- within Insurance, Media, Telecoms, IT and Entertainment topic(s)

SEC DEVELOPMENTS

Update on the Climate Disclosure Rules

On April 4, 2024, the U.S. Securities and Exchange Commission (the "SEC") voluntarily stayed the climate disclosure rules it had adopted only a month earlier. The voluntary stay followed a number of legal challenges being filed against the new climate disclosure rules, which were consolidated in the Eighth Circuit. Briefings on those challenges are due to be completed by September 3, 2024. While it's difficult to predict when we'll see a final resolution of that litigation, the voluntary stay order issued by the SEC contemplates that the challenges to the climate rules may extend beyond 2025. If the SEC prevails in the litigation, we expect it will push back at least some of the disclosure requirements. Large accelerated filers will not be in a position to make their first disclosures for 2025 (due in 2026) if they do not begin their supporting work well in advance.

However, the SEC's stay of its new climate disclosure rules does not affect other disclosure obligations under the U.S. federal securities laws. The SEC has long been of the view that some of those obligations may require disclosure of climate-related matters. The SEC issued guidance in 2010, which we discuss here, that highlighted how climate-related matters might need to be discussed under existing principles-based business, risk factors, legal proceedings and MD&A requirements. More recently, in 2021, the SEC published a sample comment letter on climate change-related disclosures. The SEC staff also has issued climate-related comments to many registrants, and has recently come under pressure from Democratic members of Congress to "ensure robust enforcement of existing SEC climate disclosure-related guidance" while litigation on the new rules remains pending.

Aside from the SEC's rules, public and private companies need to manage other current and pending climate disclosure requirements (and other ESG disclosures more generally) at the U.S. federal and state levels as well as outside the United States. Most notably, the EU's Corporate Sustainability Reporting Directive (the "CSRD") will require that climate and other sustainability disclosures be made by thousands of companies, including a large number of U.S.-based multinationals and/or their EU subsidiaries. In addition to companies listed on regulated markets in the EU, the CSRD applies to private entities organized in an EU jurisdiction, including wholly-owned and other subsidiaries of public and private U.S.-based multinationals, that exceed specified balance sheet, income and employee thresholds. EU subsidiaries of U.S. multinationals largely will be in the second wave of CSRD reporting companies – required to make disclosures in 2026 for fiscal years beginning after January 1, 2025.

California has also adopted three new laws that will require a large number of companies to make greenhouse gas emissions and other climate disclosures, though each of those three laws is the subject of proposed amendments that would, among other things, delay reporting deadlines. Other jurisdictions (such as the UK) have adopted or are considering adopting rules requiring climate and other ESG disclosures, and many others have adopted or are considering adopting standards such as those based on the standards released by the International Sustainability Standard Board, which we discuss here. While there is substantial uncertainty as to when or if the SEC's climate disclosure rules will come into effect, companies will continue to need to assess their requirements to and prepare to make climate and other sustainability disclosures.

SEC Corp. Fin. Director Provides Additional Guidance on Cybersecurity Incident Disclosures

Erik Gerding, the SEC's Director of the Division of Corporation Finance, recently issued two guidance statements related to Item 1.05 of Form 8-K, which was adopted by the SEC last year and requires public companies to disclose material cybersecurity incidents. While his first statement issued in May was focused on voluntary disclosure of cybersecurity incidents on Form 8-K, his second statement issued in June addressed the private sharing of additional information (i.e., beyond an Item 1.05 disclosure) concerning a cybersecurity incident and related Regulation FD considerations.

In his May statement, Gerding provided the following guidance:

- Only cybersecurity incidents that a company has determined to be material should be disclosed under Item 1.05 of Form 8-K;

- To avoid investor confusion or dilution in the value of Item 1.05 disclosures, a company that wishes to disclose an immaterial cybersecurity incident or a cybersecurity incident that it has yet to determine to be material may do so under Item 8.01 of Form 8-K;

- If such incident is subsequently determined to be material, however, the company must file an Item 1.05 Form 8-K within four business days of such determination. While the new filing may refer to the prior Item 8.01 disclosure, it must satisfy all Item 1.05 requirements; and

- Companies are reminded that they should consider all relevant factors in determining the materiality of a cybersecurity incident or in assessing the incident's impact (or reasonably likely impact), including qualitative factors such as harm to its reputation, customer or vendor relationships, competitiveness, as well as the possibility of litigation or regulatory investigations or actions.

In his June statement, he noted that:

- Item 1.05 of Form 8-K does not prohibit a company from privately discussing or sharing information about a material cybersecurity incident with other parties (which may include vendors or customers, or companies similarly at risk) beyond what it discloses in an Item 1.05 Form 8-K – doing so may facilitate remediation, mitigation, or risk avoidance efforts, or such parties' regulatory compliance;

- While Item 1.05 does not alter the application of Regulation FD to cybersecurity communications, whether Regulation FD, which requires public disclosure of any material nonpublic information that has been selectively disclosed to securities market professionals or shareholders, is implicated by such private disclosures, depends on the information disclosed and the persons to whom it is disclosed; and

- With their counsel's guidance, companies may be able to privately disclose such information in several ways without implicating Regulation FD, including by entering into confidentiality agreements with such parties covering such information.

SEC Corp. Fin. Division Highlights 2024 Disclosure Review Priorities

At the 2024 SEC Speaks Conference in April, staff of the SEC's Division of Corporation Finance identified the Division's disclosure review priorities for 2024. Erik Gerding, the Division's Director, recently issued a statement regarding the priorities outlined at the conference. According to the statement, those priorities include disclosures regarding artificial intelligence (AI), certain financial reporting matters, China-based companies, material ongoing impacts of inflation, interest rate and liquidity risks, commercial real estate market exposure, and recently adopted disclosure rules on cybersecurity incidents, clawback of executive compensation, pay versus performance, universal proxy, and beneficial ownership reporting.

Artificial Intelligence

On AI, the statement notes that existing rules may require a company to disclose its AI use and related risks, including in the description of business section, risk factors, management's discussion and analysis (MD&A), the financial statements, and the disclosure on the board's role on risk oversight. In 2024, the Division will focus on the disclosure of AI opportunities and risks, such as whether or not a company:

- clearly defines AI and how AI could improve its results of operations, financial condition, and future prospects;

- provides tailored disclosure about its material AI risks and their reasonably likely impact on its business and financial results;

- focuses on its current or proposed AI technology rather than AI unrelated to its business; and

- has a reasonable basis for its claims on AI prospects.

Financial Reporting

Regarding financial reporting, the Division will focus especially on areas that involve judgment, as well as recently issued accounting standards, including:

- segment reporting, including compliance with new U.S. GAAP disclosures effective in annual periods beginning after December 15, 2023;

- compliance with non-GAAP regulations and rules;

- critical accounting estimates disclosure in MD&A; and

- disclosures related to supplier finance programs in the notes to the financial statements and any related information in MD&A.

SEC Issues Spring 2024 Regulatory Flexibility Agenda

On July 5, 2024, the SEC issued the SEC Chair's agenda of rulemaking actions. The agenda, which is generally as of May 1, 2024, reflects the targeted timelines for the SEC Chair's rulemaking priorities. We highlight below some of the timelines in the agenda for proposed and final rulemaking actions that may be of interest.

Expected Final Rules

- Edgar Filer Access & Account Management – October 2024

- Rule 14a-8 Amendments – April 2025

Expected Proposed Rules

- Human Capital Management Disclosure – October 2024

- Corporate Board Diversity – April 2025

- Rule 144 Holding Period – April 2025

- Regulation D and Form D Improvements – April 2025

- Revisions to Definition of Securities Held of Record – April 2025

Selected SEC Filing Reminders

- Companies—other than smaller reporting companies (SRCs)—filing their Form 10-K or Form 20-F for a fiscal year that began on or after April 1, 2023, will be required to disclose in that report if they have adopted insider trading policies (including those governing trading by the company itself) and, if not, why they have not done so. If they have adopted an insider trading policy, the policy must be filed as an exhibit to the report. The disclosure applies to SRCs for fiscal years beginning on or after October 1, 2023.

- Beginning with Form 10-Ks for fiscal years beginning on or after April 1, 2023 (or, at an issuer's option, proxy statements for stockholder meetings after that year), issuers (other than foreign private issuers and SRCs) must disclose certain information regarding options, stock appreciation rights, and similar instruments granted to named executive officers within four business days before or one business day after, (i) filing of a quarterly report on Form 10-Q or annual report on Form 10-K, or (ii) filing or furnishing a Form 8-K (other than a Form 8-K reporting only the grant of a material new option award that includes material nonpublic information). The disclosure must also include the issuer's policies and practices on the timing of awards of options in relation to the disclosure of material nonpublic information by the issuer. The disclosure applies to SRCs for fiscal years beginning on or after October 1, 2023.

- Compliance with revised Schedule 13G deadlines (discussed here) will be required beginning September 30, 2024.

- Most calendar year resource extraction companies will be required to file a Form SD by September 26, 2024, disclosing payments made in the 2023 fiscal year to the U.S. federal government or foreign governments for resource extraction development purposes. See further details here.

DEVELOPMENTS FROM THE COURTS

SEC Wins First Novel "Shadow Trading" Case – Key Takeaways from the Panuwat Insider Trading Case

On April 5, 2024, a civil jury in the SEC's first "shadow trading" case found the defendant, Matthew Panuwat, liable for insider trading for using material non-public information (MNPI) about his employer (namely, that the employer was going to be acquired) to trade in the securities of a purportedly comparable company. The jury verdict gives rise to potential complications for compliance departments who will have to assess how the decision impacts their company's insider trading policies and procedures.

We summarize the decision below and outline practices for incorporating the case's guidance to ensure that companies are best positioned to withstand scrutiny from the SEC in the wake of this case.

Background

The Facts

As with any insider trading case, the issue in the Panuwat trial was whether the SEC could establish that the defendant traded in breach of a duty of trust and confidence while in possession of MNPI.

The case was tried in a Northern California federal court, where a jury found those elements were satisfied on the following facts after just roughly two hours of deliberation. Panuwat traded while serving in a business development role at Medivation, an early-stage pharmaceutical company. In 2016, several minutes after Panuwat received an email from Medivation's then-CEO conveying material progress toward Medivation's potential acquisition by Pfizer, Panuwat purchased call options for securities issued by a third company, Incyte. Incyte was a comparable near-peer to Medivation but not a direct competitor or business partner. The SEC took the position that Panuwat traded on the basis that news about the acquisition was material to Incyte – that, once the Pfizer acquisition news became public, Incyte's value would increase. Incyte's stock price did, in fact, increase when Pfizer publicly announced the Medivation acquisition, and Panuwat made a profit of $107,000 on his trades.

Shadow Trading

The Panuwat fact pattern has been referred to as "shadow trading" or the "adjacency theory" by commentators because, unlike a classic insider trading case that involves trading on the securities of an issuer based on MNPI directly about that issuer, Panuwat possessed MNPI about one issuer (his employer), but transacted in the securities of a different issuer (Incyte), based on an inference about the market impact that information would have once it became public. Shadow trading is based on the misappropriation theory of insider trading liability that imposes liability when MNPI is used for securities trading purposes in breach of a duty of trust and confidence owed to the source of the MNPI—the breach being a failure to obtain the MNPI source's consent to use the information. While the SEC has repeatedly asserted that there is "nothing novel" about this variety of the misappropriation theory of liability, the Panuwat case nevertheless represents the first time the SEC has brought a civil action under this theory.

Preliminary Motions and the SEC's Theories on the Existence of a Duty

Panuwat had moved to dismiss the complaint and sought summary judgment arguing that the SEC had not asserted a cognizable insider trading claim; both of those motions were denied.

The SEC advanced three theories to ground its claim that Panuwat owed a duty of trust and confidence to Medivation. The SEC claimed that:

- Under common law governing a principal-agency relationship, such a duty arises when an employer entrusts an employee with confidential information because the information is company property that an employee cannot use for personal benefit without obtaining the employer's informed consent.

- The duty arose under the terms of Medivation's insider trading policy that Panuwat signed. That policy expressly prohibited the use of MNPI about Medivation or other publicly-traded companies with which it has business dealings for personal benefit.

- The duty arose under the terms of a confidentiality agreement that Panuwat signed, which prohibited the use of confidential information, except for Medivation's benefit.

Agreeing with the SEC, the judge at summary judgment ruled that Panuwat independently owed duties of trust, confidence or confidentiality based on these three theories and the jury instructions reflected this.

Panuwat's Post-Verdict Steps

Following the verdict, Panuwat filed two motions: (i) a motion for judgment as a matter of law which claims that the jury did not have a sufficient basis to reach the verdict it did; and (ii) a motion for a new trial based on several grounds, including that the jury instructions were wrong. These are now fully briefed and pending before the Court.

Panuwat moved the trial court for the right to take an interlocutory appeal before trial commenced (the motion was denied) and will almost certainly appeal the jury's determination to the Ninth Circuit Court of Appeals. While reversing a jury verdict may be challenging on appeal, Panuwat will have the opportunity to renew his broader arguments as to why the SEC's theory of liability does not state a prima facie claim for insider trading—a position that the trial court rejected at the motion to dismiss and summary judgment stages. Any Ninth Circuit—or, ultimately, Supreme Court—decision may help define the outer parameters of a permissible "shadow trading" enforcement case.

Key Takeaways

In the near term, the Panuwat jury verdict surely emboldens the SEC to continue advancing an expansive interpretation of its authority to police insider trading, and may spur analogous criminal "shadow trading" investigations by the Department of Justice (DOJ). The SEC's Director of Enforcement has stated publicly that other such cases are currently being investigated.

A key question after the Panuwat trial remains the scope of the duties of confidentiality that could, if breached, serve as the basis for an action brought by the SEC. Going forward, the SEC or DOJ may advance more cases where the duty arises in contexts outside of traditional fiduciary principles. This could open the door for a "shadow trading" action brought solely on the basis of an alleged breach of a confidentiality duty that arises merely from a company's entrustment of an employee with confidential information. Compliance and in-house legal professionals should carefully consider these hypotheticals in establishing MNPI management procedures and walls.

At a practical level, compliance teams may want to consider the following:

- Inventory and assess confidentiality and MNPI management language in relevant agreements and policies (including employment and similar agreements, board of director engagement agreements, vendor contracts, and non-disclosure agreements with other third parties, as well as Compliance Manual policies and procedures) to review the scope and ensure appropriately tailored prohibitory language that is consistently applied as may be appropriate.

- Revisit pre-clearance restrictions and related controls around MNPI such as watchlists and restricted lists.

- Consider if language in trading attestations needs to be adjusted.

- When reviewing preclearance requests, understand the sector of the proposed trade and consider adding to the manual process or software an inquiry into whether the employee has MNPI about that company or any "similarly situated company."

- Conduct training on insider trading laws as well as any newly scoped trading restrictions in light of the Panuwat case.

- Ensure that there is some level of escalating repercussions for pre-clearance violations or untimely quarterly transaction reports (as well as other Code of Ethics violations), and enhance electronic communication surveillance when appropriate.

- Stay tuned to the industry adjustments following the case, such as changes in expert network controls, and consult with counsel when amending agreements.

Above all, the Panuwat episode highlights the SEC's increasing appetite to bring cases involving the alleged misuse of MNPI that may seem marginal or legally challenging. The Panuwat case underscores a reality of insider trading enforcement that is harder to capture in formal guidance but remans salient: notwithstanding Panuwat's legal defenses, the facts showed that Panuwat traded within minutes of receiving a confidential internal business update. The jury's abbreviated deliberations suggest that this factual evidence was sufficiently convincing, notwithstanding any lingering doubts about the legal validity of the SEC's theory of liability.

DOJ Secures Conviction in First Insider Trading Case Based on 10b5-1 Plan Abuse

On June 21, 2024, a federal jury in California convicted Terren Peizer, the former Chief Executive Officer, Executive Chairman, and Chairman of the Board of Ontrak Inc., for insider trading on the basis that he possessed material non-public information (MNPI) about Ontrak (the imminent termination of a significant customer relationship) when he entered into two Rule 10b5-1 plans under which he sold shares of the company, avoiding more than $12.5 million in losses. The DOJ had alleged that Peizer started selling shares a day after establishing each plan and had refused to include cooling-off periods in the plans, as advised by his brokers. The case is the DOJ's first insider trading prosecution based exclusively on the use of a trading plan, and, after the verdict, the DOJ warned that "it will not be our last."

Rule 10b5-1 under the Securities Exchange Act of 1934 (the "Exchange Act"), which rule was recently amended by the SEC (discussed here), provides a widely used affirmative defense against insider trading liability under Section 10(b) of the Exchange Act and Rule 10b-5 thereunder for corporate insiders to trade securities, permitting them to adopt a plan that satisfies certain conditions and that would trigger trades at some point in the future based on pre-established criteria. Among other conditions, to be compliant, an insider must not have possessed MNPI about the issuer when the plan is adopted, and the plan must have been adopted in good faith. ;Although the case, which was part of a data-driven initiative led by the DOJ's Fraud Section to identify executive abuses of Rule 10b5-1 plans, was based on the pre-amendment Rule 10b5-1, which, unlike the current Rule 10b5-1, did not require a cooling-off period, it signals that the DOJ is focused on abusive practices with respect to Rule 10b5-1 plans.

Pure Omissions Are Not Actionable Under Rule 10b-5(b), Supreme Court Declares

On April 12, 2024, the U.S. Supreme Court delivered its ruling in Macquarie Infrastructure Corp. v. Moab Partners, L.P., 601 U.S. 257, finally laying to rest a lingering question: Can one be liable under Rule 10b-5(b) under the Exchange Act (an antifraud provision) for failing to disclose information one is required to disclose under Item 303 of Regulation S-K even if the failure does not make any disclosed statements misleading? A unanimous court answered: "No."

In Macquarie, the Supreme Court considered the liability nexus between Item 303 (Management's Discussion and Analysis of Financial Condition and Results of Operations) of Regulation S-K's provision that companies describe "any known trends or uncertainties that have had or that are reasonably likely to have a material favorable or unfavorable impact on net sales or revenues or income from continuing operations" and Rule 10b-5(b)'s provision that makes it unlawful for any person to "omit to state a material fact necessary in order to make the statements made, in the light of the circumstances under which they were made, not misleading, in connection with the purchase or sale of any security," as the case involved an allegation that such a known trend or uncertainty was undisclosed.

Although the court's decision was in the context of Item 303, the decision stands for these broad principles:

- Pure omissions (silence in circumstances that do not give any

particular meaning to that silence) are not actionable under Rule

10b-5(b); only false statements and misleading half-truths are;

- So, an affirmative assertion must be identified before determining if other facts are needed to make that assertion not misleading.

- Rule 10b-5(b) does not create an affirmative duty to disclose any and all material information;

- A duty to disclose does not automatically render silence misleading under Rule 10b-5(b)

While the decision settles the narrow question raised in the case, it does not address whether the other prongs of Rule 10b-5 (i.e., Rule 10b-5(a) or Rule 10b-5(c)) support liability for pure omissions or what "statements made" means under Rule 10b-5(b) and, importantly, does not affect liability for pure omissions under Section 11 of the Securities Act of 1933 (the "Securities Act"), which continues to apply to registered offerings. Furthermore, the decision is likely to encourage the plaintiff bar to simply recast their Rule 10b-5(b) claims as half-truth claims. Companies should therefore be mindful that the decision may be of limited practical effect.

Supreme Court Reasserts Federal Courts' Interpretive Authority by Overruling Chevron Doctrine

In Loper Bright Enterprises v. Raimondo, No. 22-451, 2024 WL 3208360 (U.S. June 28, 2024), the Supreme Court overruled the Chevron doctrine, a longstanding judicial precedent that required federal courts to defer to the interpretations of ambiguous statutes by administrative agencies like the SEC so long as that interpretation was reasonable, holding that federal courts are the final authority on interpretation of such statutes. The decision is expected to make it easier to challenge statutory interpretations by administrative agencies. Our discussion of the case is available here.

Supreme Court Declares SEC Administrative Proceedings for Securities Fraud Unconstitutional

On June 27, 2024, the Supreme Court ruled in SEC v. Jarkesy, U.S. No. 22-859 (2024), that the SEC may not initiate an administrative proceeding seeking civil penalties for securities fraud because the Seventh Amendment to the Constitution requires a jury trial for such actions. Accordingly, such actions may only be pursued in federal courts. The decision is, however, not likely to have a great impact on the SEC has already been moving towards using the federal courts for some time now. We discuss the case and its likely implications, particularly for other administrative agencies, here.

NYSE DEVELOPMENTS

NYSE Mandates Trading Halt for Reverse Stock Splits

Effective May 11, 2024, the New York Stock Exchange (NYSE) amended its rules to impose a mandatory trading halt on securities subject to a reverse stock split. The trading halt will be initiated before the end of after-hours trading on other markets on the day immediately before the effective date of the reverse stock split. Specifically, the NYSE generally expects to initiate the halt at 7:50 p.m. E.T. on that day (i.e., ten minutes before after-hours trading ends on other markets). Trading in the security will then resume via a trading halt auction at 9:30 a.m. E.T. on the effective date of the reverse stock split. The NYSE rule, which is modeled after recent amendments to Nasdaq's rules and comes on the heels of an increase in reverse stock splits in recent years, is intended to promote consistency across the exchanges for the benefit of market participants and minimize the potential for processing errors, including incorrect adjustment or entry of orders, resulting from market participants and investors being unaware of the reverse stock split.

Prior to the amendment, an NYSE-listed security that was subject to a reverse stock split was available for trading on other markets at 4:00 a.m. on the effective day of the split on a split-adjusted basis.

Under Proposed Rule, NYSE May Delist Companies That Change Their Primary Business Focus

In April 2024, the NYSE proposed a change to its Listed Company Manual that would allow it to immediately commence suspension and delisting procedures against companies that significantly change their primary business focus. Under the proposal, the NYSE may exercise this discretion when a company changes its primary business focus to a business that is substantially different from its business at the time of listing or that was immaterial to its business at that time. The proposal aims to protect investors for whom the change represents a fundamental change in their investment decision (including from stock price drops that may result from the change) and to provide the exchange with the opportunity to consider if the company would have been suitable for listing had the modified business been its primary business at the time of listing. In deciding whether a company should face delisting, the NYSE will primarily consider whether the NYSE would have accepted the company for listing with its modified business focus. The NYSE notes in the proposal that, in analyzing this, it would not consider its quantitative standards for initial listing, but would instead focus on qualitative factors, including management and board changes, and changes in the company's voting power, ownership, and financial structure that occur in connection with the change in primary business focus.

Importantly, the NYSE acknowledges in the proposal that, as delisting on these grounds would be an extraordinary action, it expects to exercise the discretionary authority infrequently and only after considering all relevant facts and circumstances. The SEC is expected to act on the proposed rule by July 24, 2024.

NYSE Proposes to Expand the Circumstances for the Listing of Rights

In April 2024, the NYSE proposed a rule change that would allow the listing of rights exercisable for securities that are not already listed on the exchange and will not be concurrently listed with those rights. As proposed, the rule would expand the circumstances for the listing of rights to cover rights ("prospective listing rights") whose underlying security will be listed on the exchange only when the rights are exercised and whose exercise will be pursuant to an effective Securities Act registration statement in place by the time the rights are listed. The proposed rule change is intended to give issuers more flexibility in raising capital through rights offerings, as they would not be limited to offering rights to existing shareholders only. The registration statement requirement is intended to protect investors by ensuring they have access to current information about the issuer on a continuing basis for purposes of trading in the rights.

The proposed rule includes certain requirements and conditions for listing and delisting prospective listing rights. For initial listing, there must be at least 1,000,000 rights issued and at least 400 public holders of round lots. For delisting, the NYSE will initiate suspension and delisting procedures if (i) the underlying security will not be listed on the exchange, (ii) the market value of the publicly held prospective listing rights falls below $4,000,000, or (iii) the prospective listing rights are still outstanding at the time the underlying securities are listed and they fail to meet the initial listing requirements applicable to non-prospective listing rights. The SEC is expected to act on the proposed rule by August 13, 2024.

NYSE Proposes to Extend Listing Lifespan of SPACs

In March 2024, the NYSE proposed amendments to its Listed Company Manual that would extend the maximum allowable time a special purpose acquisition company (SPAC) may remain listed without completing a business combination from 36 months to 42 months of its listing date, so long as the SPAC has entered into a business combination agreement within three years of listing (or a shorter period provided for in its governing documents). Under the proposal, a SPAC that has not entered into a business combination agreement within three years of listing (or such shorter period) would face delisting. If approved as proposed, the proposed amendments would give NYSE-listed SPACs additional flexibility in the timing of their business combinations and avoid situations under the NYSE's current rule where a SPAC that fails to complete a business combination within three years of listing is faced with the option to liquidate, transfer to an exchange that affords a longer completion period, or face delisting, notwithstanding that it has a subsisting business combination agreement. The proposed amendments are intended to foster competition for SPAC listings by bringing the NYSE rules in line with a similar extension in timing available under Nasdaq's rules through discretionary extensions granted by Nasdaq's hearing panels.

On July 9, 2024, the SEC instituted proceedings to determine whether to approve or disapprove the proposed rule change.

NASDAQ DEVELOPMENTS

Nasdaq Proposes to Clarify Phase-in and Cure Periods for Corporate Governance Requirements

On May 8, 2024, Nasdaq filed with the SEC proposed rules to clarify and modify the phase-in schedules for certain of its corporate governance requirements, including its independent compensation and nominations committee requirement and certain of its audit committee composition requirements, and to clarify the applicability and computation of related cure periods. The proposal, which seeks to codify a number of Nasdaq's policies, is generally consistent with similar NYSE rules.

Phase-in Periods

IPO Companies and Similar Companies

If approved by the SEC as proposed, for companies listing in connection with an initial public offering (IPO companies), the rule would:

- clarify that the phase-in schedule that applies to the audit committee independence requirements under Rule 10A-3 of the Exchange Act also applies to Nasdaq's audit committee independence and financial literacy requirements;

- provide that the audit committee's three-member minimum requirement may be phased in as follows: at least one member by the listing date, at least two members within 90 days of the listing date, and at least three members within a year of the listing date;

- modify the timing of the phase-in for the one-member aspect of the independent compensation and nominations committees requirement by providing that one member must satisfy the requirement by the earlier of the IPO closing date or five business days from the listing date (instead of the current listing date timing)—this is to accommodate the common practice of appointing additional independent directors shortly after the listing date but prior to the IPO closing date; and

- provide that the compensation committee's two-member minimum requirement may be phased in as follows: at least one member by the listing date, and at least two members within a year of the listing date.

Under the proposed rule, phase-in provisions similar to those for IPO companies will apply to companies listing in connection with a carve-out or spin-off transaction and those whose public company status are triggered by the total assets and record holder thresholds of Section 12(g) of the Exchange Act. In the case of the latter companies, however, the audit committee independence and financial literacy requirements must be satisfied by the listing date.

Companies That Cease to be Foreign Private Issuers

For the requirements discussed above (including the majority independent board requirement), Nasdaq proposes a six-month phase-in period for a company that ceases to be a foreign private issuer. Such a company will have six months from its most recently completed second fiscal quarter to comply with the requirements, but members of its audit committee must satisfy the Exchange Act's independence requirement during the phase-in period.

Cure Periods

Regarding its cure periods for its majority independent board, audit committee composition, and compensation committee composition requirements, Nasdaq proposes to codify its policy that:

- a company relying on a phase-in period is ineligible for a cure

period immediately after the phase-in period expires, unless the

company is a company (an "initially compliant company")

that complied with the relevant requirement during the phase-in

period but later fell out of compliance before the phase-in period

expired; and

- This rule would allow Nasdaq to immediately commence delisting procedures against non-initially compliant companies that, immediately after a phase-in period expires, are non-compliant with a requirement.

- an initially compliant company would not be considered deficient with a requirement until the requirement's phase-in period ends, and the cure period for an initially compliant company will run from the date of the event that caused the company to fall out of compliance, and not from the end of the phase-in period.

Timeline for SEC Action:The SEC is expected to act on the proposed rules by August 27, 2024.

U.S. EQUITY & DEBT MARKETS ACTIVITY – Q2

2024

(Data sourced from Dealogic)

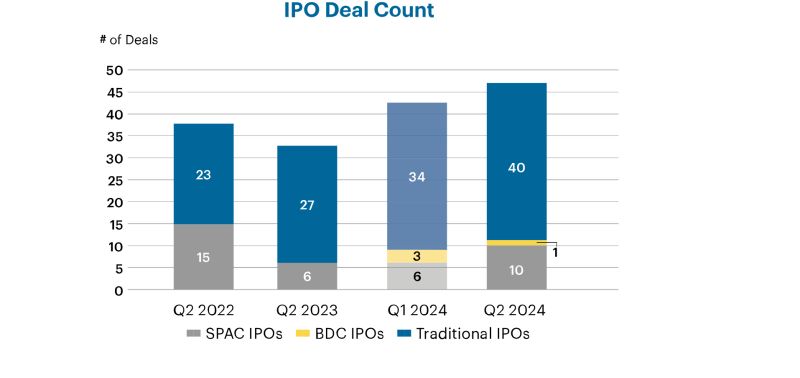

Traditional IPOs

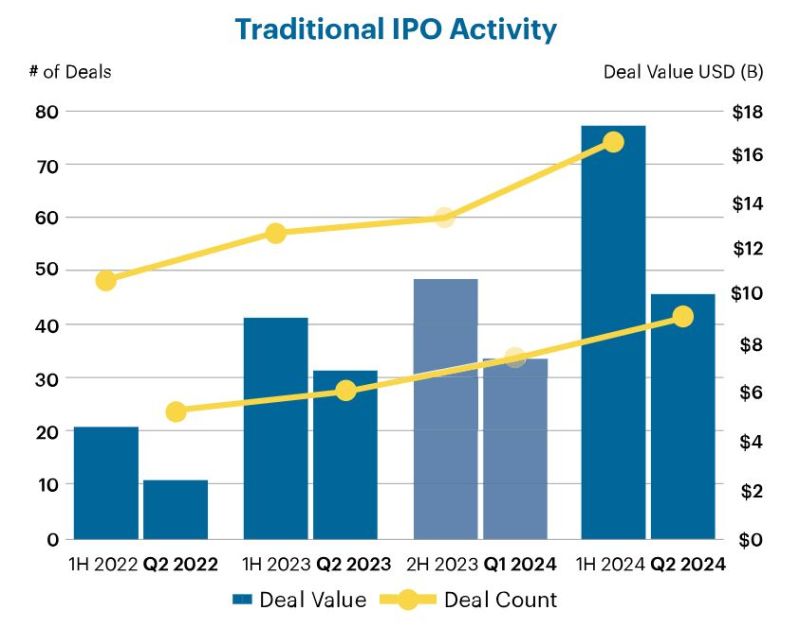

Traditional IPOs continue to show a rebound in activity with deal value and deal count up by 39% and 48%, respectively, in Q2 2024 as compared with Q2 2023. Q2 2024 activity also increased the momentum from Q1 2024, with a 27% increase in deal value and an 18% increase in deal count as compared with Q1 2024. In all, with 74 IPOs ($17.1 billion), the first half of 2024 was markedly better for the traditional IPO market than the first half of 2023 with 58 IPOs ($9.1 billion).

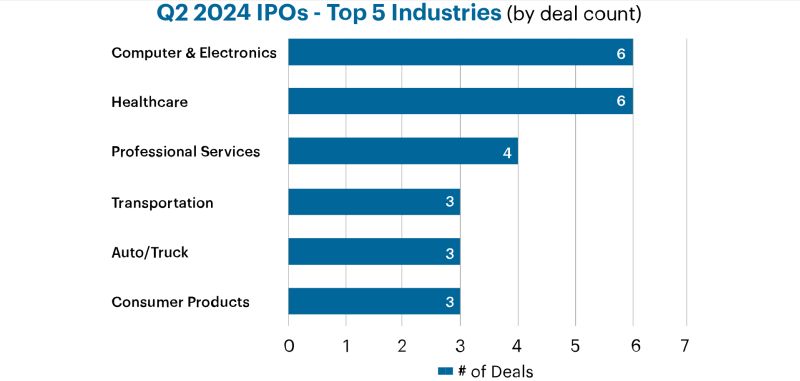

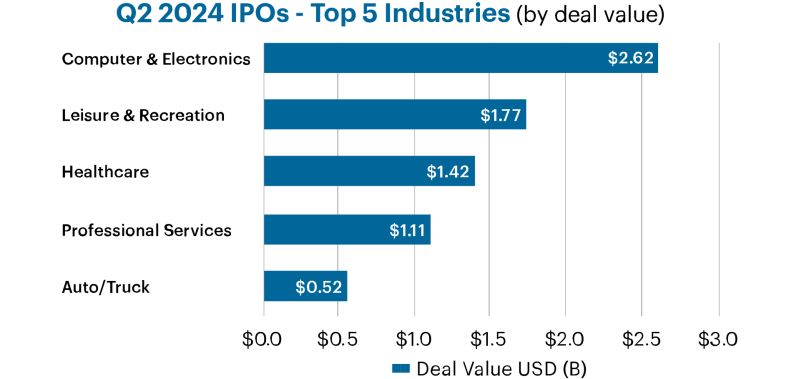

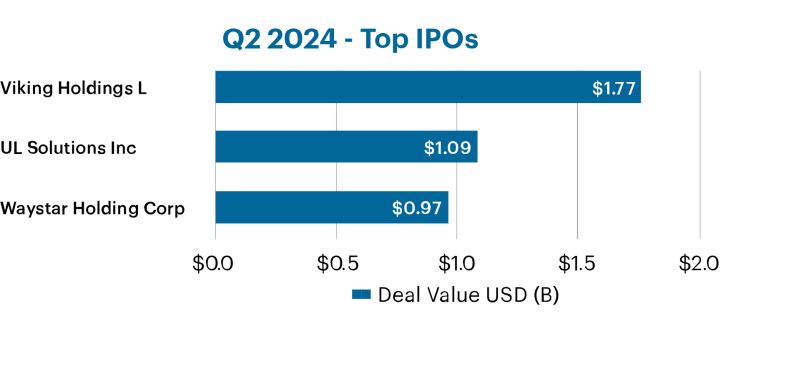

In Q2 2024, the computer and electronics (C&E), and healthcare industries continued their Q1 2024 deal count lead with six IPOs each, down from 11 healthcare IPOs in Q1 2024 and almost flat for C&E IPOs (vs. Q1 2024). C&E IPOs, however, topped the Q2 2024 deal value chart with $2.6 billion in total proceeds. The leisure and recreation industry also made a strong showing with the $1.8 billion IPO by Viking Holdings Ltd, a cruise ships company, being the largest in Q2 2024.

SPAC IPOs

Although there was a 67% uptick in the number of IPOs by special purpose acquisition companies (SPACs) in Q2 2024 as compared to Q2 2023 and Q1 2024, SPAC IPO activity remains minimal, with only 10 SPAC IPOs in Q2 2024. Compliance with most of the SEC's recently adopted rules on SPAC IPOs (and their business combinations with target companies (de-SPACs)), which we discuss here, kicked in on July 1, 2024, and Q3 2024 should offer a glimpse of the likely impact of those rules on SPAC IPOs and de-SPACs.

BDC IPOs

There was only one IPO by a business development company (BDC) in Q2 2024, down from three in Q1 2024. Except for 2021's three BDC IPOs and 2020 and 2023 which had no BDC IPOs, BDC IPOs have been one per year since 2017. 2024's half-year record has, therefore, already surpassed this recent historical record.

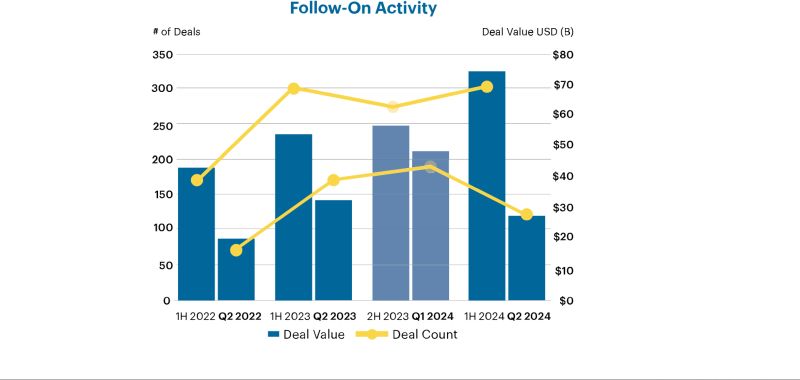

Follow-Ons

As compared to Q2 2023, Q2 2024 follow-on offerings (FOs) were down 14.6% by deal value and 27.2% by deal count. The downturn in activity was, however, more significant as compared to Q1 2024 (down 42.1% and 31.7%, respectively). Despite this lower activity, the first half of 2024 was at par with the first half of 2023 in deal count (303 vs. 302) and surpassed 1H 2023 in deal value by almost 40%.

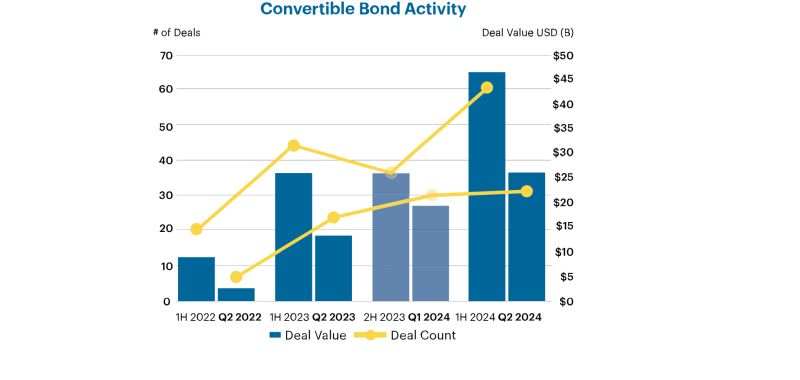

Convertible Bonds

Convertible bond offerings continued their upward trend in Q2 2024, with deal value and deal count more than doubling Q4 2023 levels. As compared to Q2 2023 and Q1 2024, in Q2 2024, deal value was up 95% and 34%, respectively, and deal count was up 35% and 7%, respectively. Convertible bond activity was also significantly higher in 1H 2024 as compared to 1H 2023, up 79% by deal value and 36% by deal count.

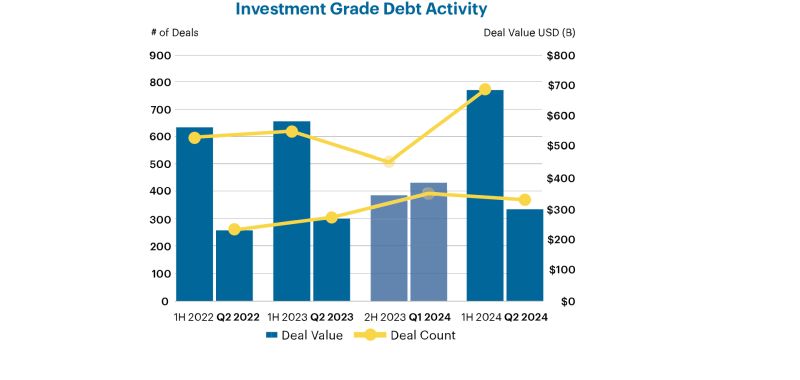

Investment-Grade Debt

While issuance of investment-grade corporate bonds1 was up in Q2 2024 as compared to Q2 2023 (up 9.4% by deal value and 19.2% by deal count), issuance was down as compared to Q1 2024 (down by 22% by deal value and 7.5% by deal count). Notably, investment-grade corporate bonds issuance in 1H 2024 significantly outperformed 1H 2023 with almost a quarter increase in deal count and a 20% increase in deal value.

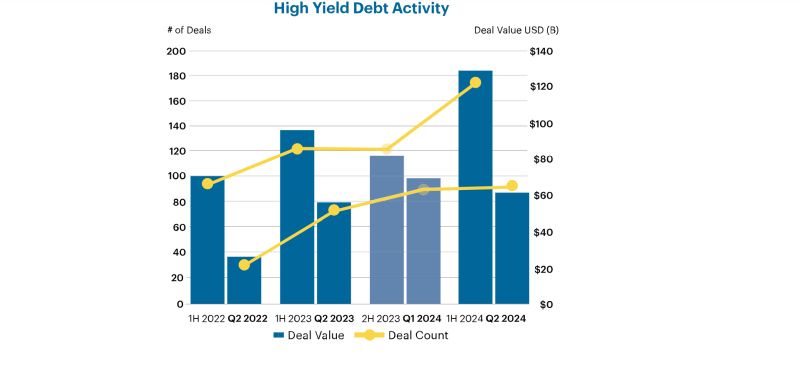

High-Yield Debt

The number of high-yield debt offerings in Q2 2024 only increased slightly over Q1 2024's record-breaking numbers (89 vs. 87); deal value was, however, down by 12%. The number of deals in Q2 2024 was almost 25% more than in Q2 2023, with Q2 2024 up 9.5% in deal value versus Q2 2023.

Footnote

1 Excludes medium-term notes, asset-backed securities, mortgage-backed securities, and short-term debt.