in search of opportunities to capture returns (Figure 4).

Figure 4. The midfield lineup

| Insurance-linked securities | Alternative risk premia |

|---|---|

| Invests in instruments tied to insurance risks, such as catastrophe bonds or reinsurance contracts. | Takes exposure to different risk premia or factors beyond traditional market indices, such as volatility, carry and momentum. May include unique strategies such as merger arbitrage and carbon credits, which can be allocated to when opportunities occur. |

| Tends to perform best during periods of low catastrophic events, as this reduces the likelihood of insurance payouts and allows investors to benefit from steady coupon payments and principal preservation on catastrophe bonds. Return potential from active allocation also tends to be affected by supply and demand dynamics. | Tends to perform best during market dislocations or periods of heightened volatility. These events can create pricing inefficiencies and opportunities for systematic strategies to capture alternative risk premia. |

In their different ways, these strategies can help provide a consistent source of returns over time, irrespective of broader market conditions.

Insurance-linked securities (ILS) such as catastrophe bonds are a growing asset class that can provide strong, reliable return potential, particularly on a risk-adjusted basis, while remaining uncorrelated with global equities. As shown in Figure 5, "cat bonds" have outperformed equities and credit on a risk-adjusted basis for the past several years. For equity investors in particular, cat bonds have offered good diversification properties, with a beta to equities of less than 0.2 since 2018. [1]

Figure 5. Inflation-linked securities have offered an attractive risk-return trade-off Comparing Sharpe ratios of ILS, equity and credit indices

*Risk-free rate used in Sharpe ratio calculation is the Ice BofAML three-month Treasury bill.Notes: ILS = SwissRe Cat Bond Index; Equity = MSCI ACWI; Credit = Bloomberg Global Aggregate Unhedged.Source: eVestment, Bloomberg. Data as of December 31, 2023.

| ILS | Equity | Credit | ||

|---|---|---|---|---|

| Sharpe ratio* | 1 year | 10.3 | 1.1 | 0.1 |

| 3 years | 0.9 | 0.2 | –0.9 | |

| 5 years | 0.9 | 0.6 | –0.3 |

'Offense' pushes for extra performance

Offensive players, often the focal point of a football team, tend to be the goal scorers and creators of scoring chances. In the world of liquid diversifiers, the offensive players include directional, higher-octane strategies that seek to generate alpha. For example, long-short fund managers will take high-conviction views, seeking to profit from some aspect of emerging themes, companies and overall market dynamics (figure 6). Incorporating these more aggressive players into a portfolio of liquid diversifiers can help meet long-term goals by providing a boost to returns.

Figure 6. The offensive lineup

| Equity long-short | Credit long-short |

|---|---|

| Relies on stock pickers' assessment of whether a company's stock is over- or undervalued. May use leverage to increase exposure. Styles vary, e.g. generalist-focused vs. sector-focused and global vs. regional. Thematic views may be incorporated, such as artificial intelligence, the clean energy transition and emerging markets. | Takes positions in credit instruments such as bonds, loans and other debt securities. Managers analyze credit markets to identify opportunities for buying potentially undervalued or improving credit instruments and for selling potentially overvalued instruments. |

| Tends to perform best during market dislocations or corrections when stock prices and valuations diverge and managers can seek to exploit pricing anomalies. This may include periods of company-specific events, such as earnings surprises, mergers and acquisitions, or other catalysts that can drive return potential. | Tends to perform best during positive credit environments as bond prices rise and credit spreads tighten. Stable or declining interest rates can be favorable for credit hedge funds. Lower interest rates tend to boost the prices of existing bonds, and credit spreads may narrow, contributing to capital appreciation. |

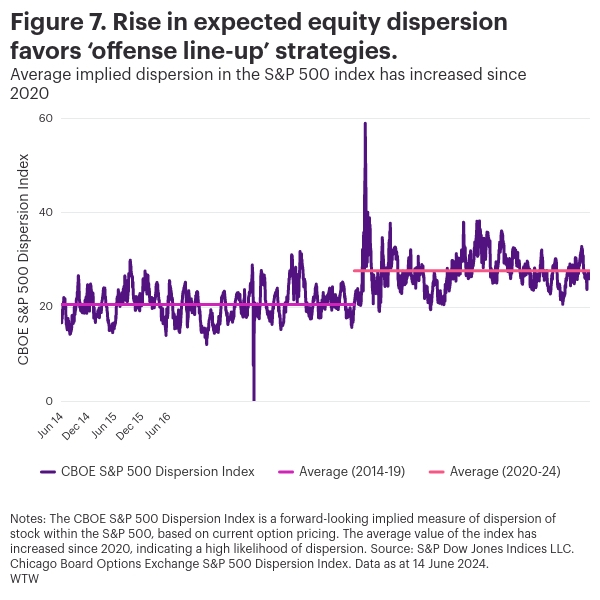

Active long-short strategies tend to benefit from high dispersion in asset prices, which creates opportunities for long-short managers to profit from mispricing. In this respect, Figure 7 shows that conditions have become more favorable for equity long-short managers since 2020.

Selecting the right manager

A successful team needs optionality at the transfer window. Portfolio construction should aim to consider every eventuality, including remaining highly liquid to provide flexibility without sacrificing diversity—something we think liquid diversifiers are well equipped to do.

It's important to note that, while the diversification benefits and uncorrelated nature of liquid diversifiers can make them a compelling investment opportunity, they are not immune to risks and investors can experience losses. A sound and systematic approach is therefore needed to monitor and manage leverage, left-tail risk and manager selection risk.

WTW has managed liquid diversifier strategies since 2007, selecting managers and constructing portfolios to help our clients meet their investment objectives. Contact us to understand how we can help you achieve your portfolio goals.

Footnote

1 Beta refers to the volatility of an asset's returns versus the volatility of a broader market. In this case we looked at rolling 3-year beta of ILS to equities where ILS = SwissRe Cat Bond Index and equities = MSCI ACWI.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.