Cyprus as your Blockchain Jurisdiction of choice

Cyprus being an EU jurisdiction with a well-organized and regulated regime in full compliance with European legislation, provides additional comfort to prospective investors to rely on ICOs or STOs having Cyprus as their base. Further, Cyprus has a favorable tax system along with an extensive network of the double tax treaties making Cyprus an ideal jurisdiction from a financial aspect as well for both the issuing company and the investor. The flexible and well-organized infrastructure of Cyprus as well as the low costs for setting up an office in Cyprus for the ICO or STO project, are some additional advantages to be considered favorably for such a choice of jurisdiction.

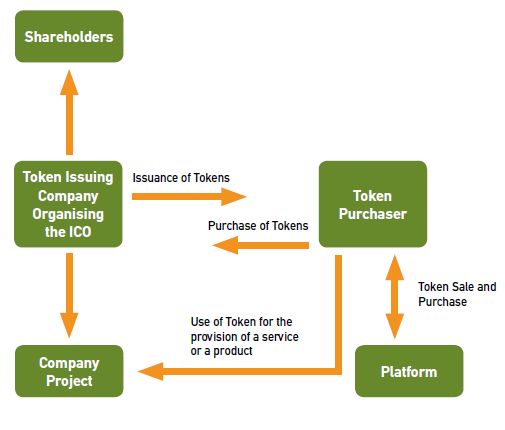

Initial Coin Offering (ICO)

ICOs have become an increasingly popular method of fundraising for start-ups and other companies with the intention to fund innovative projects based on Blockchain technology. Although there is not a specific regulatory framework for ICOs, Cyprus has shown willingness to support innovation through the creation of the Innovation Hub and having a constant oversight over market developments. ICOs may be conducted through Cyprus companies provided the securities legislation is not violated.

Security Token Offering (STO)

STOs as their name suggests, are securities in the form of digital assets which can be indicatively, Debt Tokens, Equity Tokens, Convertible to Shares Tokens, Derivative Tokens and generally Tokens having characteristics similar to shares, that need to be compliant with securities legislation before their offering to the public, subject to exceptions. STOs are regarded to be the upcoming gamechangers to the traditional financing methods. STOs either done by way of a private placement of a tokenized security or by way of a public offering, are providing companies with innovative ideas with the opportunity to reach a pool of investors and raise funding for their projects in a compliant, easier and cost-efficient method. Particular guidelines and specific regulations need to be issued by the regulator facilitating and clarifying the matter.

Any STO would require the publication of an approved prospectus, unless qualifying for an exemption applicable under the existing legislation. The exceptions currently in force are:

1. A public offering of securities from Cyprus for a total consideration in the whole European

Union less than €5 million calculated over a 12-month period.

2. An offer of securities addressed solely to qualified investors.

3. An offer of securities addressed to fewer than 150 natural or legal persons per Member

State, other than qualified investors.

4. An offer of securities whose denomination per unit amounts to at least €100.000.

5. An offer of securities addressed to investors who acquire securities for a total consideration

of at least €100.000 per investor, for each separate offer.

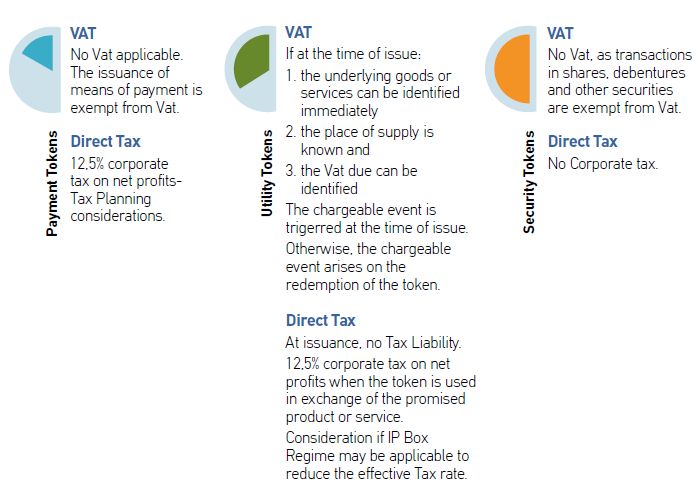

Tax & Vat Considerations

Taxation is always of an immense importance as it is one of the most important factors to consider when making an investment. Cyprus offers an attractive tax regime with one of the lowest corporate Tax and Vat rates in the EU being 12.5% and 19% respectively.

In order to assess both the Tax and Vat implications of ICOs or STOs one needs to understand the nature of the tokens being offered. In their simple form these can be classified as Payment Tokens which are designed as a means of payments, Utility Tokens giving access to goods and services and Security Tokens resembling the characteristics of equities, debentures, financial instruments.

In the absence of specific guidelines by the Cyprus Tax Authorities on both Tax and Vat implications of tokens, we hereby express our views based on the basic and fundamental provisions of the Cyprus Tax and Vat Legislations that are currently in force, while having in mind the general provisions of the International Financial Reporting Standards (IFRSs).

How Kinanis Law Firm can assist

Our Firm is ready to assist clients with:

" Legal, Tax, Vat and Accounting advice for Blockchain projects;

" Classification of Tokens to be issued;

" Drafting or review of Whitepaper, Prospectus or Offering Memorandum;

" Drafting or review of privacy policy agreement and the terms and conditions of sale agreement;

" Drafting or review of the terms of use of the website agreement, the risk factors document and

" the cookies policy;

" Advice on AML, KYC, and Compliance issues - preparation of relevant manuals;

" Advice on Data Protection law issues (GDPR) and drafting of GDPR provisions;

" Advice on the ICO, STO and corporate structure to be used;

" Formation and management of companies to be used in the project;

" Support on banking issues for the opening of bank accounts;

" Drafting of Shareholders' agreements;

" Ongoing legal advice on the project and related issues.

Our Firm

We are a Law Firm with offices in Cyprus and Malta and a representative office in Shanghai China comprising of more than 80 lawyers, accountants and other professionals who advise, international and local clients.

The Firm has been offering legal and consulting services since 1983 evolving from a traditional law firm to an innovative cutting-edge multidisciplinary law firm combining exceptional expertise in law, tax, vat and accounting.

From its establishment the Firm's focus has been heavily business oriented and always abreast with the latest global developments and innovations. Drawing from our pool of experienced professionals we provide our clients' businesses full legal and accounting support on an everyday basis as well as customized solutions in today's global financial and legal challenges.

We consider ourselves as 'traditional pioneers' and our motto is to foresee and anticipate any issues that may potentially impact our clients' business and to offer effective advice and solutions proactively.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.