WHAT IS THE SHARING ECONOMY?

The current international tax system was established on principles dating back to the first half of the 19th century, when the internet did not exist and the economy mostly consisted of brick-and-mortar stores. Back then, a foreign entity would generally have a taxable presence in a host country if the entity had a certain level of physical presence in that country to which income generation could be linked. Such taxable presence is referred to as a "permanent establishment." But with the advent of the internet came the rise of the digital economy, and what has evolved is a mix of brick-and-mortar and online stores.

As the purchase of services and goods was gradually dematerialized and internet giants such as Google or Microsoft appeared, governments struggled to keep up. The growth of digital economy brought increased scrutiny of tax structures1 set up under laws designed for brick-and-mortar stores. Most recently, governments around the world have shifted their focus to a relatively new part of the digital economy called the "sharing economy." The I.R.S. describes it as follows:

The sharing economy typically describes situations where the Internet is used to connect suppliers willing to provide services or use of assets — apartments for rent, cars for transportation services, etc. — to consumers. These platforms are also used to connect workers and businesses for short-term work.2

Well-known examples of companies that utilize the sharing economy are Uber or Airbnb.

Uber is an electronic platform that is linked to an app. This app connects independent drivers with potential customers, by enabling customers to request a car and using geolocation to pair them with nearby drivers. Once a driver accepts the request and completes the ride, the customer's bank card, which is registered on the application, is immediately charged.

Like Uber, Airbnb is also an electronic platform linked to an app. Customers can use both the app and the Airbnb website to find a host who will rent them an apartment, room, or other accommodation to use while they are travelling. Hosts receive payment for the accommodation through the Airbnb platform.

Both Uber and Airbnb have worldwide operations and use a similar international tax structure. And both companies are dipping deep into the market shares of traditional businesses in the transportation and hospitality industries, respectively.

THE CHALLENGE OF TAXING THE SHARING ECONOMY

The Uber Structure

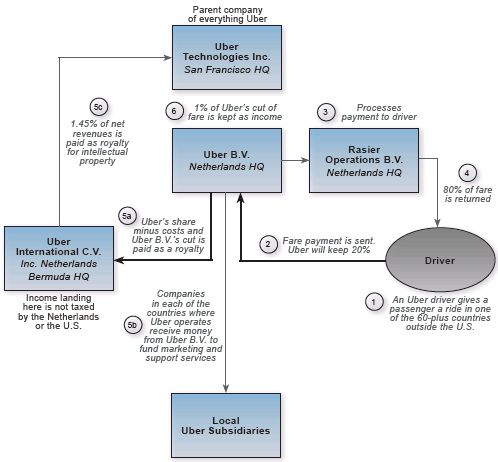

Uber's structure is comprised of a dense worldwide network of holding companies, limited partnerships, and local operating companies. Since Uber's is a privately held company, details of the exact structure are not publicly available. To the extent it is understood, the international structure can – in a simplified form – best be illustrated as follows:3

- Uber Technologies Inc. ("Uber U.S.") is a Delaware corporation with over 135 direct or indirect subsidiaries, both inside and outside the U.S.

- Among these subsidiaries is Uber International C.V. ("Uber C.V."), an entity with no employees, formed in the Netherlands, that has its headquarters in Bermuda. It is not considered taxable in the Netherlands, and Bermuda has no corporate income tax.

- Uber C.V. holds the non-U.S. subsidiaries of Uber U.S.4 As of 2014, these local operating companies have been held by Uber C.V. via two Netherlands-based holding companies organized in the form of private partnerships, Uber International Holdings B.V. and Uber International B.V.5

- In 2013, Uber C.V. and Uber U.S. entered into an agreement pursuant to which Uber C.V. paid a one-time fee of approximatively $1 million to Uber U.S., along with a royalty of 1.45% of future net revenue, for the right to use Uber U.S.'s intellectual property ("I.P.") outside the U.S.

- Uber C.V. and Uber U.S. also entered into a cost-sharing agreement pursuant to which they agreed to share the costs and benefits of I.P. developed in the future.

- Another Uber subsidiary, Uber B.V. (also a Dutch entity), processes the worldwide payments of all Uber rides. Every ride payment is sent to this entity. After deducting payouts to the local drivers (generally, 80% of the ride fare), the balance of revenues is kept by Uber B.V.

- Uber B.V. then pays the local Uber (operating) company a small fee for its services, including marketing. The fee is determined based on costs of the local operating company plus a mark-up (e.g., 8.5%). The mark-up is effectively the profit that is taxed in the local jurisdiction.

- Pursuant to an I.P. licensing agreement between Uber C.V. and Uber B.V., Uber B.V. also pays a royalty fee to Uber C.V. for the use of the I.P. This leaves Uber B.V. with an effective 1% of revenue. (Remember, Uber C.V. holds the I.P. it received in 2013, plus its share of any I.P. developed in collaboration with Uber U.S.)

By using low-tax jurisdictions and having transferred its I.P. out of the U.S., Uber is able to generate substantial profits and pay very little tax. Under current law, the tax effect of the structure for the various jurisdictions may be summarized as follows:

- Under the agreement between Uber C.V. and Uber U.S., the latter's income consists of the (minimal) 1.45% royalty fees it receives from Uber B.V. This amount is then subject to U.S. income tax.

- The timing of the two arrangements between Uber C.V. and Uber U.S. was prior to Uber's substantial increase in value (allegedly $330 million rather than $3.5 billion), which effectively allowed Uber to shift the I.P. out of the U.S. at as low a cost as possible. Under the same agreement, future profits from the exploitation of the Uber I.P. outside the U.S. will be non-U.S. source and thereby sheltered from U.S. Federal income taxation under current rules.

- The royalty payments pursuant to the agreement between Uber C.V. and Uber B.V. are not taxable under Dutch tax laws.

- On a local level, 80% of the ride fares are ultimately earned by the independent Uber drivers. The local Uber operating company receives only a small percentage of income, which is then subject to tax. Furthermore, local tax authorities are potentially subject to substantial losses should the drivers not comply with local income reporting obligations.

The Airbnb Structure

Airbnb uses a similar structure. However, instead of using Dutch subsidiaries, it channels its income through Ireland and Jersey.

Airbnb's European headquarters is located in Ireland. The concept is similar to the one Uber applies, a minimum profit is left in the local operating countries and profits are "bundled" in Ireland via royalty payments to the I.P. company located there. Only residual fees are ultimately paid by the Irish subsidiary to its U.S. parent.

Playing the System: Putting the Traditional Tax Framework on the Spot

From a business perspective, the services offered by Uber and Airbnb are not new: In some areas, brokers have operated as intermediaries between producers and customers for hundreds of years. The difference is that new technology is facilitating this brokerage business to the tune of an estimated $6 billion in revenue for Uber in 2016 (after payouts to its drivers)6 and nearly $3 million in short-term Airbnb rentals in more than 34,000 cities.

While, conceptually, the brokerage business model is not new, Uber and Airbnb share another characteristic that significantly deviates from the tax structures of traditional (brick-and-mortar) businesses: They are highly tax efficient. More specifically, from a direct tax perspective, the structures used by Uber and Airbnb benefit from tax arbitrage – known in a post-B.E.P.S. world as "base erosion."

The majority of profits are shifted to low-tax jurisdictions while only minimal profit is left in the high-tax source jurisdiction. This is achieved by what these companies may deem a smart use of existing tax rules. In the view of local governments and institutions such as the O.E.C.D. and the E.U. Commission, they are clearly qualified as tax abusive. However, these companies find themselves mostly well within the framework of current tax rules.

- Local Presence of an

"IPCo" in the Operating Jurisdiction – Permanent

Establishment ("P.E.") Exposure:

As explained above, under the Uber and Airbnb structures, the local jurisdiction is left only with a residual profit from a services fee. The majority of the profits end up in the hands of an IPCo (i.e., the subsidiary holding the group I.P.) located outside the operating jurisdictions. Under current income tax treaty principles, foreign taxpayers are typically only subjected to the source country's tax regime if they have either a physical presence or a dependent agent negotiating contracts on their behalf in the source country. In comparison, Uber and Airbnb operate via local subsidiaries. Most income tax treaties concluded by the U.S., for example, include a clarification that if a foreign company carries on business in the source state via a subsidiary, it shall not of itself constitute a P.E. A similar provision can be found in income tax treaties based on the O.E.C.D. Model Tax Convention. From a U.S. tax perspective, a number of P.E. authorities illustrate that the separate status of affiliated corporations generally is respected.7 Tax authorities in the subsidiary's jurisdiction may take a deviating view if the local subsidiary is deemed a dependent agent. This would, however, require additional facts, such as legal or economic dependence upon the parent (other than solely by reason of share ownership) and entering into contracts on the account of the parent. Under current treaty rules, a subsidiary, however, cannot be a P.E. if its activities would be merely ancillary in character if performed directly by the parent.8 - Lack of Substance in an IPCo

– Treaty Abuse Exposure:

Current income tax treaties that follow the O.E.C.D. Model Tax Convention (i.e., treaties between O.E.C.D. countries other than the U.S.) do not require that the corporate recipient of royalty income has substance. In particular, these treaties do not contain the so-called Limitation on Benefits ("L.O.B.") clause, which subjects the reduced withholding tax rate (in this case, for royalties on I.P.) to certain conditions.9 Inter alia, these requirements provide that the ultimate beneficial owner must be a qualified individual resident in one of the contracting countries, the recipient or related companies based in the recipient's jurisdiction must meet a certain degree of substance (the "active trade or business test"), or the company must be listed on a recognized stock exchange. In the absence of an L.O.B. clause, the royalties could be paid by the local operating countries with zero, or significantly reduced, withholding tax under an applicable income tax treaty, even if the recipient lacks substance. - Intercompany Arm's Length

Payments – Transfer Pricing Exposure:

s long as the royalty paid by the local operating company conforms with the arm's length standards under its local jurisdiction's transfer pricing rules, local tax authorities will find it difficult to successfully challenge these payments to an IPCo. The same holds true for the service fee paid by Uber B.V. However, the buy-in payment from Uber C.V. to Uber U.S. may not withstand scrutiny by the tax authorities given the significant increase in value that followed the transfer. - I.P. Services v.

Transportation and Hospitality Businesses – V.A.T.

Exposure:

Uber argues that from a V.A.T. perspective it acts as a mere agent of self-employed drivers rather than a service provider. As a result, it deems itself not subject to V.A.T., and in most instances, the drivers will stay below the V.A.T. registration threshold (e.g., £85,000 in the U.K.).

WHERE DO GOVERNMENTS GO FROM HERE?

Globally, tax authorities have become wary of this type of set up, which deprives them of substantial tax revenues at the business entity level. In addition, tax authorities have noticed that independent contractors, such as Uber's drivers and Airbnb's hosts, are not always aware of their tax reporting and filing obligations, which also leads to a substantial loss in tax revenues. On August 22, 2016, the I.R.S. attempted to resolve this issue when it launched the Sharing Economy Tax Center. The site provides education and resources relevant to the taxation of the sharing economy, so that individuals earning income through platforms like Uber and Airbnb can comply with their U.S. filing obligations.

As we have noted, by utilizing technology and the brokerage business model, sharing economy companies are able to generate substantial profits while paying very little tax. With these structures cutting deep holes in source jurisdictions' tax revenues, governments are now taking various approaches to attempt to obtain their fair share. These local initiatives, which can be characterized as income tax, indirect tax, or regulatory focused, will be addressed in the next edition of Insights along with international efforts at the level of the O.E.C.D. and the E.U.

Footnotes

1. These structures were for instance attacked on an E.U. level under E.U. State Aid rules, see the examples of Apple and Starbucks described in " Treasury Attacks European Commission on State Aid – What Next?" Insights 8 (2016).

2. "IRS Launches New Sharing Economy Resource Center on IRS.gov, Provides Tips for Emerging Business Area," news release, August 22, 2016.

3. "How Uber Plays the Tax Shell Game," Fortune, October 22, 2015. Note that this assessment is based on the author's research and may contain inaccuracies. Please further note that the structure will lose major benefits once the E.U. Anti-Tax Avoidance Dir ctive and the amendments to the Directive are implemented into Dutch law.

4. It cannot be verified whether this holds true for all foreign operating companies. As of 2014, Uber France, for example, was reported to be owned directly by Uber U.S. This may, however, have changed. ("Uber's Tax-Avoidance Strategy Costs Government Millions. How's that for 'Sharing?'," 48 Hills, July 10, 2014.)

5. Id., with reference to records held by the Registrar of Companies in England and Wales in the case of the London-based operating company.

6. See "Pipsqueak Lyft Could Reach Profitability Before Giant Rival Uber," CNBC, January 12, 2017. Uber is allegedly the largest transportation network company in the U.S., claiming between 84% and 87% of the U.S. ride-hailing market ("Uber Loses at Least $1.2 Billion in First Half of 2016," Bloomberg Technology, August 25, 2016).

7. See, e.g., Rev. Rul. 76-322 1976-2 CB 487 (consignment sales through U.S. subsidiary); Private Letter Ruling (P.L.R.) 8715037 (U.S. marketing cooper- ative); P.L.R. 8131059 (U.S. marketing cooperative); P.L.R. 7923075 (U.S. subsidiary formed to provide certain services in connection with French parent corporation's and unrelated U.S. corporation's manufacturing operations).

8. Pursuant to the B.E.P.S. initiative, the O.E.C.D. Model Convention includes changes to the definition of commissionaires as well as limitations on ancillary activities. France appears to be pushing in the same direction, expanding the P.E. definition in a draft legislation issued in 2016.

9. Changes to the O.E.C.D. Model Convention, including the addition of an L.O.B. provision, were presented for public comment. The changes are subject to approval by the Fiscal Committee, which is expected by the end of this year. For details, see "O.E.C.D. Receives Public Comments on Proposed Changes to the Model Tax Convention," Insights 10 (2017).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.