- within Consumer Protection and Antitrust/Competition Law topic(s)

- with Senior Company Executives, HR and Inhouse Counsel

- with readers working within the Transport and Law Firm industries

Michael Bacina, Steven Pettigrove, Jake Huang, Luke Higgins and Luke Misthos of the Piper Alderman Blockchain Group bring you the latest legal, regulatory and project updates in Blockchain and Digital Law.

Clash of titans: ASIC sues ASX

The Australian Securities and Investments Commission (ASIC) has filed a lawsuit against the Australian Securities Exchange (ASX) over its ill-fated CHESS replacement project. In a proverbial clash of titans that pits the country's top financial watchdog against the largest market operator, ASIC accuses ASX of misleading and deceptive conduct, claiming that the exchange misled the market about the progress of the project, which was set to replace the Clearing House Electronic Subregister System (CHESS) with a blockchain system.

ASX embarked on its ambitious CHESS replacement journey in 2015. The project was a bold step towards modernising the way trades are cleared and settled in Australia. By December 2017, ASX proudly announced it would swap out the aging CHESS system for a cutting-edge blockchain-based platform, developed in partnership with an organisation named Digital Asset. The new system promised to enhance security, scalability, and performance, while also catering to the evolving needs of market participants. It was also peak hype around blockchain with many other financial giants exploring the technology.

From 2016 onwards, the project seemed to be progressing as planned, with industry engagement, testing phases, and the gradual release of technical documentation. However, as the years continued to pass, the initial excitement began to wane. By 2022, ASIC alleges in its recent post, the wheels seemed to have come off the blockchain bandwagon, and ASIC alleges that ASX's assurances that the project was "on track" were, in fact, far from the truth.

ASIC's action centers on a series of announcements made by ASX in February 2022 where the exchange claimed the project was still on course for its April 2023 go-live date and was "progressing well." According to ASIC, these statements were misleading as at that point, the project was not progressing according to plan, and ASX allegedly had no reasonable basis for its promising updates.

ASIC Chair Joe Longo didn't mince words, calling out ASX for what he described as a "collective failure" by the board and senior executives:

[The] critical importance [of the CHESS replacement] was all the more reason ASX needed to ensure it told the Australian public the truth about how the project was tracking and whether it would be completed on time.

This serves as a cautionary tale about the perils of overpromising and underdelivering—particularly when cutting edge technology of any kind is involved. Blockchain, often hailed as the future of finance, carries immense potential for transforming industries. However, as a foundational technology, managing stakeholders and complicated interfaces of ageing computer systems with a completely new way of moving information can be more expensive and time consuming than anticipated.

The ASX's new program to replace CHESS is still likely to utilise blockchain technology, but it will be a number of years before it is rolled out. There is no word yet on whether the ASX will defend the ASIC claim.

ATO rules on Digital Surge creditor claims

The ATO has published a Class Ruling in relation to the tax treatment of creditor claims and administration processes flowing from digital currency exchange Digital Surge's administration. A Class Ruling is a type of public ruling that aims to explain the tax outcome of a specific transaction or dealing to a specific class of persons. The primary purpose of a class ruling is to provide certainty to persons and otherwise obviate the need for individuals to seek their own private rulings.

Background

Less than a month after FTX was placed into bankruptcy in November 2022, Digital Surge entered voluntary administration as a significant proportion of its assets were under the control of FTX pursuant to a broker agreement entered into between the two exchanges. At the second meeting of creditors, it was resolved that the company would enter into a Deed of Company Arrangement.

A Deed of Company Arrangement, or a DOCA, is a document whereby the reconstruction of an insolvent company's business as approved by its creditors is implemented. Through a DOCA, a company can continue to trade and can otherwise rely on the financial compromise aspects of the DOCA in relation to creditor claims. For creditors, there are advantages to a DOCA, as there is the potential for a better dividend than would be received if the company had gone into liquidation.

However, while the company is subject to a DOCA, the words "subject to deed of company arrangement" must be inserted in brackets after the company name on every public document and instrument. One way to avoid this is to use a creditors' trust arrangement by which the company is quickly moved from a DOCA and into another arrangement. A creditors' trust arrangement typically involves changing creditor rights against the company into rights as beneficiaries of a trust whose funds are set up by the DOCA. This was the case for Digital Surge, who shortly terminated the DOCA and entered into a Creditors' Trust.

Unlike an ordinary insolvency process which involves creditor claims being primarily denominated in fiat currency, Digital Surge's circumstances posed an interesting question – if customers deposited crypto-assets into the exchange, and the exchange went bankrupt, what would they be entitled to? Crypto-assets, or perhaps the AUD-equivalent amount of fiat currency?

The terms and conditions of the Digital Surge exchange meant that customers deposited crypto-assets and fiat currency into accounts maintained by the company. However, once customers transferred funds, Digital Surge became the legal owner of the assets. Instead of a direct ownership right over the underlying assets, customers held a right to demand payment from Digital Surge. This payment was to be based on the value reflected in their accounts, but the form of payment – whether in crypto-assets or fiat currency – was at Digital Surge's discretion.

Under insolvency rules, the value of creditors' claims was locked based on crypto-asset prices at the point in time of administration.

Questions before the ATO

The ATO was asked to consider the possible tax events that would arise from the above arrangements. At a high level, the ATO's findings are as follows:

- There are no income tax consequences for

certain creditors following:

- the appointment of administrators of Digital Surge;

- the execution of the DOCA; or

- the settlement (i.e., creation) of the Creditors' Trust,

- There is a capital gains tax (CGT) event for

certain creditors following:

- the termination of the DOCA (Taxable Event A); and

- when the Creditors' Trust makes payments to creditors (now "beneficiaries" of the Creditors' Trust) (Taxable Event B).

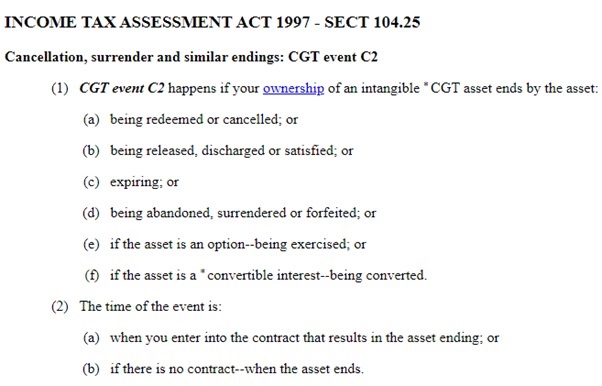

A CGT event occurs when there is a transaction or change in ownership in relation to a CGT asset. A CGT asset can include most forms of property, including intangible property such as a legal right to payment from another person. A capital gain will occur when the capital proceeds from a CGT event exceed the cost base of the CGT asset. A capital loss will occur when the capital proceeds from a CGT event are less than the cost base of the CGT asset.

The CGT event that occurs under 2(a) and 2(b) above is CGT event C2. Pursuant to section 104-25 of the Income Tax Assessment Act 1997 (Cth) (ITAA 97), CGT Event C2 occurs when an intangible CGT asset is cancelled, surrendered, satisfied, or "ended" in a similar manner:

Taxable Event A

When the DOCA was terminated, the ATO has ruled that CGT event C2 occurred for creditors as their claim under the DOCA was effectively released. However, this claim was "replaced" by an equivalent AUD-value entitlement against the Creditors' Trust which was set up contemporaneously to the DOCA termination.

The proceeds from the CGT event C2 therefore are the total of any money or market value of property received in respect of the event. By way of example, the likely effect of this is as follows:

- A creditor has an AUD $10,000 claim against the company;

- the DOCA is terminated, whereby the creditors release their claims against the company;

- given the terms of the Creditors' Trust and DOCA, the creditor's claim against the company is replaced with a claim as a beneficiary of the Creditors' Trust for an equivalent amount ($10,000);

- no capital gain or loss occurs as the proceeds are equivalent to the cost base (i.e., $10,000 – $10,000 = $0).

Taxable Event B

When the Creditors' Trust makes a payment to a creditor, CGT event C2 occurs as the creditor is effectively having part of their CGT asset (being the right to receive payment) satisfied.

The proceeds from the CGT event C2 are equivalent to the market value of any money or property received from the Creditors' Trust. However, the cost base is calculated in a modified manner in accordance with the apportionment rule in section 112-30(3) of the ITAA 97. This means that if a creditor receives a partial payment, their cost base for the given CGT event will be proportional to how much of that payment makes up of the total claim. By way of example, the likely effect of this is as follows:

- a creditor has an AUD $10,000 claim against the company that is converted into a $10,000 right to payment from the Creditors' Trust;

- the Creditors' Trust makes a payment of $5,700 to the creditor;

- the creditor's proceeds are $5,700;

- the creditor's cost base is also equal to $5,700 due to the apportionment rules;

- no capital gain or loss occurs as the proceeds are equivalent to the cost base (i.e., $5,700 – $5,700 = $0).

For Digital Surge's creditors, the ATO ruling means that the effect of the administration process and distribution process is tax neutral.

A copy of the Digital Surge class ruling can be found here.

Conclusion

The Class Ruling provides helpful clarity for creditors of Digital Surge. By recognizing that no capital gain or loss arises when a creditor's claim is effectively replaced with an equivalent right under the Creditors' Trust, the ATO ensures tax neutrality. This is particularly important for creditors, who should not face tax consequences merely due to the insolvency process or through the ordinary course of dealing with their crypto-assets on the platform.

ASIC flips Qoin with appeal on scope of authorised rep exemption

In May, ASIC scored a win in its legal action against BPS Financial Pty Ltd (BPS) with Justice Downes of the Federal Court finding that BPS had carried on an unlicensed financial service when offering the "Qoin Wallet" to consumers as it did not have a valid Corporate Authorised Representative (CAR) arrangement in place with a financial services licensee during certain periods of time. The Court also found that BPS had made certain misleading representations in relation to its product offering.

However, the Federal Court rejected ASIC's attempts to argue that the blockchain platform developed by Qoin formed part of the unlicensed "financial product" under Australian law. Justice Downes also rejected ASIC's long-standing position (as reflected in Regulatory Guide 36 and Information Sheet 251) that the authorised representative exemption cannot be used by a CAR to issue a financial product on the basis that issuance by its nature can only be carried on by a principal and that a CAR, as an agent of a licensee, cannot offers financial services as principal.

This week ASIC confirmed that it has appealed Justice Downes rejecting ASIC's position on whether the CAR exemption is broad enough to allow a CAR to act as an issuer of a financial product, defending its long-standing guidance with potentially significant implications for the scope of the CAR regime and the types of services which can be offered by an authorised representative under another's license.

The "authorised representative" exemption allows a person or entity to provide a financial service under the Corporations Act on behalf of the holder of an Australian Financial Services Licence (AFSL) as the authorised representative of the license holder under a written agreement, without having to hold an AFSL itself. It is one of the more common exemptions relied by many financial service providers, including in the payments industry.

As part of this exemption, an AFSL holder may enter what is known as "Corporate Authorised Representative Agreement", referred to as a CAR agreement, with a licensed entity within or outside of its own group structure.

ASIC's long-standing view, as outlined in ASIC Regulatory Guide 36 and Information Sheet 251 is that the exemption is only available to persons acting as an "agent" of the AFSL holder, but cannot be relied upon if the person is acting as a "principal" (i.e., by actually offering or issuing the particular product).

However, in the BPS decision, Justice Downes found that, among other things, the defendant could rely on the authorised representative exemption in respect of the period in which it was covered by the AFSL of PNI Financial Services Pty Ltd as the terms of the CAR agreement properly authorised BPS to issue the relevant financial product and to provide financial product advice. In this case, the product that BPS issued was a crypto payment product called Qoin Wallet.

In reaching this view, Justice Downes said that the exemption is available to an authorised representative regardless of whether it is acting as an agent for the AFSL holder. In other words, the exemption allows the authorised representative to act as a principal and issue financial products on its own behalf, including a payment product like the Qoin Wallet.

The decision sparked heated debate among financial services experts and industry professionals, as it not only challenged ASIC's posture which was widely accepted by the industry, and potentially foreshadowed a broader ability for authorised representatives to issue financial services under a CAR arrangement.

In the circumstances, it is not surprising that ASIC has chosen to challenge Justice Downes' decision, although the fact this has only come to light now through a note inserted in Information Sheet 251 and an editor's note to an earlier ASIC Press Release is surprising given the potentially significant implications of the appeal for the financial services industry. The note does not explain the potential consequences of the BPS litigation or Justice Downes' view on the correctness of ASIC's guidance which otherwise remains unchanged.

ASIC's update to Information Sheet 251 states:

Note: The decision in ASIC v BPS Financial Pty Ltd [2024] FCA 457 is relevant to this information sheet. The decision confirmed that, to rely on the intermediary authorisation exemption under section 911A(2)(b), the product provider must be a separate person from the person making the offers.

The decision also addressed the question of whether BPS Financial Pty Ltd was entitled to rely on the authorised representative exemption under section 911A(2)(a). ASIC has appealed part of the judgment in this matter in relation to the operation of the authorised representative exemption under section 911A(2)(a): see Editor's Note 2 in Media Release (MR 24-090) ASIC wins first court outcome regarding a non-cash payment facility involving crypto assets (3 May 2024). In our appeal, ASIC has not challenged the court's findings in relation to the intermediary authorisation exemption. We will update this information sheet once there is a decision in the appeal proceeding.

Meanwhile, Justice Downes' finding and reasoning in identifying the scope of the unlicensed financial services offered by BPS (which was confined to its wallet product) remains undisturbed with potentially significant implications for the legal treatment of blockchain based product offerings.

At this stage, no date has been set for the hearing of ASIC's appeal. The appeal will be watched with interest given its potentially significant implications for the scope of the Australian financial services licensing regime and the authorised representative exemption.

A lawsuit a day? Songwriter Sues SEC

Jonathan Mann and Brian L. Frye have filed a lawsuit against the Securities and Exchange Commission (SEC), seeking to protect their digital artwork, which was sold as non-fungible tokens (NFTs) from being subjected to regulatory oversight.

The lawsuit, filed in the US District Court for the Eastern District of Louisiana, aims to address a particular interpretation of the landmark 1946 Supreme Court ruling in SEC v. W.J. Howey, which has long defined what constitutes an "investment contract" under US securities laws (commonly referred to as the Howey Test).

The artists argue that the SEC's recent application of the Howey Test to NFTs is an overreach of the SEC's authority. According to the complaint, the SEC has been leveraging the Howey Test to classify the sale of NFTs as securities offerings, which has led to regulatory actions against NFT sellers in the past year.

While a recent report found that US intellectual properties law is adequate in categorising and dealing with NFTs, the same certainty does not apply to sales of artist's NFTs. The plaintiffs contend that the SEC has not provided clear guidance on when sales fall under its jurisdiction and that a song sold as an NFT is not within the SEC's wheelhouse.

Mann, who holds the Guinness World Record for most consecutive days writing a song plans to sell over 10,000 NFTs, each featuring a unique remix and a digital image of one of his songs, while Frye creates artwork based on legal scholarship and plans to sell 10,000 digital editions of conceptual artwork. Both hope to make royalties on each resale of the NFTs.

The lawsuit seeks a declaratory judgment that their upcoming NFT projects do not violate the SEC's rules and asks the court to pre-emptively block the SEC from taking enforcement action against them for not registering their NFT projects as securities.

This legal battle could have far-reaching implications for the NFT market, which saw explosive growth in 2021, including high-profile sales like the $69 million NFT artwork auctioned by Christie's, before succumbing to a market slump. The outcome may set a precedent for how digital assets are regulated in the future, providing much-needed clarity for artists, creators, and investors alike.

The SEC has yet to comment on the lawsuit, and there is no guidance available, nor any practical or affordable way, for any artist to seek to sell their art based NFTs as a financial product or security, so if these artists are not successful and the SEC continues to assert that art based NFTs are securities/financial products, artists will not enjoy the same tech-neutrality that applies to selling their artwork in other formats, and will lose out on the potential automation of royalty collection offered currently by blockchain and token based smart contracts.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.