The United States M&A market has shown increased activity in 2024, but its recovery from 2023 levels has been more gradual than some had expected. Stabilizing inflation, stock market highs, stronger corporate profits and increased confidence have fueled a moderate recovery. At the same time, dealmakers remain cautious due to persistent high interest rates (see our article "Private credit market: latest trends and election forecast") and regulatory, legal (see our article "U.S. capital markets: 2024 and beyond") and geopolitical uncertainty. The upcoming U.S. election in November adds additional uncertainty that could slow the M&A market's further recovery in the short term until there is clarity on which party will hold the White House and Congress.

Impact of U.S. presidential elections on M&A

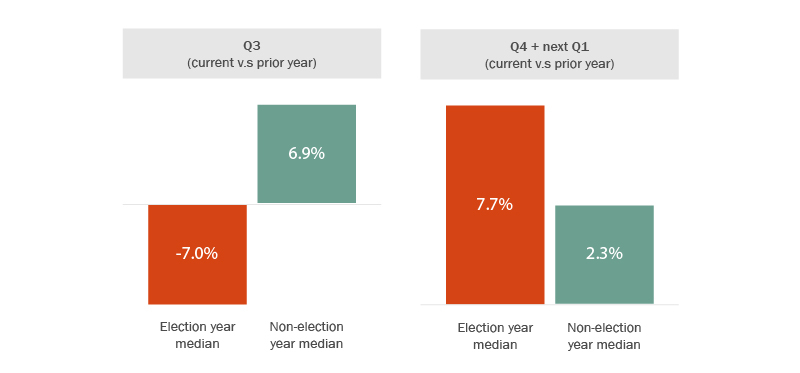

The 2024 U.S. presidential election is approaching quickly, and the M&A community is speculating on its impact on deal activity. Common wisdom among dealmakers is that U.S. presidential elections have more of an effect on deal timing than deal outcomes. Deal volumes in the third quarter of presidential election years are typically depressed relative to non-election years, while relative deal volumes in the first quarter of the year following presidential elections spike by approximately the same amount that they were depressed prior to the election. This "dip and recovery" pattern suggests that some deals are delayed to allow parties to adjust deals for election outcomes—but that most ultimately go through in some form, regardless of the election outcome.

Figure 1: Percent change in number of announced M&A transactions (by U.S. acquirors, 1992 – 2022, excluding 2008).

Source: "Election Uncertainty Leaves M&A, Activism in Limbo", The Deal. Data source: CapIQ, Harris Williams. Data includes U.S. M&A transactions.

The parties' different approaches to antitrust and national security enforcement could impact M&A meaningfully in the coming years (for more, read our article "The next four years of antitrust and foreign investment policies: a look ahead at the 2024 U.S. election"). Many expect a second Trump administration would roll back Biden's executive orders and guidelines that allow novel approaches to antitrust enforcement, particularly against big tech multiplatform companies and private equity roll-up platforms (for more on the private equity environment, read "Secondaries in a challenging fundraising environment" and "Recent trends in U.S. private funds"). And given his Silicon Valley venture capital background, Trump's running mate J.D. Vance (as well as the parade of Silicon Valley billionaires supporting Trump at the Republican National Convention) has sparked curiosity about what a Trump presidency might mean for the technology sector, particularly in light of the enhanced scrutiny of antitrust, privacy and issues in the technology companies during Biden's presidency.

Relatedly, some commentators blame tighter merger regulation under Biden for a drop in the relative proportion of M&A-fueled activist campaigns versus operations-driven activist campaigns during the Biden years. These observers wonder whether a looser antitrust and CFIUS environment under a Trump administration could encourage activists to return to more traditional M&A-fueled activism.

2024 H1 M&A market overview

In the first half of 2024, the global M&A market showed signs of recovery from 2023's troughs, with the global value of M&A activity reaching US$1.0 trillion, which represents a 4% increase compared to the same period last year but remains substantially below a ten-year average of US$1.5 trillion at the end of Q2 1.

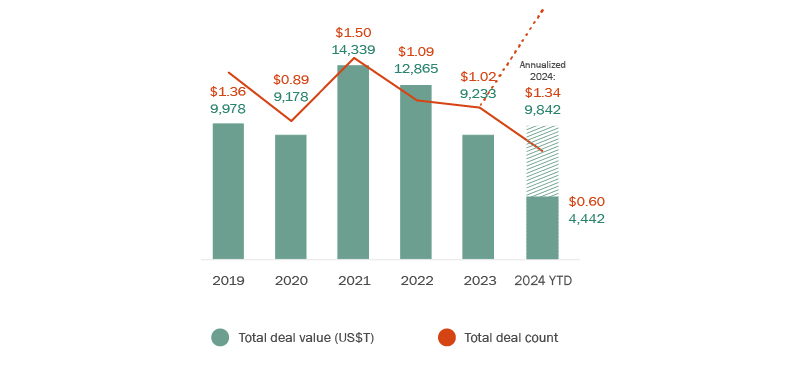

U.S. domestic dealmaking has rebounded more aggressively from 2023, though still lower than the banner years of 2021 and 2022. On an annualized basis, the U.S. domestic M&A market is projecting 9,842 deals for 2024 (versus 9,233 for 2023) and $1.34 trillion aggregate deal value (versus US$1.02 trillion for 2023). See Figure 2.

Figure 2: Deal value and count (U.S. acquiror of U.S. target)

Source: Bloomberg. Based on M&A deals announced during Jan 1, 2022 - June 13, 2024. Excludes terminated and withdrawn deals.

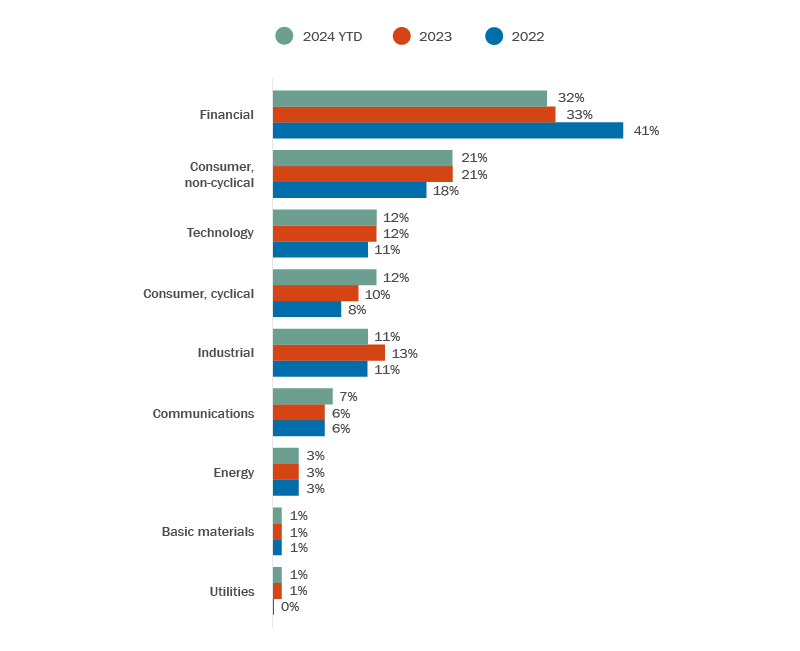

From a sector perspective, the volume of deals in most sectors is consistent with historical averages. Financial services M&A is seeing a spike in overall volume (led by Capital One's $35B acquisition of Discover as well as large deals in the private equity and insurance subsectors). Among the other sectors in which significant deals have transacted so far in 2024 are energy (ConocoPhillips' $36B acquisition of Burlington Resources and Diamondback Energy's $26B acquisition of Endeavor), tech (Synposys' $35B acquisition of Ansys) and basic materials (Home Depot's $18B acquisition of SRS Distribution).

Figure 3: Target industry breakdown (U.S. acquiror of U.S. target)

Source: Bloomberg. Based on M&A deals announced during Jan 1, 2022 - June 13, 2024. Excludes terminated and withdrawn deals.

Canadian inbound investment into the U.S.

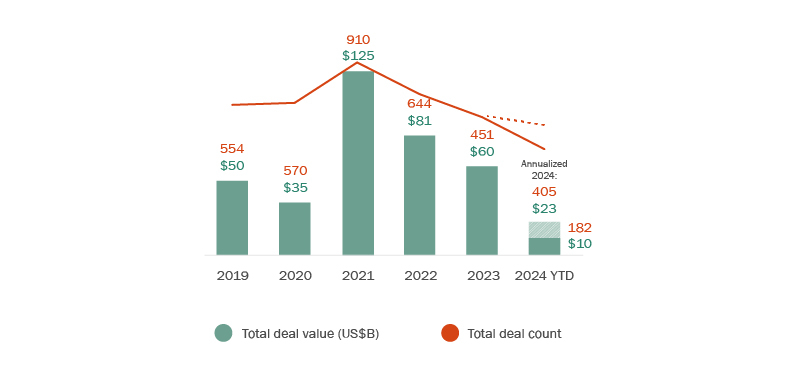

Challenged by high interest rates and low growth, domestic Canadian domestic M&A has experienced low levels in 2023 into 2024. Perhaps not surprisingly, Canadian investment into the U.S. in the first half of 2024 also decreased relative to 2023 levels on an annualized basis, with an annualized value of around US$23 billion compared to US$60 billion in 2023. Annualized deal count for Canadian acquisitions of U.S. targets is at 405 deals, down from 451 deals in 2023, which continues the year-over-year decreases seen since 2021's peak of 910 deals. See Figure 4.

Figure 4: Deal value and count (Canadian acquiror of U.S. target)

Source: Bloomberg. Based on M&A deals announced during Jan 1, 2022 - June 13, 2024. Excludes terminated and withdrawn deals.

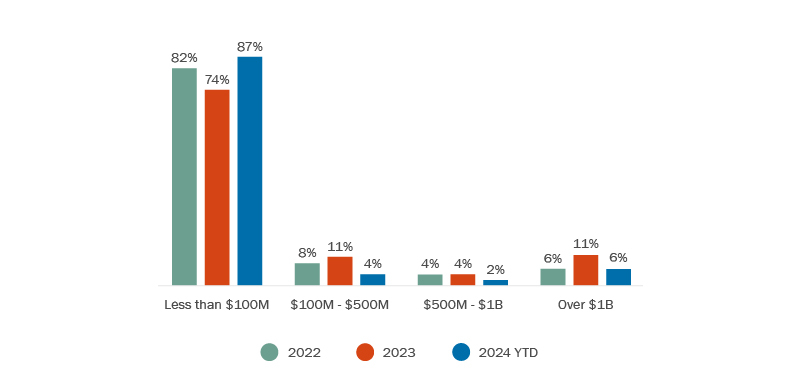

The size of Canadian inbound deals has also continued to decrease. The proportion of southbound deals from Canada into the U.S. with a deal value under $US100M has increased to 87% from 74% in 2023 and 82% in 2022, while deals in the sub-$500M, sub-$1B and $1B+ ranges all remain lower than prior years. See Figure 5.

Figure 5: Deal value range (Canadian acquiror of U.S. target)

Source: Bloomberg. Based on M&A deals announced during Jan 1, 2022 - June 13, 2024. Excludes terminated and withdrawn deals.

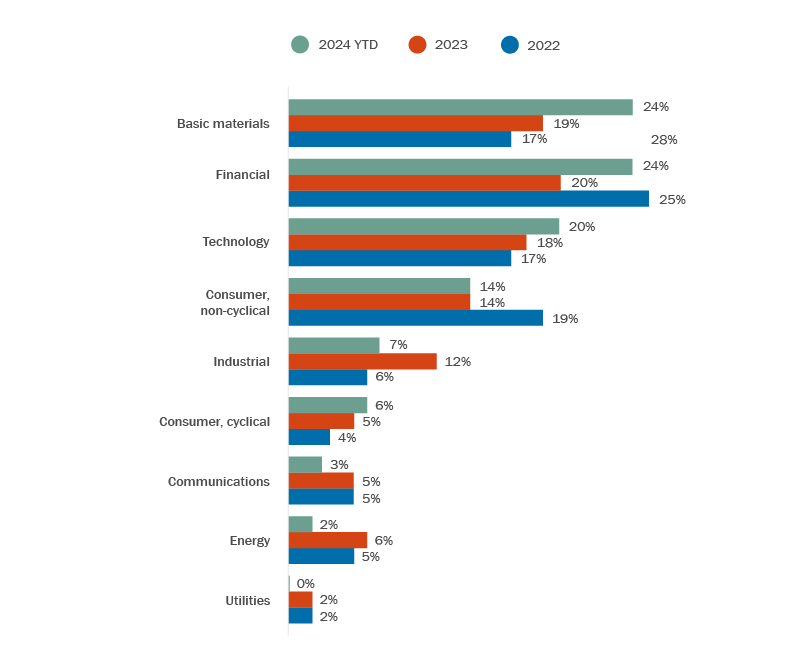

Sector by sector, the relative portion of Canadian acquisitions of U.S. technology firms increased moderately for the first half of 2023, while deals for U.S. industrials, communications, energy and utilities companies declined proportionately (see Figure 6). Consistent with overall sector trends in the U.S. discussed above, Canadian acquisitions of U.S. financial sector companies also bounced back to roughly 2022 levels, and basic materials also made a strong showing.

Figure 6: Acquiror industry breakdown (Canadian acquiror of U.S. target)

Source: Bloomberg. Based on M&A deals announced during Jan 1, 2022 - June 13, 2024. Excludes terminated and withdrawn deals.

Conclusion

Despite the first half of 2024 seeing continued high interest rates and significant regulatory scrutiny on deals, the U.S. M&A markets have seen a substantial recovery from 2023 levels. While Canadian acquirors remain somewhat more on the sidelines in U.S. acquisitions than they have in recent years, they are opportunistically cherry-picking smaller deals, and some are focusing on deals in the most active industries including tech, financial services and basic materials. The U.S. election remains a question mark both domestically and for Canadian acquirors that may hover over M&A decision-making at least into November and perhaps longer.

Footnotes

1 See "M&A Insights H1 2024: The Recovery Continues".

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.