Welcome to the December 2009 edition of Banking and Capital Markets Insight, which focuses on technical issues currently coming out of the banking, capital markets, securities and fund management arenas. I would normally undertake a review of the year at this stage, and a prediction of expectations for 2010. This year, however, the issues are so myriad and complex, that a compendium article will not do them justice or provide sufficient insights. Suffice it to say that the pace of change which we have seen in 2009 is not likely to diminish in 2010. Rather we will see the embedding of the regulatory and other changes which originated in 2009.

Our articles cover the following diverse areas:

- Alan Chaudhuri/James Polson on the need for systematically important banks to devise effective resolution and recovery plans, both under the FSA and international requirements, and the scope of the project planning involved;

- Kush Patel on the IASB exposure draft on impairment and the approach proposed which will smooth the effect of expected losses over the life of the asset, and will require greater disclosure of the effect of impairment losses;

- Stephen Woodhouse on potential approaches to the remuneration of employees, in the light of the 50% tax rate, including acceleration of remuneration, deferral of taxation, pension replacements and rewards attracting capital appreciation;

- Andy Whitton on the significant challenges for deposit takers to be able to give a single customer view to the Financial Services Compensation Scheme within 72 hours of failure and to target payouts within 7 days of an FSCS request; and

- Eric Wooding on the challenges facing the medium sized and smaller investment firms in meeting the FSA Liquidity Risk Management requirements, the systems and controls element of which came into place on 1 December 2009.

We look forward to your comments on the current edition and your suggestions for future articles. Best wishes for 2010.

Living Wills – Planning for bank recovery and resolution

There has been much recent public comment regarding dealing with firms which are 'too-big-to fail'. The FSA issued a Discussion Paper1 in October 2009 which set out initial proposals for the UK including:

- A case for applying additional capital surcharges on the most systemically important banks.

- Greater emphasis on the standalone sustainability of national subsidiaries within global groups.

- Continuing activities to reduce the interconnectedness of the wholesale markets.

- Reforms to trading book capital, differentiating between basic market making activities and riskier trading activities.

- The production of recovery and resolution plans ('RRPs' or 'Living Wills').

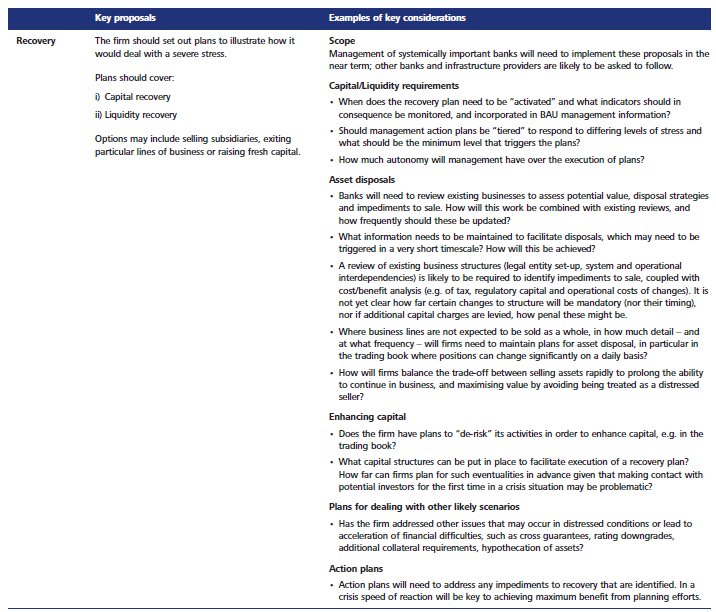

There are two main components to a Living Will. Firstly, plan to prolong the ability of the firm to continue in business and secondly, a plan to ensure an orderly workout can occur in the event the firm fails. Producing recovery and resolution plans will be a complex exercise, we believe the key activities are likely to include:

Recovery

- Determining when recovery plans should be 'activated'.

- Determining which businesses/assets could be sold and prioritisation of sale.

- Determining the impediments to any business/asset sales and how these could be reduced to facilitate future sales.

- Determining steps to 'de-risk' the business.

- Ensuring there are strong liquidity and capital recovery plans, including options to enhance capital in a crisis situation.

- Determining responses to other scenarios (e.g. rating downgrades, failure of large counterparties) likely to occur in a crisis situation.

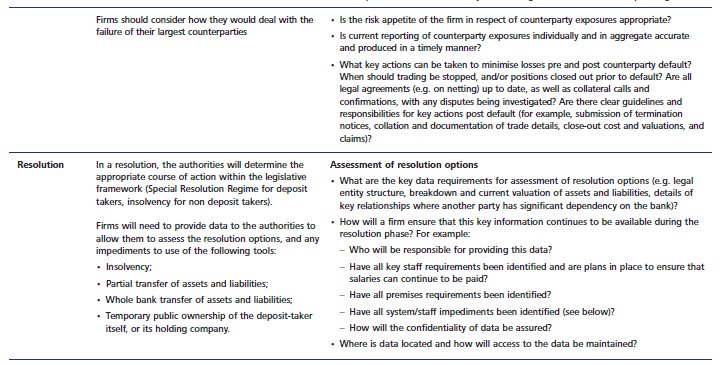

Resolution

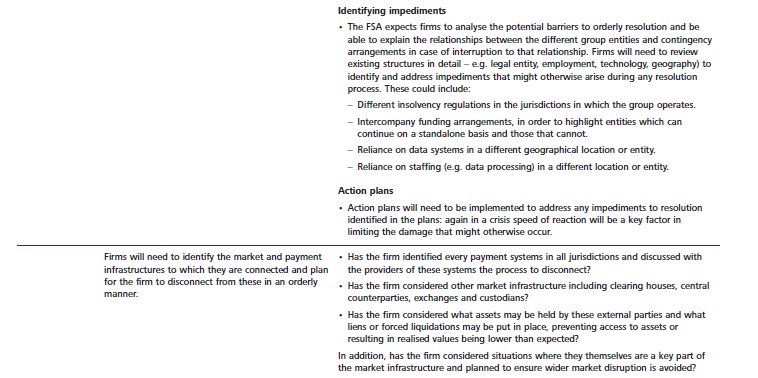

- Determining the key impediments to effective resolution (e.g. cross-border data reliance, staffing reliance, legal entity structure) and how these could be reduced.

- Determining detailed resolution plans for each business area including identification of data requirements and plans to ensure ongoing production of data.

- Determining appropriate actions to facilitate payment of compensation to depositors or return of client assets.

- Determining and mitigating the potential impact on market and payment infrastructures.

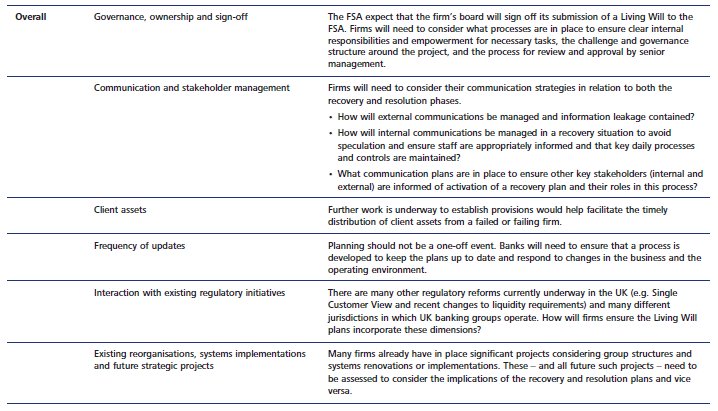

Plans will need to be discussed and agreed with the regulator, approved by the Board and kept up-to-date.

There are a number of structural issues that are likely to require assessment:

- Legal entity and operational structure. Systemically important banks are often global in nature with complex legal entity, operational and information technology structures and a large number of interdependencies. As a result, these may not be geared towards effective and efficient recovery and resolution.

- Deposit taking activities. A key question that has been raised by the FSA's proposals is whether any restructuring of complex integrated groups will require a clear separation (legally and operationally within the group) of the retail deposit-taking business from any business undertaking proprietary trading activities.

The FSA has stated that a small number of major UK banking groups will begin work to produce their recovery and resolution plans in 2009 with first drafts submitted by the end of Q1 2010. This will be followed by a period of review by the authorities, who will consider both the adequacy of the plans for each firm and the wider policy implications. Eventually, the FSA expects the requirement to be extended to all UK deposit takers (in proportion to their nature and scale) as well as other systemically important firms.

Subsequent to the release of the Discussion Paper, HM Treasury has introduced the Financial Services Bill to Parliament. Amongst the many proposals included in the Bill is one to amend the Financial Services and Markets Act ('FSMA') to impose a duty on the FSA to introduce rules to require firms to produce RRPs.

The FSA Discussion Paper addresses topics which are the subject of significant international debate and study in which the FSA is closely involved with work being undertaken by bodies such as the Financial Stability Board and the Basel Committee on Banking Supervision. In addition to the UK proposals there are currently proposals in relation to Living Wills contained in the recently published discussion draft of the "Restoring American Financial Stability Act of 2009" from the US Senate Committee on Banking, Housing and Urban Affairs2 and in recent Communications from the European Commission.3 The UK Financial Services Bill proposes to amend FSMA to require the FSA to have regard to international developments in making rules around RRPs.

In the UK, there are currently open questions as to the requirements for foreign owned institutions with significant UK presence and the operations of UK banking groups in other jurisdictions. Whilst the UK is further advanced in terms of making the production of Living Wills a reality, the requirement seems likely to extend to many significant financial institutions internationally in one form or another in the near future.

The tables opposite set out some of the key proposals relating to Living Wills in the Discussion Paper and some considerations for management as they prepare these plans.

The challenges of developing a Living Will are as much to do with setting up a cross-disciplinary project team to deal with the required changes to existing legal entity, governance, tax and IT infrastructure, as they are to do with the development of an effective recovery and resolution plan going forward. All that systematically important banks can realistically hope to achieve by the end of Q1 2010 is an outline plan and a template for how they will develop the detailed Living Will project over the next 12-18 months.

There is nonetheless a lot of significant thought that will need to go into the development of that initial planning in the next 3 months.

Impairment rules rewritten

In the current economic environment the accounting rules on recognising and measuring impairment on financial assets has come under close scrutiny. Both the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB) are in the process of rewriting the rules on accounting for financial instruments including when an impairment loss on a financial asset is recognised and how it is measured. The end goal is a common set of rules for use on both sides of the Atlantic. However, the IASB is working on an accelerated basis and has already issued a final standard on classification and measurement of financial assets (IFRS 9: Financial Instruments was issued on 12 November 2009) which sets out which assets are assessed for impairment. In addition, it issued an exposure draft (ED), Amortised Cost and Impairment, on 5 November 2009 proposing a replacement to IAS 39's incurred loss model with an expected loss approach. The IASB's intention has been to address some of the key weaknesses of the current rules.

The rules on impairment are interwoven with the rules on classification and measurement. IAS 39 has been criticised for the many different classification categories and the resulting different approaches to measuring impairment. For example, debt instruments classified as either available-for-sale (AFS), held-to-maturity (HTM) or loan and receivable (L&R), and equity investments classified as AFS and those held at cost must all be assessed for impairment. Furthermore, the measurement of impairment depends on the classification. For AFS assets impairment is based on fair values, for HTM and L&R assets it is based on discounting expected cash flows using historical discount rates, and for equities measured at cost impairment is based on assessing discounted cash flows using current discount rates. Then to top it off the rules on reversing impairments differ too with reversals required for debt instruments but prohibited for equity investments.

IFRS 9 cuts down this complexity to a single impairment requirement only for debt instruments measured at amortised cost. An impairment assessment is not required for investment in equity securities. IFRS 9 limits the extent of assessing for impairment but does not, to date, change the way impairment is measured. The current 'incurred loss' approach to recognising impairment has been criticised for prohibiting recognition of expected losses, however likely, unless there has been a credit trigger event, such as default. This approach has the effect of deferring the recognition of expected losses leading to a 'cliff effect' when loans start to go bad. The approach has been argued as being 'pro-cyclical'. If many loans go bad together, like in the recession, the cliff drop can be significant.

Some commentators, particular bank regulators, have suggested that impairment provisioning should instead be 'anti-cyclical'. Two often cited 'anti-cyclical' provisioning techniques are through-the-cycle provisioning and dynamic provisioning. Through-thecycle provisioning would see provisions being built up from income on loans in the good times to be released against future loan losses in the bad times, although not necessarily on the same loans. One feature of dynamic provisioning is that a provision can be set aside for loans when they are written leading to a loss on day one.

Expected loss model

The IASB has not opted for either of these two methods in its ED as neither is considered to neutrally portray the economic characteristics of the recognised loans. Instead the IASB's approach is one that smoothes the effect of expected losses over the expected life of a loan. For example a five year loan written with an interest rate of 7% may have an expected return of 5% after taking into account expected losses. Under the expected loss model the effective interest rate (EIR) applied to the amortised cost carrying value of the loan would be 5% and a provision would begin to build up by setting aside the difference between the contractual interest and the EIR. This provision would be used to absorb expected losses when they materialise and are written off. This approach does not recognise a loss on initial recognition of a loan nor does it retain provisions from old loans to be set off against losses on future loans.

Those who think this method eliminates all volatility from recognising impairment losses would be mistaken. Only where estimates of initial expected losses are accurate is the recognition of the effective return smooth over the life of a loan. If there are changes in the expectation of losses over the life of the loan then this will result in an immediate gain or loss being recognised in profit or loss. At each reporting date an entity will no longer need to consider whether there is a credit trigger like under IAS 39, but will instead be required to continuously reassess its expectations of future cash flows.

Two IASB board members voted against publication of the ED partly because they believe the approach will not provide sufficient benefit in improving financial information to justify the costs. Concerns were raised that the approach would increase the potential for earnings management because in their view the loss expectations of management cannot be audited. To address some of these concerns the ED proposes additional presentation and disclosure requirements.

Disclosures

Interest income is to be presented both before and after expected credit losses which will give prominence to the margin of contractual income that the borrower is charged to recover the lender's expectations of future credit losses. Separate presentation is also required for gains and losses arising from changes in the expectation of credit losses which will give insight into the direction and timing of management's re-estimations. Disclosure explaining changes in estimates are also required.

The ED proposes all provisions to be held in a separate allowance account (which is set off against the loan balance) instead of reducing the carrying value of a loan directly. Entities would be required to disclose the size of their allowance accounts which could vary in size depending on their write-off policy hence a reconciliation of its use is also required.

An analysis of the year of origination and maturity of loan assets held at amortised cost is also proposed. These disclosures could be quite extensive for entities involved in long term lending arrangements such as residential mortgages. Stress testing information is also required where this is prepared for internal risk management.

Implementation

The objective of the ED is simple. Putting it into practice will not be. For many entities, particularly lending entities such as banks, the new approach would require significant demands on information systems. The IASB has acknowledged this by allowing some practical expedients in applying the proposed model. The IASB is also in the process of establishing an expert advisory panel to consider further guidance and practical expedients that may be needed. Although the standard, if adopted, would not be effective until at least 2013, the decision whether to proceed with the proposals is expected to be in the second half of 2010 – this is when the real work will start.

Tax and the City – Preserving value and reducing cost

While the subject of remuneration and reward continues to take up column inches (or perhaps feet) in the press, relatively little attention has focussed on the tax treatment or bonuses and other rewards and the opportunities to reduce cost which this can give rise to.

Background

There are some key tax facts influencing the design of remuneration structures.

- 50% tax will apply to income in excess of £150,000 from 6 April 2010.

- Combined with personal NIC rates, this will result in an overall effective rate of tax and NICs for high earners of 51.5% from 6 April 2011.

- It is expected that this rate will survive any change of Government.

- Pension funding in excess of £30,000 (or in some cases, £20,000) is now subject to an effective tax charge of 20% (due to increase to 30% from 6 April 2010).

- Capital gains are chargeable at the relatively low rate of 18% with no national insurance contributions.

These features drive the planning mainly being considered for higher level earnings.

Acceleration of reward

As a starting point, where it is possible for remuneration to be accelerated so that it is paid and taxed in the current tax year, that offers an immediate 10% tax saving compared with making payments in the following year. Acceleration of reward should therefore be considered and where this is possible without a need for claw-back provisions in respect of the amounts being accelerated, should achieve the desired tax saving without significant complexity.

Where there is a commercial imperative for claw back protection to be included, however, more complexity and risk results as HMRC may seek to attribute the payment to the subsequent tax year. Further, it needs to be recognised that where amounts are paid early and are subject to tax, that tax has to be paid even where the award is subsequently forfeited due to a change of employment.

While acceleration should be one of the first areas to be considered, its application may not be straightforward and may result in the need for the use of equity or other securities to secure the intended tax treatment while preserving the overall commercial integrity of the awards.

Deferral

An alternative approach, more in keeping with the expectations for the commercial structuring of reward, would be to seek to defer the tax charge. This would potentially allow the amounts deferred to be invested on a gross basis to improve effective pre-tax returns and, if tax rates reduce in future, may result in the eventual rate of tax on payment also being reduced.

There are various approaches which allow deferral on a basis consistent with the intended effect of the tax legislation and the expectations of City investors and regulators. For instance, the tax regime provides specific relief to defer the tax charge in relation to options over securities (and not just employer shares) until they are exercised. An appropriate use of option structures is therefore one way to allow deferral consistently with the substance and intent of the tax legislation.

Pension replacements

The provision of pension replacements is linked to deferral. For most people with income of £150,000 per tax year, receiving substantial pension funding into a qualifying pension scheme is unlikely to be attractive. Replacement approaches need to be considered.

There are various approaches:

Paying cash – this is the simplest approach and one which is favoured by many listed companies, but with no tax benefits (other than ensuring the tax charges on qualifying pension funding do not apply).

Unfunded pension – aside from any tax issues, this creates a long term unfunded liability for the Company which is difficult to quantify and therefore to account for without volatility exposure.

Funded plans – funded, non-qualifying plans are specifically provided for by the tax legislation. The main tax points with the expected tax treatment are:

- No income tax or national insurance contributions on funding the plan.

- No corporate tax relief on funding the plan.

- Tax deferral on fund returns where the plan is outside the UK and invested for capital returns (or non-UK source income).

- Income tax on the provision of retirement benefits (but with possible protection where the individual is not resident on the payment of the benefits depending on their form and timing).

- NIC protection on the payment of pension income from the fund (but potential NICs on lump sums).

- Corporate tax relief for the funding of the plan but only when benefits are provided.

It will be seen that these plans offer long term deferral and tax protection at the cost of a matching deferral of corporate tax relief. It is expected that the incidence of these plans will proliferate given the current tax regime given the combination of high personal tax rates, relatively low corporate tax rates and the restrictions on reliefs for qualifying pensions.

Family benefit trusts – although specifically not a pension scheme, a family benefit trust offers the potential for more flexible long term wealth creation. An FBT operates through a discretionary employee benefit trust. Contributions are made on a discretionary basis and allocated to sub-funds for the families of particular individuals. The assets in the sub-funds are available to provide benefits to the family of the employee concerned either during or after employment or to be invested.

The intended tax treatment is similar to a non-qualifying pension plan but with additional flexibility both on the timing for the provision of benefits (which can be during or after employment and without limitations by reference to age) and with scope for additional advantages in terms primarily of tax protected benefits.

Family benefit trusts are currently subject to greater review and scrutiny by HMRC which should be recognised when they are established in order to ensure that the risks of challenge are minimised.

Capital appreciation

The final area we have considered for this article is the delivery of reward in a form which attracts capital gains tax with the benefit of an 18% tax rate with no NICs (although equally no corporate tax relief except where this is achieved through an HMRC qualifying or approved plan).

There is a myriad of different structures which allow for a capital gains tax rather than income tax treatment, but they fall into two main categories, although in both cases there has to be real capital growth for capital gains tax to apply.

Approved/qualifying plans – with approved or qualifying plans, the capital gains tax treatment is available at the same time as the employer being able to obtain corporate tax relief for the cost of delivering the underlying equity, subject to satisfying the detailed requirements of the legislation. The cost of this is that the plan must satisfy the detailed rules to obtain the approved/qualifying status and in particular the limitations placed on plan awards (such as the £30,000 initial value of equity subject to approved discretionary options). While this will limit the value which can be delivered, there is a role for these plans as part of a wider approach to delivering optimum benefits through the overall remuneration mix.

Growth interests – the second area is the delivery of a growth interest. This may be a separate class or share or (more likely for a listed company) a joint interest in an ordinary share. The interest will participate in future value growth above a threshold. Income tax and NICs are payable when the interest is acquired but the intention is that this would be on a low or nil value (where the employee pays market value for that interest) with capital gains rather than income tax/NICs payable on the future value appreciation.

Aside from the tax benefits, these plans offer scope to align remuneration value with the interests of shareholders and regulators as they require long term capital growth to deliver the tax value.

Overview

With the extensive coverage of remuneration levels within the Financial Services market over the last twelve months, there has been less focus on the scope to reduce costs through appropriate tax structuring. This does not require plans which are overly aggressive or which conflict with the intended effect of the tax legislation but rather an appreciation of the opportunities offered by a combination of existing high marginal tax rates. Significant differences between income and capital gains tax rates and commercial pressure for substantial remuneration packages to reflect long term capital growth.

This article has highlighted some of the approaches which can be followed and which can be used as a base for a review and development of existing remuneration structures.

A guide to faster payout What the new FSA rules mean for the Financial Services industry

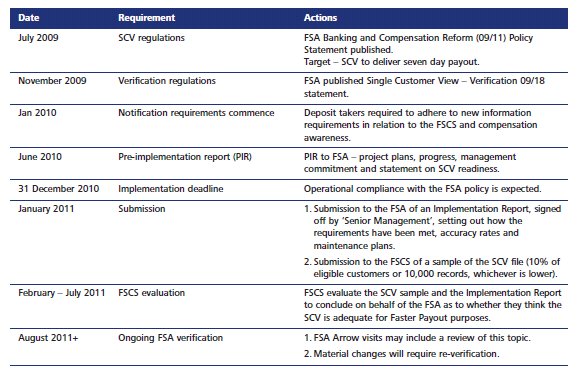

In July 2009, following a formal consultation process, the FSA published new regulatory rules requiring authorised deposit takers to develop a 'single customer view' (SCV) showing each customer's aggregate positive balances across all of their accounts at any given point in time. The requirements go beyond producing an SCV – the FSA also requires deposit takers to apply a specific set of 'Faster Payout Rules' to help ensure compensation can be paid within a target of seven days should they go into default. If a deposit taker fails, it will have 72 hours to provide the Financial Services Compensation Scheme (FSCS) with an SCV file with the Faster Payout Rules applied to the data set. While a European Directive will require payment within 20 days, the UK authorities are targeting compensation payout within seven days of receiving a request from the FSCS. The implementation deadline is 31 December 2010.

The demands this places on the financial industry are significant. Technology changes are required, and the associated process and controls developments, will affect many parts of an organisation. One question currently being considered is whether this regulatory requirement can be used to drive strategic changes, delivering competitive advantage through better customer services, improved cost management and ultimately increased revenue?

Consumer impact

This new regulatory requirement is designed to promote consumer confidence by ensuring that if a deposit taker fails, savers will be able to get up to £50,000 compensation within seven days. Additionally, consumers will receive more comprehensive information (notifications) from their banks or building societies explaining how the FSCS compensation process works and how their deposits are protected.

Deposit taker impact

An SCV file needs producing with the relevant Faster Payout Rules applied by 31 December 2010. This requires a 'reliable and consistent' view of aggregate deposits for each eligible customer per 'authorised deposit taker'. While some deposit takers' existing SCV implementations will provide a good starting point, new requirements like calculating term accounts at default, capturing in-flight transactions, allocating unique customer record numbers and building in flexibility to deal with changes to variables (e.g. compensation limits and eligibility criteria) will all present very new challenges.

Market innovation

Some deposit takers will tightly follow the above steps to achieve regulatory compliance. Others are being more innovative and aggressive in meeting their regulatory obligations and are considering how to develop and maintain a real time SCV to support the well rehearsed operational, risk and compliance benefits:

- Gain real-time access to integrated customer information.

- Enhance data accuracy and reduce IT costs.

- Open new partnership channels, expand efficiencies and increase revenue levels.

Another consideration is how they can cross-sell FSCS protection within their own groups to enhance customer service and promote confidence in their institutions. More radical changes include adapting their institutional structures and account opening procedures.

At a product level, the new regulatory requirements will potentially change the structure and types of products deposit takers offer, with some types of 'off set' mortgages no longer being covered by the compensation requirements.

Beyond the regulatory imperative, deposit takers also need to be alert to the reputational risk of being perceived as non-compliant. Particularly with formal notification detailing the coverage provided by the FSCS being sent to customers every six months, consumers and the press will become increasingly aware that if a bank or building society fails, people can expect to receive their money back in 7 days. No deposit taker will want to be seen as unable to meet this target.

This is an excerpt from our recently released "Guide to faster payout". To read the full article, please visit www.deloitte.co.uk/fasterpayout or contact Andy Whitton for more information on 020 7303 7215.

Glossary

FP – Faster Payout – Policy framework designed to ensure consumers are compensated within 7 days.

SCV – Single Customer View – Consolidated view of all eligible customer accounts.

VFPR – Valuation Faster Payout Rules – Valuation rules used to produce the SCV file.

EFPR – Eligibility Faster Payout Rules – Eligibility rules governing which consumers should be included in the SCV file.

PiR – Pre-implementation Report – June progress report to the FSA from every deposit taker.

FSCS – Financial Services Compensation Scheme – The Compensation scheme that will receive the SCV file and pay consumers.

FSA's new liquidity risk regime: Q & A for investment firms

This article seeks to provide basic information on FSA's new liquidity regime for the management of investment firms who have not themselves studied the new regime in depth.

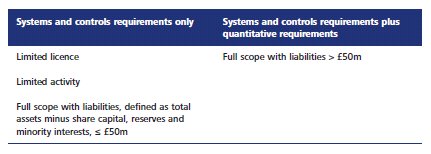

Which parts of the regime apply to different types of BIPRU investment firm? FSA's new liquidity rules essentially divide BIPRU investment firms into two main categories: those which are subject to liquidity systems and controls requirements only and those which are subject to both systems and controls requirements and quantitative requirements called 'individual liquidity adequacy standards' (ILAS). The table below summarises the types of BIPRU investment firm which fall into each category:

When do the systems and controls requirements come into effect, what are they and what should we do about them?

The systems and controls requirements are already in effect. They came into effect on 1 December 2009. Key elements include: (1) requirements for the board to establish a liquidity risk tolerance for the firm, approve policies and procedures for managing liquidity risk and conduct an annual review of these items, and (2) detailed guidance on what the liquidity risk management system should contain, liquidity stress testing (which the board must review at least annually for continuing relevance) and contingency funding plans.

As they are more detailed than the previous liquidity systems and controls requirements which were set out in SYSC 11, firms that have not already done so should compare the new requirements to their current procedures, identify any gaps and develop a plan to remedy them as early as practicable.

When do the quantitative requirements come into effect, what are they and what should we do about them?

Quantitative requirements

The quantitative requirements come into effect on 1 November 2010. Very few investment firms subject to the quantitative requirements are expected to qualify for a 'simplified ILAS' waiver. Therefore most will be 'standard ILAS' firms and as such will be subject to the following quantitative requirements:

- to submit to FSA periodically seven liquidity returns;

- to conduct an 'individual liquidity adequacy assessment' (ILAA) at least annually; and

- to comply with 'individual liquidity guidance' (ILG) set by the FSA, which will normally be based on FSA's review of the firm's ILAA.

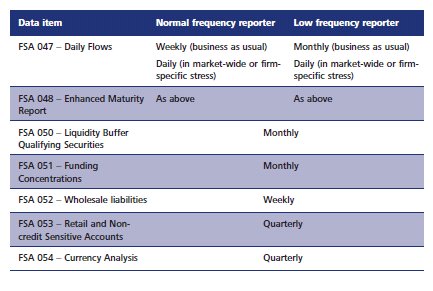

Liquidity returns

The seven required liquidity returns ('Data items' in FSA parlance) and the frequency with which they are required are set out in the table below. To qualify as a 'low frequency' reporter a firm must have total assets below £1bn.

As the returns are designed for deposit takers and major securities dealers, smaller investment firms which are subject to the requirements may need to ask FSA to clarify what is required and therefore should start their analysis of how the returns apply to their business and their discussions with software providers at an early stage.

If a firm chooses to apply for an intra-group liquidity modification (see below), it needs to take into account the implications for its reporting. In particular, there will be a new level (the 'designated liquidity group') at which at least some of the above returns are required but in some cases there may be a reduced burden at the solo level i.e. the level of the individual regulated entity.

The Individual Liquidity Adequacy Assessment (ILAA)

An investment firm that is a 'standard ILAS' firm is required to have carried out and documented its ILAA by 1 November 2010. The ILAA contains the firm's own calculation of the liquidity it needs to survive without reliance on support from the public authorities three stresses specified by the FSA, namely a firmspecific stress, a three month market-wide stress and a combination of the two. Unless the firm has obtained an intra-group modification, it must prepare the ILAA at the solo level of the individual regulated firm.

The ILAA must also contain the firm's own assessment of its compliance with the systems and controls requirements.

Preparing the ILAA is clearly a task that merits the careful attention of senior management and the board. In the first place, the ILAA is a crucial input into the process, called the Supervisory Liquidity Review Process (SLRP), by which FSA determines its Individual Liquidity Guidance (ILG) for a firm. A poor quality ILAA could therefore result in a firm having to maintain a bigger buffer of government securities than would otherwise be the case. Secondly, FSA's requirements for conducting an ILAA are substantial, demanding for example, that in carrying out each stress test the impact on 10 sources of risk must be assessed.

Individual Liquidity Guidance (ILG)

Following its review of a firm's ILAA FSA will issue a firm with ILG that covers the size of a firm's liquid assets buffer and the firm's funding profile.

The buffer can only contain government securities issued by specified governments, certain sight deposits with central banks of the same countries and securities issued by specified multilateral development banks. The governments and central banks must meet rating requirements intended to ensure they are high quality. Cash in a bank account cannot be part of the required buffer.

While the switch on date for the quantitative requirements is 1 November 2010, clearly FSA will not have performed a review of every ILAS BIPRU investment firm's ILAA by that date. Hence firms may wish to contact their FSA supervisor in order to clarify what buffer requirements, if any, will apply to them between 1 November 2010 and the date ILG based on a review of the firm's ILAA is issued.

FSA's policy is to introduce ILG progressively, that is to say, initial low-level liquidity guidance will be provided to firms as they migrate onto the new regime, to be followed by 'a gradual raising of liquidity standards over time, paced according to wider macro-economic developments.' Thus the transition to the full buffer requirement may take 'some years'.

FSA plans to announce in the first quarter of 2010 'its programme for making and applying judgement about the ultimate calibration of our quantitative requirements, and the appropriate trajectory, set flexibly to achieve it through time.'

In short, the order of magnitude of the buffers that will be required of investment firms and precisely how they will be phased in is not yet clear.

The intra-group liquidity modification

Unless a firm obtains an intra-group liquidity modification from FSA, it must comply with the new liquidity regime on a stand-alone basis i.e. without any reliance on its parent or other members of the group to which it belongs. This means that the new liquidity risk systems and controls requirements, the full set of returns and ILG will apply at the level of the individual ILAS firm, not at group level (there are however limited additional reporting requirements at group level).

An intra-group liquidity modification can result in the principle of liquidity self-sufficiency for UK solo entities being relaxed. In the case of a UK group or sub-group, the key effect of such a modification will be that ILG is set at the level of the UK 'designated liquidity group' (DLG) [i.e. the firm plus the UK group entities on which the firm is permitted to rely for liquidity purposes] and not at the level of the individual firm, although the individual firm will still be required to have adequate liquidity to wind down its business in an orderly way. In addition the full set of returns will be required at UK DLG level although some returns continue to be required, albeit less frequently, at individual ILAS firm level. Finally, a firm with an intra-group modification may rely on other parts of the group to meet systems and controls requirements, subject to the group having regard to the liquidity position of the individual ILAS firm.

In the case of firms with a foreign parent, FSA says that it will consider an intra-group liquidity modification to rely on a foreign parent but that will 'only result in a partial switch off of the self sufficiency requirement, such that ... the UK entity or collection of UK entities (or ILAS group) will have enough liquidity to enable it to wind down in an orderly manner.' FSA will inform such a firm how much of its liquidity can be held elsewhere in the group.

In the case of firms wishing to rely on a foreign parent, FSA will grant an intra-group liquidity modification only if it is satisfied that the parent is subject to liquidity regulation broadly equivalent to FSA's new regime and it has reached agreement on various points with the overseas regulator and the parent. In particular, the parent will be required to make available to the FSA information on the group's liquidity.

Investment firms which wish to apply for an intra-group liquidity modification must do so by 1 June 2010. The FSA has until 1 October to determine the application, only one month before the new quantitative requirements come into effect. Firms who are considering applying for such a modification may therefore wish to discuss this with their supervisor at an early stage.

Footnotes

1 DP 09/4 Turner Review Conference Discussion Paper, A regulatory response to the global banking crisis: systemically important banks and assessing cumulative impact ("Discussion Paper"). http://www.fsa.gov.uk/pubs/discussion/dp09_04.pdf

2 Discussion draft, "Restoring American Financial Stability Act of 2009", published November 2009

3 The Commission communication (COM(2009) 561/4), An EU Framework for Cross- Border Crisis Management in the Banking Sector

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.