- with readers working within the Banking & Credit and Retail & Leisure industries

UK motorists buying cars on finance before 2021 may have been unaware that car dealers were receiving commission from lenders on the finance package. One common commission model gave the dealer/broker discretion over the interest rate offered, and linked the level of commission to the interest rate agreed. These discretionary commission arrangements (DCAs) for motor finance were banned by the Financial Conduct Authority (FCA) in January 2021.

What the FCA motor finance investigation could mean for the industry

In January 2024, the Financial Ombudsman Service (FOS) published two decisions which upheld customer complaints in respect of DCAs. The FCA then announced it would assess whether the former use of DCAs means that motorists paid too much interest across the motor finance sector and are due compensation from regulated firms.

Analysts at the Royal Bank of Canada forecast that the industry could face redress costs of £16 billion – putting the viability of some lenders in doubt.

In this article, we explore the economics of car-buying, and pose the question of whether the finance arrangements can be unbundled from the deal that the motorist and the dealer/broker strike.

How the economics of a car purchase can vary

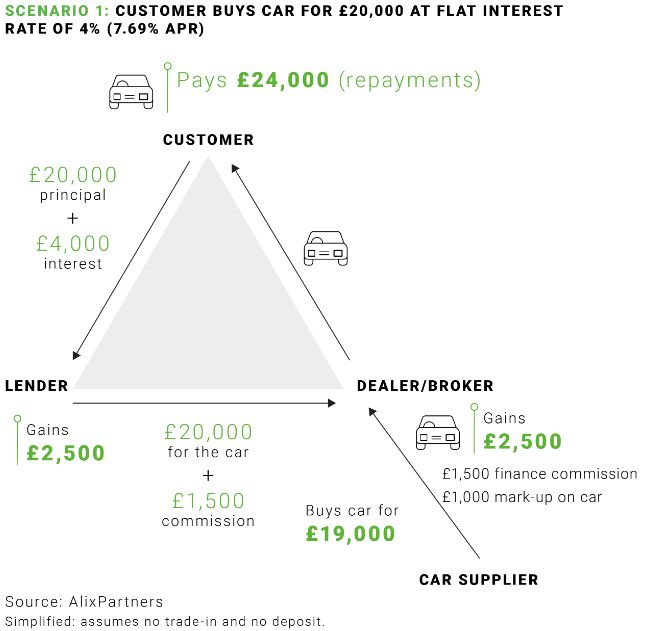

Core scenario:

- A customer, Mrs A, chooses a car with a sticker price of £21,500, which the dealer purchased for £19,0001.

- The car dealer is also a credit broker and selects Lender Z from a panel of lenders.

- Lender Z operates a DCA with the broker. The DCA allows the dealer/broker to take any interest above minimum flat rate2 of 2.5% as commission.

In this scenario (1), DCA is applied at 4% flat. Mrs A negotiates a discount on the new car of £1,500. She agrees to pay the £20,000 net amount through a finance agreement of £400 per month for 5 years. The finance cost, £4,000, equates to an annual percentage rate (APR) of 7.69% (4% flat).

Mrs A ultimately pays £24,000 for the car. Lender Z generates revenue (net of commissions) of £2,500, and the dealer/broker generates commission of £1,500 on the finance deal in addition to the £1,000 profit realised on the car.

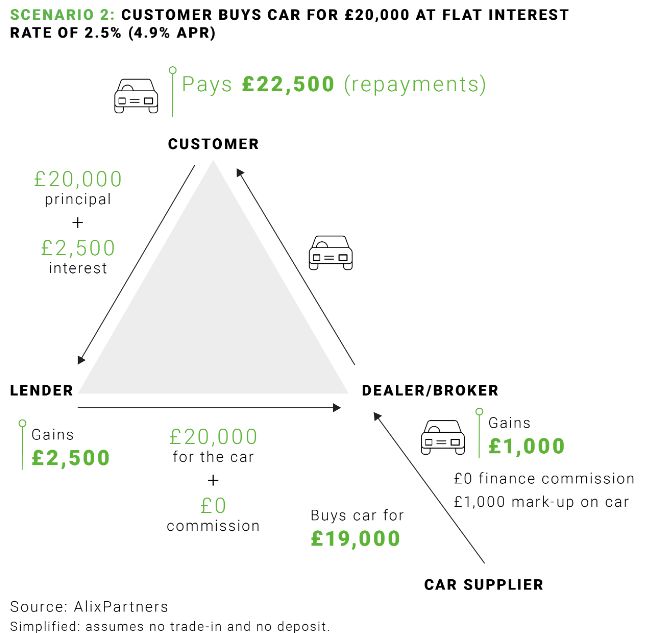

What if the minimum rate of interest is applied (consistent with the FOS decision)?

Scenario 2 illustrates the revised economics of the deal. Mrs A pays £22,500 through 60 monthly repayments of £375 at a flat rate of 2.5% (APR of 4.9%). Lender Z generates the same revenue (£2,500) as there is no commission to pay to the dealer/broker, who is only able to generate profit through the mark-up on the car (£1,000).

Is this realistic? The economics need to make sense to each party for there to be a deal. At a 2.5% flat interest rate, the dealer/broker would not make enough profit; there is no deal.

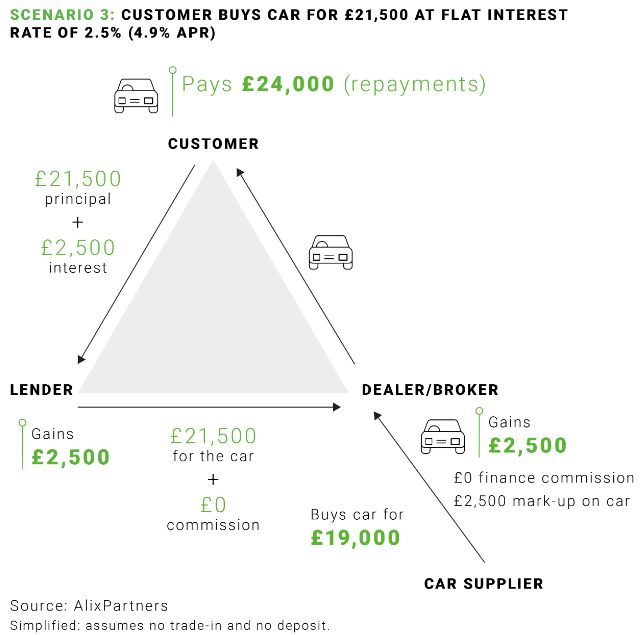

What if the dealer/broker adjusts the price of the car?

If the dealer/broker is restricted to the minimum flat rate of 2.5% (APR of 4.9%) but has discretion on the price of the car then, to realise the same economics, the dealer/broker will only agree to sell the car at a higher price. Mrs A would have to agree to pay the sticker price of £21,500, and commit to monthly repayments of £403.13 for 5 years (Scenario 3).

In scenario 3, Mrs A pays £24,000 for the car, the lender generates revenue of £2,500, and the dealer/broker brings their revenue back to £2,500, replacing the lack of commission with a greater mark-up on the sale of the car. Although the deal structure is different, the economics are the same as where the finance is sold under a DCA.

What can we learn?

The dealer/broker will only agree to a deal that generates sufficient profit, and Mrs A should only agree to a deal if the repayments are affordable and competitive. Although the DCA could establish a conflict of interest between Mrs A and the dealer, Mrs A can shop around for the best-value deal, irrespective of whether there is a DCA in place. The purchase price of the new car, any trade-in value and the finance package agreed are all components within the transaction. For most buyers it is the monthly payment that matters, and this reflects the overall economics of the deal.

Another observation is that, in any scenario, the lender ends up with the same interest (net of commission). Media coverage has to date largely focused on lenders, their role, and their potential financial exposure. But, as these scenarios illustrate, it is the broker who pockets (absent any other arrangements) the proceeds from the application of the DCA. How the FCA chooses to factor this in and apply it to any potential redress scheme remains to be seen.

One distinctive feature of this issue is that we have a ready-made counterfactual, in that we are able to compare how behaviours change without DCAs being available. As the FCA banned DCAs for motor finance in 2021, we can explore three years of data to see what has actually happened following the ban. Do brokers really take zero commission, and if so, did that impact car prices? Or, do they move to a fixed-fee commission arrangement and, if so, at what level is that set? What does this mean for the average cost of car finance relative to when DCAs were in operation – is it more expensive, or have economic forces resulted in equilibrium being restored?

Evaluating this will require sophisticated economic analysis, as over that same period we have experienced increased cost of credit, a pandemic, and a significant increase in the cost of cars, all of which need accounting for.

What are the likely financial implications for the sector?

If the RBC analyst is correct the sector faces costs of £16 billion to compensate customers, costs in the same order as Payment Protection Insurance (PPI). Have motorists really suffered detriment of this significance?

There are other parallels with PPI: the activity of Claims Management Companies (CMCs) and the press in promoting the issue; a flood of claims (including from customers who didn't have motor finance with a DCA, or have suffered no real harm); and uncertainty about how redress might be calculated. Complaints lodged with the FOS surged by 144% year on year for Q2 2023/24. This increase in complaints, coupled with the potential for an industry-wide redress scheme under section 404 of the Financial Services and Markets Act, means that the financial and operational burdens on affected lenders are likely to be substantial and sustained.

The impact on larger lenders is likely to be manageable, in that they are well-capitalised and diversified. Smaller, specialised lenders could see a far greater impact. These lenders, which may have relied heavily on discretionary commission models, could face severe financial strain. In some cases, the cost of compensating affected consumers could threaten the viability of these firms, leading to insolvency or requiring significant restructuring efforts.

What should lenders do to prepare?

As lenders await the FCA's announcement, it would be prudent to take proactive steps to manage the regulatory changes and minimise the financial and operational disruptions that will inevitably arise. The focus areas should include:

- Scenario planning: Lenders need to anticipate a range of regulatory outcomes and develop plans for each. This involves understanding potential regulatory requirements, estimating the financial impact of different redress scenarios, and preparing strategies to address these challenges.

- Impact assessment: Conducting thorough impact assessments would help lenders understand how different regulatory scenarios will affect their financial stability and operational viability. This involves evaluating the potential cost of redress, assessing the impact on capital and liquidity, and identifying any areas of the business that may require restructuring.

- Readiness for action: Given the likelihood that the FCA will impose challenging deadlines to remediate affected customers, lenders must be operationally ready to implement redress schemes swiftly and efficiently – while ensuring that they minimise the operational and financial impact on their business. This might mean engaging experts who can deploy a cost-effective automated solution to execute an effective remediation programme, including automating the identification of affected customers, calculation of redress and production of customer letters.

How can lenders address potential redress liabilities?

Lenders can adopt one of several strategies to manage their financial and operational burdens effectively. These options can be adapted from similar strategies used in other sectors, such as the scheme of arrangement utilised by other financial institutions to address customer claims:

- Proactive engagement with regulators: By cooperating closely with regulators, lenders can negotiate the terms of redress schemes and ensure compliance with regulatory requirements. This proactive approach can also help lenders gain regulatory support for their optimal strategies, facilitating a smoother implementation process and potentially mitigating some of the financial impacts.

- Scheme of arrangement: A scheme of arrangement, as defined under Part 26 of the Companies Act 2006, is a court-approved agreement between a company and its creditors or shareholders. This mechanism allows a company to restructure its debts and liabilities, providing a structured way to handle claims and distribute redress payments. Other financial institutions were able to utilise this tool to manage their potential liabilities, offering customers a route to submit claims while enabling the company to continue operations. Lenders could therefore use a scheme of arrangement as a viable path to manage large-scale redress liabilities.

- UK Restructuring Plan: Introduced as part of the Corporate Insolvency and Governance Act 2020, the UK Restructuring Plan provides a flexible framework for companies to restructure their debts and liabilities. This strategy would be like a scheme of arrangement, but with the addition of allowing a company to impose a plan on dissenting classes of creditors if approved by the court. This tool is particularly useful during complex restructurings and can help lenders manage significant liabilities while maintaining operational stability.

In summary

The coming months will be crucial for the car finance sector and, as the regulator prepares to announce its findings, lenders must brace themselves for potential costs and operational challenges. Proactive planning and readiness will be essential for navigating the regulatory landscape and ensuring compliance, while maintaining financial stability.

How we can help

As a worldwide advisor to companies operating in every major industry sector, our clients benefit from hands-on experience in the industries we serve.

AlixPartners' risk advisory practice helps clients to understand the financial and operational implications of regulatory requirements, proactively build their compliance and risk management capabilities, and respond to urgent regulatory interventions.

Our global automotive practice works hand-in-hand with company leaders to compete in this new disrupted environment. Our new offering, Berylls by AlixPartners, provides clients with the consulting industry's most comprehensive range of expert automotive advice.

We are a leading global provider of turnaround and restructuring services, called

in by investors, creditors, law firms, governments, and corporates

to solve complex problems – when it really matters.

Footnotes

1 For the purposes of this example, we ignore any trade-in value that Mrs A might be able to negotiate as part of this deal. As such, the scenarios here are simplified. In reality, the dealer is able to pull other levers to make the deal attractive.

2 Flat interest rate is used in calculating commissions in certain DCAs. Whereas APR factors in that the principal amount borrowed gradually decreases over the loan term, and the interest charges are effectively front-loaded, flat rate interest assumes the interest charged is apportioned equally across the loan term, based on the original amount borrowed. So, by way of the example cited in the FOS decision, if a consumer borrowed £10,000 over 48 months, and the total amount of interest payable was £4,800, that would equate to a flat rate of 12% (or £1,200 per year).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.