Carey Olsen Starting Point Guides are intended as a general introduction and guide to different aspects of Guernsey law.

They contain many of the most important issues that we come across but are very much the edited highlights of those issues. If you would like legal advice in relation to any specific circumstances, please contact us.

Guernsey

Guernsey is part of the Channel Islands and is a British Crown dependency.

It has its own financial, legal and judicial systems and its own parliament. It is not part of the UK or the European Union.

Is there specific legislation in Guernsey relating to pensions?

Guernsey has no specific pension legislation. However, Guernsey pensions and pension schemes have their own local tax approval regime which is contained in the Income Tax (Guernsey) Law 1975, as amended (the "Guernsey Income Tax Law"). Furthermore, a new regulatory and supervisory framework for pension schemes and their providers is currently being put in place as described below.

Is there a pensions regulator in Guernsey?

The Guernsey Financial Services Commission ("GFSC") is the supervisory authority for pensions in Guernsey. The formation, administration and management of pension schemes and gratuity schemes have been regulated activities since 30 June 2017.

Certain but not all pension related activities may also form the basis of complaints to the Channel Islands Financial Ombudsman.

Approved pension schemes in Guernsey

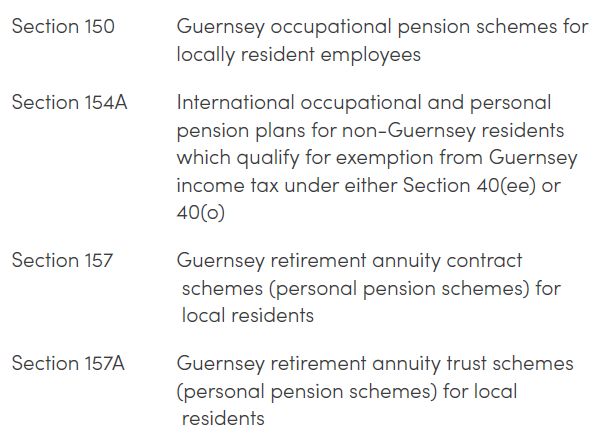

If a pension scheme meets certain requirements, an application can be made to the Director of Income Tax in Guernsey (the "Director") for approval under the relevant Section of the Guernsey Income Tax Law. If approval is obtained, there are certain tax and other benefits for employers and scheme members. The types of approved schemes in Guernsey are as follows:

Personal pension schemes established for both local and non-Guernsey members may also, if they meet certain criteria, obtain "exempt" status under Section 157(E) whereby the scheme itself as well as any benefits received from the scheme by members are exempt from Guernsey income tax but no tax allowances are claimable on contributions made to such schemes.

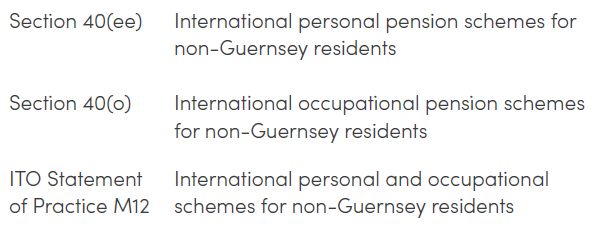

Schemes established for non-Guernsey residents may qualify for general exemption from Guernsey Income Tax if they meet certain requirements. The types of exempt schemes in Guernsey are:

Guernsey practice notes The requirements a pension scheme must

meet in order to obtain approval under:

- Section 150 of the Guernsey Income Tax Law are set out in the Guernsey Practice Notes - Requirements for Approved Occupational Pension Schemes; and

- Sections 157 and 157A of the Guernsey Income Tax Law are set out in the Guernsey Practice Notes - Requirements for Approved Retirement Annuity Trust Schemes and Approved Retirement Annuity Schemes.

The Practice Notes are updated periodically and can be accessed on the States of Guernsey website – gov.gg.

Unapproved pension schemes

It may not always be appropriate or necessary for a pension scheme to be an approved or exempt scheme, in which case it may be administered on an unapproved basis. However, legal and tax advice should be taken when establishing or joining an unapproved pension scheme or seeking to transfer benefits to or from such a scheme.

Defined benefit or defined contribution?

The majority of occupational (employer sponsored) pension schemes are now defined contribution (also known as "money purchase") schemes. This means the amount of a member's pension will depend on the value of their individual fund or "pension pot" in the scheme when they take their benefits. This amount will depend on matters such as the amount of contributions made by or on behalf of a member and how well the investments in which such contributions have been invested, have performed over the period during which they have been held in the scheme.

Pension scheme members of defined benefit pension schemes will normally receive a multiple of their final salary as a pension when they choose to take their benefits. However, many such schemes have been closed to new members over recent years due to the cost of employer contributions which has resulted in employers no longer being willing to contribute the funds required to enable the schemes to pay such pensions in full when they fall due.

Regulation and supervision of Guernsey pension schemes and their providers

In 2017, the States of Guernsey decided to introduce a regulatory and supervisory framework for Guernsey pension schemes and their providers. At the same time, legislative changes were introduced to enable non–domestic pension schemes to seek approval under the Guernsey Income Tax Law, with a view to providing information reporting to the local tax authority as an approved scheme. One of the motivations behind these changes was to enable eligible pensions to meet the approved status requirements of the OECD's Common Reporting Standard ("CRS") to enable such schemes to fall outside the scope of CRS reporting.

Under the new framework, the formation, administration and management of pension schemes or gratuity schemes (as defined), and the provision of advice in relation to the formation, management or administration of pension schemes or gratuity schemes in Guernsey is now a regulated activity and the GFSC is the new supervisory authority.

On 25 August 2017, the GFSC published "The Pension Licensees (Conduct of Business) & Domestic & International Pension Scheme and Gratuity Scheme Rules (No 2) 2017"(the "Rules"). Amongst other things, these include various notification and reporting requirements to the GFSC and guidelines for trustees of pension schemes to follow, for example on transfers, investments and the provision of information to the GFSC and members. The Rules came into force as from 29 August 2017, although changes to a previous version of the Rules published on 7 July 2017 are effective from 30 June 2017. The Rules apply to persons who hold a licence under the Regulation of Fiduciaries Administration Businesses and Company Directors, etc (Bailiwick of Guernsey) Law 2000, (as amended) and apply in respect of pension schemes and gratuity schemes (as defined). There is a transitional period as part of the introduction of the Rules, whereby licensees must comply with the Rules by 30 September 2018. There is a comment in the Rules that the GFSC may in its discretion notify a licensee in writing that it agrees to exclude or modify the application of any part of the Rules if it is satisfied this will not prejudice the interests of the members of the pension scheme. At present, there is no any indication of the likely types of derogations which the GFSC may consider.

The new supervision and information reporting regime is still in its early stages of development. Industry will be consulted over the next year on the preparation of a Policy Letter setting out further details of the new regulatory framework and any further legislative changes that may be required to implement the regime. In addition, the Income Tax Office in Guernsey has indicated that supplementary bulletins will be issued as the regulation evolves over time.

Multi-jurisdictional occupational pension schemes

It is common for an employer to want to establish a pension scheme outside Guernsey for employees employed in and resident in a number of different jurisdictions. Where such a scheme includes Guernsey resident employees, it is possible, if the necessary requirements are met, for part approval under Section 150 of the Guernsey Income Tax Law to be obtained in respect of the section relating to Guernsey employees. Where such a scheme is established in Guernsey, the remaining part of the pension scheme, covering members in other jurisdictions outside Guernsey, may, if it meets the necessary requirements, qualify for exemption from Guernsey Income Tax under Section 40(o) of the Guernsey Income Tax Law and may also qualify for approval under Section 154A.

Qualifying Recognised Overseas Pension Schemes ("QROPS")

Guernsey schemes established for Guernsey residents with Trustees licensed by the GFSC and which meet the relevant United Kingdom tax criteria are capable of being QROPS and therefore able to receive transfers of United Kingdom pension benefits.

Transfers between pension schemes

It is possible to transfer accrued benefits between pension schemes in certain circumstances. Relevant factors will include what is permitted under the relevant scheme documentation and whether either or both schemes have obtained formal approval, registration or similar, in the relevant jurisdiction or jurisdictions. In certain cases, the approval of the Director to a proposed transfer will be required. It is possible to make transfers between pension schemes in Guernsey and the UK if various conditions are met.

We recommend specific advice is always taken on any proposed transfer to ascertain whether it is possible, what the legal requirements are and what the tax implications will be.

Pension scheme documentation

In Guernsey, pension schemes other than retirement annuity contracts are typically documented by way of a trust instrument with scheme rules attached. Normally, the trustees arrange for scheme funds to be invested and commonly appoint a professional investment manager to assist with this. Alternatively, trustees may purchase one or more insurance policies to secure the benefits due under a particular pension scheme.

Divorce – can pension sharing orders from other jurisdictions be enforced?

Pension sharing orders cannot be enforced in Guernsey, as there is currently no legislation in Guernsey which recognises them.

An alternative solution therefore needs to be sought in these cases, such as offsetting the value of the pension against other assets. This often means that the party with the pension arrangement may have to sacrifice liquid capital to retain the benefit of the pension arrangement.

Retirement age - are there any issues under the discrimination law in Guernsey?

Age is not currently a protected characteristic under Guernsey law.

Tax

The tax issues concerning a pension scheme or a particular action to be taken under a pension scheme should always be ascertained.

In respect of pension schemes for overseas employees and individuals, tax advice in all relevant jurisdictions(s) should be taken.

Is there a Guernsey equivalent to the UK's Section 75 debt?

There is no equivalent in Guernsey to a UK statutory Section 75 debt under which an employer may be obliged to stand behind a scheme's ongoing liabilities and any debt on a scheme's discontinuance. The employer's obligations in relation to funding are as contained in the scheme documentation. In the event of a deficiency in a defined benefit pension scheme in Guernsey, the employer and the trustees would be expected to consider together how this may be cleared, including by putting in place a recovery plan.

Does pension freedom apply as in the UK?

No. Although the Guernsey tax approval regime has been amended over recent years to provide greater flexibility in the way in which pension scheme benefits may be provided, there are currently no plans to amend Guernsey legislation further to introduce "pension freedom" along the lines introduced in the United Kingdom in 2015.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.