- within Strategy, Insolvency/Bankruptcy/Re-Structuring and Family and Matrimonial topic(s)

- with Senior Company Executives, HR and Inhouse Counsel

- with readers working within the Accounting & Consultancy and Law Firm industries

INTRODUCTION

Corporate regulation reveals its sharpest edges when the law maps traditional concepts of ownership onto modern, borderless multinational enterprises. This tension peaks even without fraud or concealment. Modern multinational enterprises operate through deeply layered holding structures, professional boards, and dispersed management teams. Consequently, tracking the individual exercising ultimate 'control' over an Indian subsidiary is no longer a straightforward exercise. This tracking becomes highly contentious when regulators bypass shareholding records or contractual rights. Instead, they infer control from internal governance practices, cross-border executive hierarchies, and public disclosures.

Accordingly, the proceedings in LinkedIn Technology Information Private Limited & Ors. v. Union of India & Ors. (W.P.(C) 6677/2026) assume considerable significance. On May 15, 2026, the Hon’ble Delhi High Court granted interim stay of the impugned orders passed by the Registrar of Companies (“ROC”) and the Regional Director. These impugned orders had penalized the petitioners under Sections 89 and 90 of the Companies Act, 2013 (“Act”).

Though interim, the order has already drawn two enduring questions in Indian corporate law: (i) how far the significant beneficial ownership ("SBO") framework can extend in tracing “control” through multinational corporate chains; and (ii) how far a regulatory authority may legitimately stretch its investigative and interpretive reach before crossing into the territory of jurisdictional overreach.

The controversy traces back to an order dated May 22, 2024, in which the ROC concluded that the Chief Executive Officer (“CEO”) of Microsoft Corporation (Mr. Satya Nadella) and the CEO of LinkedIn Corporation (Mr. Ryan Roslansky)qualified as SBOs of an Indian private limited company situated several layers below them in the ownership chain. What makes the matter particularly striking is that the finding was not founded on direct shareholding, voting rights, shareholder agreements, or formally documented powers of control. Instead, the ROC relied upon an assortment of foreign corporate governance materials, including filings made before the United States Securities and Exchange Commission ("SEC"), Microsoft Corporation’s bylaws filed with the SEC, and descriptions appearing on LinkedIn Corporation’s own website, to infer the existence of “significant influence” and “control” over the Indian entity.

If upheld, this functional approach will materially expand India’s SBO regime by permitting regulators to identify beneficial ownership through global executive authority and operational influence rather than traditional proprietary thresholds. For multinational corporations (“MNC(s)”), this introduces acute compliance unpredictability and subjects borderless, matrix-managed governance structures to intense extraterritorial scrutiny. Modern MNCs rely on diffused global leadership rather than linear ownership hierarchies, and statutory mechanisms under Section 90 and the Companies (Significant Beneficial Owners) Rules, 2018 (“SBO Rules”), originally designed to pierce opaque shell structures, are now being stretched beyond those legitimate management realities.

While the Delhi High Court’s interim stay is not a final resolution, it signals a clear judicial willingness to scrutinize the ROC’s expansive reasoning and offers a timely opportunity to define the framework's jurisdictional limits where legal title and functional control diverge. The eventual writ ruling will therefore carry consequences well beyond the immediate parties, definitively shaping the interpretation of Sections 89 and 90 of the Act, and rebalancing domestic regulatory enforcement against international corporate governance.

THE PARTIES AND THE CORPORATE STRUCTURE

The dispute before the Delhi High Court arises from the corporate structure and ownership disclosures of LinkedIn Technology Information Private Limited ("LinkedIn India"), an Indian subsidiary operating within the larger Microsoft group. Incorporated on December 31, 2009 under the Act, LinkedIn India has its registered office in New Delhi and is principally engaged in technology services, including substantial research and development operations.

For F.Y. 2022–23, LinkedIn India reported operational revenues of approximately INR 18,314 million. It employed nearly 477 personnel within its R&D division alone. These figures reflect the significant scale of LinkedIn India's operations within the broader Microsoft group.

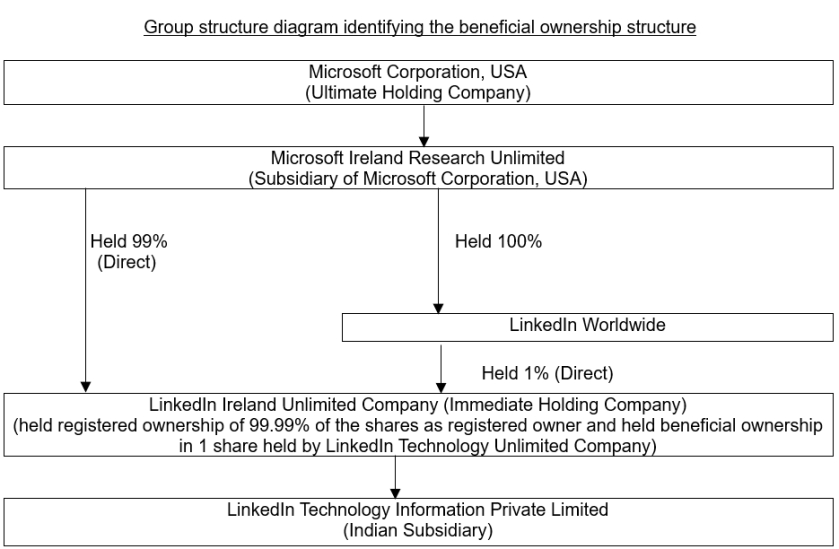

At the outset, the ownership structure disclosed by LinkedIn India appeared relatively straightforward, though layered across multiple jurisdictions in a manner typical of large multinational enterprises. LinkedIn India stated that its immediate holding company was LinkedIn Ireland Unlimited Company, incorporated in Ireland. That entity, in turn, was held 99% by Microsoft Ireland Research Unlimited Company and 1% by LinkedIn Worldwide Research Unlimited Company, both incorporated in Ireland. The chain routed through two Isle of Man upstream entities: LinkedIn Worldwide and LinkedIn International. The structure ultimately culminated in Microsoft Corporation, USA, designated as the group's ultimate holding company.

LinkedIn India consistently maintained that no individual qualified as an SBO under Section 90 or the SBO Rules. Because Microsoft Corporation's public shareholding is widely dispersed, no single natural person meets the 10% threshold.

The company’s position rested substantially on the fact that Microsoft Corporation is a globally listed corporation with widely dispersed shareholding, and that no natural person held, directly or indirectly, 10% or more of its shares, voting rights, or distributable dividend entitlements. According to the petitioners, the statutory framework was therefore incapable of tracing beneficial ownership to any identifiable natural person within the group. However, it was precisely within this seemingly settled ownership narrative that the controversy emerged.

A core conflict arose from the financial statements. While disclosures by LinkedIn India had listed Microsoft Corporation as the ultimate holding company, its financial statements had historically referred to LinkedIn Corporation, USA as its "holding company." Importantly, however, LinkedIn Corporation did not appear within the formal ownership chain separately disclosed before the ROC. This apparent divergence between the legal ownership structure and the operationally acknowledged corporate relationship became a focal point of the ROC’s inquiry. For the ROC, the discrepancy appeared to suggest that the formal chain alone did not adequately capture the actual locus of influence and control within the group structure.

The proceedings that followed ultimately resulted in the ROC passing an order dated May 22, 2024, holding that senior executives within the Microsoft and LinkedIn corporate hierarchy qualified as SBOs of LinkedIn India.

Challenging this determination, LinkedIn India and other affected parties, including certain individual officers, approached the Hon'ble Delhi High Court under Article 226 of the Constitution of India.

The dispute thus moved beyond a routine compliance inquiry and evolved into a broader contest over the meaning of beneficial ownership, the evidentiary limits of regulatory inference, and the extent to which Indian authorities may rely upon foreign corporate governance materials to attribute "control" within complex multinational structures.

THE ROC PROCEEDINGS

The Section 89 Dispute: Clerical Error v. Substantive Default

The proceedings before the ROC were initiated following the filing of e-Form MGT-6 by LinkedIn India on January 29, 2024. Through this filing, the company disclosed LinkedIn Technology Unlimited Company as the registered holder and LinkedIn Ireland Unlimited Company as the beneficial owner of 1 equity share, while stating January 11, 2024 as the date of creation of the beneficial interest.

Upon examining the company’s financial statements for F.Y. 2022–23 and prior years, however, the ROC observed that the beneficial interest had been reflected in the books for several years, including in connection with the 2014 amalgamation involving Uzanto Consulting India Private Limited. According to the ROC, the disclosed beneficial interest therefore predated the date mentioned in e-Form MGT-6 by a considerable margin.

LinkedIn India explained that the date had been incorrectly mentioned due to a clerical error and represented the date on which the declaration forms were submitted rather than the actual date on which the beneficial interest had arisen. The ROC, acting in its capacity as Adjudicating Officer under Section 454(1) of the Act read with the Companies (Adjudication of Penalties) Rules, 2014, did not treat this explanation as sufficient to cure the default. By order dated May 22, 2024, penalties under Section 89(5) of the Act were imposed on LinkedIn Technology Unlimited Company, as the registered owner, and LinkedIn Ireland Unlimited Company, as the beneficial owner. The penalties were computed over 1,152 days of default and quantified at INR 2,80,400 each, subject to the statutory cap of INR 5,00,000.

Significantly, the existence of the beneficial ownership structure itself does not appear to have been disputed by the Microsoft group entities. The company admitted before the ROC that the date of creation of beneficial interest had been erroneously stated in the e-Form MGT-6 form and that the Section 89 of the Act declarations had not been filed within the applicable timelines. While the petitioners' legal arguments during the ROC proceedings were concentrated primarily on contesting the Section 90 of the Act relating to the findings regarding the identification of SBOs, the writ petition filed before the Delhi High Court challenges both the Section 89 and Section 90 penalty orders in their entirety. The High Court's interim stay operates against both.

The Section 90 Inquiry: Shifting to Functional Control

The more significant and legally contentious aspect of the proceedings concerned Section 90 of the Act and the identification of SBOs of LinkedIn India.

As stated above, throughout the proceedings, LinkedIn India maintained a consistent position that Microsoft Corporation, its ultimate holding company, is a widely held publicly listed company in the United States with no individual shareholder holding 10% or more of its shares, voting rights, or distributable dividend entitlements. According to the company, there was therefore no natural person who could satisfy any limb of the SBO definition under the Act or the SBO Rules. LinkedIn India further stated that it had never received any declaration under Section 90(1), had not filed e-Form BEN-2, and had no reason to believe that any individual qualified as an SBO of the company.

In a stark departure from traditional asset-ownership testing, the ROC widened its net. A key factor that drew the ROC's attention was the fact that LinkedIn India's financial statements continued to describe LinkedIn Corporation, USA as its "holding company," even though LinkedIn Corporation did not separately appear in the ownership chain formally disclosed before the ROC. Proceeding on the basis that a holding company relationship necessarily implied the ability to control the composition of the Board of Directors, the ROC sought to identify the individuals through whom such control was ultimately exercised.

For this purpose, the ROC relied upon publicly available foreign corporate governance materials, including the bylaws of LinkedIn Corporation and Microsoft Corporation filed with the SEC, as well as disclosures available on LinkedIn Corporation's website. The ROC noted that LinkedIn's website described Mr. Ryan Roslansky as the "leader" of LinkedIn Corporation and further stated that he reported to Mr. Satya Nadella as part of Microsoft's senior leadership team. The ROC also examined Microsoft Corporation's bylaws, which vested the CEO with general charge and supervision of the business of the corporation. Mr. Satya Nadella held a dual role as CEO and Chairman of Microsoft Corporation. Based on this, the ROC concluded that he exercised overarching, de facto control across the entire global group.

On the basis of this analysis, the ROC concluded that both Mr. Satya Nadella and Mr. Ryan Roslansky qualified as SBOs of LinkedIn India under Section 90 of the Act, notwithstanding the absence of direct shareholding or any formally documented rights of control over the Indian entity. Penalties were accordingly imposed under Section 90(10), with INR 2,00,000 each levied on Mr. Nadella and Mr. Roslansky, while LinkedIn India and its directors were subjected to additional penalties under Sections 90 and 450 of the Act, each capped at the applicable statutory maximum.

It is this aspect of the ROC's reasoning that lies at the core of the jurisdictional and interpretive controversy now pending before the Delhi High Court. The case raises an important question: whether the concept of "control" under the SBO framework can be inferred from executive roles, reporting structures, and foreign governance documents of multinational corporations, even in the absence of demonstrable legal ownership rights or direct authority over the Indian company.

Key Grounds of Challenge by the Petitioner

In challenging the ROC's findings under Section 90, LinkedIn India advanced a series of arguments that went beyond the facts of the case and struck at the conceptual foundation of the SBO framework when applied to professionally managed multinational corporations. At the heart of its case was the principle of separate corporate personality.

Relying on Vodafone International Holdings B.V. v. Union of India [1] , LinkedIn India invoked the principle of separate corporate personality. A holding company and its subsidiary remain distinct legal entities entitled to decentralized management. The company also referred to the Delhi High Court's earlier observations cautioning against treating subsidiary directors as mere "puppets on a string" acting at the command of an invisible holding company. LinkedIn India maintained that its Board functioned independently and that no person situated higher in the Microsoft or LinkedIn corporate hierarchy issued directions to the Board of the Indian company.

A second and more fundamental argument concerned the very source of "control" or "significant influence" under the Act. The petitioner argued that executive reporting lines cannot establish 'control.' Legally recognized control must spring from an explicit source, such as a statute, shareholder agreement, or charter document." This requires a grounding statute, shareholder agreement, or charter document. The company pointed out that e-Form BEN-2 itself requires disclosure of the agreement or document through which such control is exercised, demonstrating that the statutory framework contemplates a documentary basis for identifying an SBO. Applying this reasoning specifically to Mr. Ryan Roslansky, LinkedIn India emphasized that there existed no agreement, resolution, instrument, or corporate document granting him any authority over LinkedIn India's affairs. He had never served as a director of LinkedIn India, had never attended its Board meetings, held no shares in the company, and possessed no formal or recognized right to influence its financial or policy decisions.

LinkedIn India further argued that the Act refers to the designation of "chief executive officer" only in the limited context of pooled investment vehicles, suggesting that Parliament deliberately chose not to automatically treat CEOs of ordinary corporations as SBOs.

The company also questioned the broader implications of the ROC's interpretation. Referring to the Report of the Company Law Committee, 2016 [2] , LinkedIn India argued that the SBO framework was introduced primarily to identify natural persons hiding behind opaque structures used for tax evasion, money laundering, or illicit control. Weaponizing the SBO framework against a professional executive whose authority is tethered to board oversight perverts the legislative intent of Section 90. The framework was enacted to pierce opaque shell structures shielding illicit wealth, not to upend standard, globally accepted matrix-management models. It highlighted that Microsoft Corporation and LinkedIn Corporation are not promoter driven entities but globally listed and professionally managed corporations, similar in structure to many Indian banking and technology companies.

LinkedIn India also strongly objected to the ROC's reliance on foreign corporate governance materials. It argued that it had no control over or access to the internal governance documents of LinkedIn Corporation, which was not even its direct shareholder in the disclosed ownership chain. In any event, the company submitted that the bylaws of Microsoft Corporation and LinkedIn Corporation themselves placed the CEO under the supervision and control of the Board, making it difficult to infer independent authority amounting to "control" under Indian law. The company stressed that foreign corporate bylaws could not override the statutory scheme of the Act.

The Petitioners advanced a further foundational challenge to the very characterization of executive authority adopted by the ROC. The ROC failed to appreciate the fundamental distinction between proprietary control and managerial agency. A CEO or board chairperson of a listed multinational corporation may exercise extensive administrative authority over the day-to-day affairs of the enterprise. However, such authority is neither inherent nor autonomous; it is entirely derivative, delegated, and contingent upon the mandate conferred by the board of directors. A corporate executive functions within the framework of an employment or service arrangement and remains accountable to, and removable by, the Board and ultimately the shareholders. The same governance structure that vests an executive with operational authority simultaneously subjects that authority to continuous oversight and revocation. Upon termination of the executive's appointment, such authority ceases immediately.

This inherently precarious and revocable position stands in stark contrast to the stable, independent, and legally enforceable rights that constitute "control" within the meaning of Section 90 of the Act and Rule 2(1)(h) of the SBO Rules. By treating managerial authority as synonymous with statutory control, the ROC committed a fundamental error of law. Authority that is merely contractual, conditional, delegated, and revocable cannot be equated with control over an enterprise. A fortiori, such authority cannot be attributed across multiple layers of corporate ownership so as to establish control over an independent Indian subsidiary situated further down the corporate chain.

Finally, LinkedIn India drew support from comparative international practice. It referred to guidance issued under the United Kingdom Companies Act, 2006, which clarifies that employees, directors, or CEOs of a third party are not regarded as exercising significant influence or control merely by virtue of their office. Similar submissions were also made with reference to the United States Corporate Transparency Act, reinforcing the argument that modern beneficial ownership regimes generally distinguish between professional management and actual beneficial ownership or control.

The Evidentiary Matrix Relied Upon by the ROC

Several aspects of the ROC's methodology stand out in the proceedings, not merely because of the conclusions ultimately reached, but because of the manner in which the inquiry itself was conducted.

To begin with, the ROC did not rely solely on information furnished by LinkedIn India. Instead, it independently accessed publicly available filings made before the SEC, including the bylaws of LinkedIn Corporation and Microsoft Corporation. Since LinkedIn India stated that it did not possess or control the internal governance documents of LinkedIn Corporation, the ROC sourced these materials directly from foreign public records and used them as a foundation for its analysis. From the LinkedIn Corporation bylaws and LinkedIn's own website, the ROC identified Mr. Ryan Roslansky as the "leader" of LinkedIn and treated his reporting relationship with Mr. Satya Nadella as indicative of a broader chain of control within the corporate structure.

The ROC adopted a similar line of reasoning in relation to Microsoft Corporation. Relying upon Microsoft's bylaws filed with the SEC, the ROC noted that the CEO was vested with the general charge and supervision of the corporation's business and affairs. On this basis, it anchored its finding of "significant influence" on Mr. Satya Nadella's dual capacity as CEO and chairman of the board. In doing so, the ROC conflated executive management with legal control, treating administrative authority and board leadership as sufficient indicia of statutory influence over the Indian company.

This reasoning is conceptually and legally unsustainable. A CEO or board chair, irrespective of the breadth of his operational responsibilities, ordinarily exercises authority that is delegated, fiduciary, and subject to continuous oversight by the board of directors and, ultimately, the shareholders of a listed corporation. Such authority is neither proprietary nor independent; it exists only for so long as the executive retains the confidence of the governing body that appointed him. The powers attached to the office are therefore contractual and revocable, rather than constituting legally enforceable rights of control over the enterprise.

By equating managerial authority with statutory control, the ROC disregarded the distinction between corporate governance and ownership-based influence embedded in the SBO framework. The mere fact that an executive occupies a senior leadership position cannot, without more, establish the legal right to exercise control or significant influence within the meaning of Section 90 of the Act and Rule 2(1)(h) of the SBO Rules. If such an approach were accepted, every professionally managed multinational corporation would face the prospect of its senior executives being treated as SBOs of each subsidiary within its global corporate structure solely by virtue of their office. Such a result would not only be inconsistent with established principles of company law but would also distort the legislative purpose of the SBO regime, which is directed at identifying natural persons possessing ultimate ownership rights or genuine controlling influence, rather than professional managers acting under delegated authority.

The ROC also examined the internal governance documents of LinkedIn India itself. Specific attention was drawn to Article 62 of the Articles of Association, particularly in relation to powers delegated for operation of the company's bank accounts. Certain authorizations extended to officers associated with Microsoft Corporation were viewed by the ROC as carrying significance beyond purely administrative convenience. LinkedIn India maintained that these arrangements were purely administrative in nature, but the ROC was not fully persuaded by that explanation.

Another factor relied upon by the ROC was the overlap of personnel across multiple entities in the ownership chain. The ROC flagged an overlap of management personnel. Two directors of LinkedIn India, Mr. Keith Ranger Dolliver and Mr. Benjamin Owen Orndorff, simultaneously held board positions in upstream Irish holding entities. The ROC additionally referred to SEC filings relating to earlier Microsoft acquisitions, where these individuals had reportedly been appointed to boards of acquired entities pursuant to merger arrangements granting Microsoft majority board representation. This was treated as part of a larger pattern demonstrating Microsoft's operational integration and influence across acquired businesses.

Finally, the ROC also referred to Mr. Ryan Roslansky's visit to LinkedIn India's Bengaluru office in November 2022 and his public remarks regarding the expansion of research and development operations in India. LinkedIn India responded that the visit was limited to customer engagement and internal interaction sessions, and that any public comments concerning expansion reflected general business optimism rather than formal instructions or control over the Indian company's Board. Nevertheless, the ROC considered these facts relevant while assessing the practical realities of influence and management within the group.

Taken together, these features reveal that the ROC's inquiry moved well beyond formal ownership records and entered the broader terrain of inferred managerial influence, operational integration, and governance structure analysis. Whether such material can legitimately form the basis for identifying SBOs under Indian law now lies at the centre of the challenge pending before the Delhi High Court.

The High Court's Intervention and Stay of Operation

Following the ROC's order of May 22, 2024, LinkedIn India carried the matter in appeal before the Regional Director, whose order dismissing the appeal was passed on February 27, 2026. LinkedIn India and the other petitioners then filed W.P.(C) 6677/2026 before the Delhi High Court under Article 226 of the Constitution of India, challenging both the ROC penalty order and the Regional Director's appellate order as the "impugned orders." On May 15, 2026, the matter came before Hon'ble Mr. Justice Anish Dayal.

The petitioners advanced two core arguments: (i) the ROC had gone beyond the scope of what falls within the ambit of declarations required under Sections 89 and 90 of the Act; and (ii) all petitioners had been improperly "roped in" to make declarations under Sections 89 and 90 of the Act.

After hearing the submissions advanced on behalf of the petitioners, the Delhi High Court considered the matter serious enough to issue notice to the respondents, who accepted notice before the Court. Importantly, the Court directed that the operation of both the ROC's order and the appellate order passed by the Regional Director would remain stayed until the next date of hearing, now scheduled for October 06, 2026. The respondents have been granted eight weeks to file their reply.

Although the interim order is concise, its significance should not be understated. At a preliminary stage itself, the Delhi High Court appears to have found sufficient substance in the petitioners' challenge to warrant protection against the operation of the impugned orders pending final adjudication. While the Court has not yet expressed any conclusive opinion on the merits, the grant of interim relief indicates that the issues raised are not merely procedural objections but involve substantial questions concerning the scope of the ROC’s authority under Sections 89 and 90 of the Act.

CONCLUSION

Since judgment on the merits of the writ petition remains pending and is listed for October 06, 2026, it would be premature to draw definitive conclusions. However, the following considerations emerge from the record:

(a) Adjudicatory Expansion Under Section 454 - What began as a proceeding relating to an alleged filing error under Section 89 gradually expanded into an extensive examination of the governance structure of foreign parent entities, foreign corporate bylaws, reporting hierarchies, and executive authority within the Microsoft group. The case therefore raises an important procedural question: whether there exists a limiting principle on the scope of an adjudication under Section 454 of the Act, particularly where proceedings evolve substantially beyond the subject matter originally set out in the show cause notice.

(b) Evidentiary Value of Foreign Disclosures - The ROC relied heavily on bylaws sourced from filings made before the SEC along with statements appearing on LinkedIn Corporation's website, to infer control and significant influence. This raises a broader issue as to whether Indian authorities may interpret concepts such as "control" and "significant influence" on the basis of foreign governance documents and public disclosures, and if so, what standards of evidence and procedural fairness should govern such an exercise.

(c) Requirement of a Documented and Traceable Legal Source - LinkedIn India consistently argued that the right to exercise control or significant influence must arise from a legally identifiable source such as a statute, agreement, charter document, or other enforceable instrument. The ROC, however, adopted a more functional approach based on practical influence, reporting structures, and managerial hierarchy. The final adjudication may therefore determine whether Section 90 targets legally enforceable control alone or also extends to inferred operational influence within multinational corporate structures.

(d) Whether the CEO of a professionally managed, widely held foreign corporation can qualify as an SBO of an Indian subsidiary – A central issue arising in the case is whether senior executives of globally listed and professionally managed corporations can be treated as SBOs despite the absence of direct shareholding, voting rights, or formally documented rights capable of influencing the affairs of the Indian entity. The resolution of this question could have far-reaching implications for Indian subsidiaries of multinational corporate groups, particularly where ownership is widely dispersed and no identifiable promoter or controlling shareholder exists.

At its core, the controversy requires a careful distinction between “power” and “control”. A CEO or board chair of a publicly listed corporation may exercise extensive authority over the day-to-day management and strategic direction of the enterprise. However, such authority is fundamentally managerial in nature. It derives from an employment or fiduciary relationship, remains subject to continuous oversight by the board of directors, and may be modified or withdrawn at any time in accordance with the company's governance framework. By contrast, the right to exercise "control" within the meaning of Rule 2(1)(h) of the SBO Rules contemplates a legally cognizable, independent, and enduring right, rather than a delegated authority that exists only for the duration of an executive appointment.

The ROC's approach, which treated the broad grant of supervisory powers under Microsoft's bylaws as sufficient to establish control over an Indian subsidiary, appears to blur this critical distinction. By equating executive authority with statutory control, the ROC risks extending the SBO framework beyond its intended purpose of identifying individuals who possess ultimate ownership rights or genuine controlling influence. The eventual ruling may therefore provide important guidance on whether professional managers of widely held multinational corporations can be regarded as SBOs solely by virtue of the offices they hold, or whether the statutory concept of control requires a more substantive and legally enforceable nexus with the affairs of the Indian company.

(e) Legal significance to references made in financial statements to a "holding company" - The ROC placed substantial reliance on the fact that LinkedIn India's financial statements referred to LinkedIn Corporation, USA as its holding company, despite that entity not appearing in the formally disclosed ownership chain. The case therefore raises an important interpretive issue: whether descriptions made in financial statements for accounting or operational purposes can themselves create legal consequences under the SBO framework.

(f) Whether the SBO proceedings account for disclosures already made before foreign regulators - LinkedIn India highlighted that Microsoft Corporation already makes extensive ownership disclosures before the SEC as a publicly listed company in the United States, and that no individual holds more than 10% of its shares. As beneficial ownership regimes increasingly operate within a globally interconnected transparency framework, the case may also prompt consideration of whether disclosures made under foreign regulatory systems should carry persuasive or safe harbour value in Indian SBO proceedings.

The Delhi High Court's eventual decision is therefore likely to influence not only the interpretation of Sections 89 and 90 of the Act, but also the broader relationship between Indian corporate regulation and the governance realities of modern multinational enterprises.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]