Japan's aviation policy has been focusing on building more airports and expanding the network of routes. This policy of "building and expanding" was made possible by the airport development special account (so called "the pool system"), where revenues from all airports are collected into one account and then re-distributed. At present, there are 98 airports in Japan, among them 28 are controlled by the national government and the rest by the local governments.

The policy of "building and expanding" had a certain level of rationality during the period of population increase and rapid economic growth when the airport users were increasing. However, under the present circumstances, including Japan's declining population and low economic growth as well as the financial crunch of the country, a re-examination of the policy is unavoidable and necessary. The balance of income and expenditure of the 25 state-controlled airports indicates that 20 of them are running a deficit (for the financial year of 2011). Also, the combined loss of all the 25 airports totalled 22.3 billion yen1.

In light of these facts, the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) declared at its 13th Growth Strategy Council that the aviation policy would undergo a paradigm shift from "building and expansion" to "efficiently using what have already built". MLIT announced a number of strategies for that purpose, including a strategy for achieving a fundamental efficiency through the use of private sector knowledge and funds2.

I. PRESENT ISSUES OF THE AVIATION POLICY

The following are the present issues identified by MLIT:

- The Pool System: The development, maintenance and operation of the national government-controlled airports is managed with the airport development special account, income sources. Those accounts include the airport user fees e.g. landing fees paid by airline companies, as well as funds transferred from the general accounts of the national government. Subsidies to the local government-controlled airports are also paid from the airport development special account. As a result, all the development, maintenance and operation of the airports, including the poorly-used non-profitable ones, have been managed with one purse. This has resulted in the loss of incentives for greater management efficiency and governance.

- Two-Tiered System: In most domestic airports, the national or a local government builds and maintains the airport infrastructure, including runways and taxiways. It also receives aviation related revenues, including landing fees. While airport related businesses, including airport buildings, are the recipients of non-aviation related revenues such as sales of goods, parking fees and tenant rents as a separate organization (This is referred to as the "two-tiered system".). Moreover, landing fees etc. are set out in a ministry notice that determines tariffs.

They are basically uniform throughout the country, as the balances of income and expenditure of all the airports are taken into consideration. As a result, even airports that earned sufficient profits in non-aviation related sectors is unable to establish a profitable business model, such as those generally used in foreign airports. Many foreign airports use non-aviation related profits as a revenue source to lower landing fees and facilities user fees. These lower fees encourage greater use of airport. Without such a business model the airports in the two-tiered system are unable to strengthen their competitiveness.

II. "STUDY GROUP ON FUTURE AIRPORT OPERATIONS" ORGANISED BY MLIT ("STUDY GROUP")

1. The Study Group

The Study group was formed to implement the strategies adopted in December 2011 at MLIT's 13th Growth Strategies Council. The purpose of the Study group is to discuss means for airport privatisation and how to use private sector airport management (concessions), to integrate the management of airports and airport related businesses.

The Study group has met nine times to date. The meetings have included participation by academics, financial institutions, PPP related players, domestic airlines, airport buildings companies, airport companies and local public corporations. They have addressed the following 4 issues:

- promotion of the management integration of aviation related businesses and non-aviation related businesses;

- implementation of airport management by professional managers, bringing in private sector knowledge and funds;

- solicitation of proposals from the public on airport management reforms and incorporation of local views; and

- utilisation of private sector expertise and experience to implement airport management reforms.

2. Study Group Report (draft)

On July 29, 2011, compiling the study results, the "Study group report on future airport operations (draft)" was published. It outlines the following:

- Importance of bringing up the management of domestic airports to world standards at the time when competition among world airports is escalating with the advancement of airline liberalisation. To achieve that goal, a shift to an unified management system from the current two-tier system is essential.

- Importance of implementation of airport management by professional managers, bringing in private sector knowledge and funds, along with unified management. Under the recently revised PFI law, a system called a "concession" is envisaged as a main means of achieving this. With a concession system the operating rights to airline related businesses and non-airline related businesses ("Operating rights to public facilities") are integrated and assigned to the private sector airport operating entities, while keeping the ownership of the land with the national government.

- Steps are needed to properly assign such operations to the private sector. For example, prior to inviting proposals to become an airport operating entity, a process of market sounding should be conducted. The market sounding solicits a broad range of opinions from the private sector, including investors, that desire to operate airports and existing terminal businesses. Issues dealt with include the suggested new form for the operations and methods of management, taking into account the situation of each individual airport and region. If substantial management and cost improvements can be achieved through cost reduction, networking and unified management of multiple airports, it will be necessary to consider a method of 'bundling', where operating rights to public facilities in multiple airports are bundled and assigned together to the private sector.

- The drive for unified management and 'bundling' requires expertise in administration, negotiation know-how and business operations. That is non-existent in the present day administration. It is, therefore, essential to build a system where the central government remains in the centre, while aggressively utilising private sector expertise and experience as well as sharing and accumulating their know-how

- Study on overseas examples such as London City Airport would be useful.

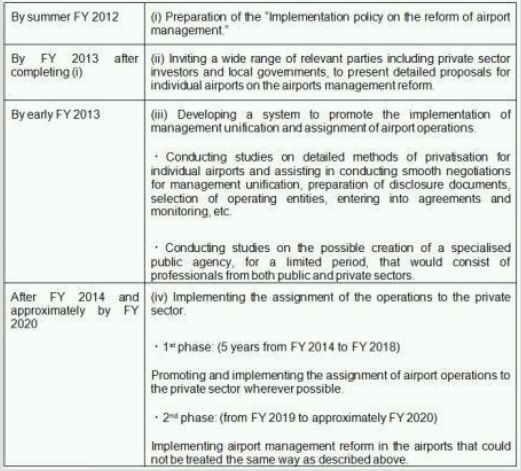

3. Time-line:

(Courtesy: Davis LLP)

III. ONGOING PROJECT KANSAI-ITAMI AIRPORT INTEGRATION PLAN:

In order to improve the fiscal health of the Kansai International Airport ("Kansai Airport") that has outstanding debts of 1.3 trillion yen, the government has been seeking to integrate the Kansai Airport with the nearby Osaka International Airport (Itami) and to assign the integrated operating rights for both airports to the private sector under an operating agreement ("concession agreement"). To achieve this goal, the Act for unified and effective establishment and management of the Kansai International Airport and Osaka International Airport was passed on May 17, 2011, and proclaimed on May 17, 2011.

This plan also aims to establish the company to be called "New Kansai International Airport Co., Ltd." by April 2012. The management of both airports will be integrated in July, 2012, after the company's general shareholders' meetings. The plan is to assign the operating rights of both airports under a concession agreement for a period of 30 to 50 years. It is expected the assignee under the concession agreement would be investment funds, so that the proceeds could be used to repay the debts of the Kansai Airport by the fiscal year 2014 at the earliest.

Footnotes

1. According to the MLIT's press release on July 26, 2011.

2. According to MLIT Growth Strategy Council Report, 3. Aviation Sector, May 17, 2010.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.