Foreword

By Carl D Hughes

UK Head – Energy, Infrastructure & Utilities

In recent years, the UK has had no difficulty generating enough electricity to meet increasing demand, and little problem in balancing the priorities of energy security, emissions reduction and the maintenance of efficient markets. Primarily, this is because the UK has been able to rely on abundant indigenous fossil fuels (particularly North Sea gas, but also coal) supported by nuclear power.

During this period, businesses have focused on exploiting North Sea reserves and achieving greater efficiencies from existing power generation assets. The reliance on gas and the systematic replacement of old polluting coal-fired plant with new, lower emissions gas-fired capacity over time has meant that greenhouse gases from power generation have been reduced.

Recently, however, a number of factors have arisen which will make it much harder for the UK to maintain the status quo and raise real questions about the adequacy of current UK energy policy. These include:

- Dwindling domestic gas reserves which, given the UK’s limited gas storage capacity, has resulted in increased reliance on imported gas;

- Planned retirement of our existing nuclear capacity;

- Downgrading expectations for the potential contribution of renewables to our generation mix;

- Elevated environmental concerns; and

- Volatility of the global energy markets.

Together, these factors point towards an emerging energy gap and an urgency around emissions reduction, necessitating a re-think of our requirements for electricity generation over the next fifteen years and beyond.

Given the differing agendas of key stakeholders in the energy policy debate, and the need to strike the right balance between ensuring security of supply, reducing emissions and optimising affordability, finding an acceptable solution to this challenge will be both technically and politically demanding. Compromise, which is never popular, will be essential if the Government is to succeed.

In this paper, we provide an insight into the choices that the UK faces by presenting a number of different scenarios for UK power generation in 2020 and beyond, analysed from the perspective of the key stakeholder groups.

We look across the whole of the energy and fuel supply value chains to take an holistic view of the challenges ahead. While we do not purport to have found ‘the solution’, we believe we have created an agenda for discussion that reflects our conclusion that the UK is unlikely to achieve its overall objectives if decisions about the future of power generation are left entirely to the private sector. It is, we believe, up to Government to set policy and facilitate development of the necessary market levers that will incentivise investment in the most appropriate infrastructure and technology.

This paper is part of Deloitte’s forward looking series on the future of UK energy. We hope you find the contents make an important contribution to the energy policy debate and welcome your comments.

Executive summary

In hindsight, we hope 2006 is remembered as a watershed in UK energy policy. After 20 years of market-driven policies aimed at delivering competition and ‘economic’ prices, HM Government is reviewing the framework within which energy policy is delivered and considering to what extent it needs changing.

This paper indicates that if we are to succeed with the collective objective of ‘securing clean, affordable energy for the long-term’, there is a clear and immediate need for change. Our conclusions in this regard are based upon a top-down qualitative and quantitative scenario and risk analysis.

Energy policy is likely to be one of the most complex and challenging issues of our time, with a delicate balance required between many competing interests, including commercial and economic priorities and the potential social impact on future generations. The key considerations are:

- Urgent need to address the emerging energy gap The planned retirement and closure of existing nuclear and coal power stations, combined with predicted demand growth, will result in a fundamental requirement to build new electricity generating capacity to fill the emerging energy gap. By 2020, over 50 GW of new or refurbished generation capacity will be required, which represents circa two-thirds of current capacity – equivalent to either 55 new CCGTs1, 30 new nuclear power stations, 95,000 on-shore – or 40,000 offshore – wind turbines. Whilst a contribution to narrowing this gap can undoubtedly be made by intensifying efforts around demand management, the majority of the UK’s response will necessarily be through managing supply with the addition of new generation capacity.

- ‘Securing clean, affordable energy for the long-term’ – a fools paradise? The Energy Strategy Review needs to set the future direction for the UK’s power generation policy. HM Government should take the lead in specifying which fiscal and other policy levers will be deployed, and by how much, to signal to the market the framework within which technology choices are to be made. A key to success will be clear and definitive agreement on objectives – whilst these are well documented, there is little consensus as to what they actually mean and where the priorities should lie. The inherent tensions between the objectives of energy security, emissions reduction and market efficiency mean compromise will be inevitable. Failure to understand and align the interests and areas of conflict will pose a significant risk to the successful delivery of the UK’s future energy requirements.

- Doing nothing is not an option The UK is currently set to pursue further expansion of its CCGT fleet in order to fill the emerging energy gap, with uncertainties regarding the commerciality of alternatives. Indeed, in order to meet the predicted 2010 capacity deficit, there are already plans in place within the private sector to develop some 2,000 to 5,000 MW of new CCGT facilities. Our analysis shows that, in the absence of immediate action to reshape energy policy, potentially half of the energy deficit by 2020 will be accounted for by new CCGT plant. This will give rise to possible carbon emissions from the UK power generation sector of 120 – 140 million tCO2 in 2020, against a likely target for the power sector of circa 105 million tCO2. Such high reliance on CCGT as the dominant plant will fundamentally compromise the UK’s ability to ensure security of supply, meet emission reduction targets and manage power price volatility.

- Diversification should be the holy grail… and that includes nuclear Our analysis shows that it is unlikely that sufficient power generation capacity can be secured, and emissions targets met, without employing a diverse range of power generation technologies. Investment in a combination of fuel and technology types will alleviate the security of supply issues associated with over reliance on a single imported fuel, whilst drawing on a number of low carbon generation technologies will facilitate meeting emissions reduction targets for the power sector.

In our view, a substantial element of nuclear new build will be required for the next generation. Other low carbon technologies will not be sufficiently developed for the UK to rely on in order to secure adequate power supplies and to achieve meaningful emissions reductions by 2020. Facilitating nuclear new-build will involve taking decisions very soon on key issues such as setting the long term price for carbon, waste disposal, funding decommissioning liabilities and addressing planning and health & safety constraints.

The cost of delivering a truly diversified, low carbon generation mix will be significant, at over £50 billion, almost twice that of placing continued reliance on CCGT. As a country, we need to decide if this is a price worth paying.

- Full potential for renewables and CCS is in the future Placing a substantial level of reliance in the short-term on emerging renewables and CCS2 technologies to secure our energy future (in the absence of nuclear new-build) would represent a high risk strategy. Many of these technologies are unproven at the scale required to fill a significant portion of the energy gap, whilst the more advanced wind technologies face the challenge of intermittency and connectivity, with consequential low load factors in comparison with the scale of installed capacity.

- Certainty needed to stimulate investment In increasingly competitive, global markets for capital and resources, HM Government will need to give clear, long-term signals on the form of market and fiscal frameworks for the next 15 to 20 years, with consensus support from the Opposition. Given the stated objectives of current energy policy, we believe that the key signal requiring immediate reform is the range of incentives around emissions reduction. This should include streamlining mechanisms such as the Renewables Obligation Certificate, Climate Change Levy and Levy Exemption Certificate and should embrace a long term carbon price signal that can operate as part of, or complimentary to, the European Union Emissions Trading Scheme, beyond 2012.

- Call to action The Energy Strategy Review is an important step in challenging existing policy. It should stimulate informed debate and provide insight into the primary objectives of key stakeholders. HM Government will need to determine the overarching priorities and build consensus on the best way of achieving them. This will undoubtedly require choices around investment in a number of new technologies, each with their own profile of risks and benefits, as well as practical steps to ease planning restrictions and connectivity issues. Our analysis highlights the need for a detailed quantitative and qualitative analysis of the outputs and risks associated with each option, such that undue reliance is not placed on specific, unproven technologies. This analysis will also allow for the development of a framework within which the appropriate apportionment of risks (particularly long-lived risks like nuclear decommissioning) between the public and private sectors can be facilitated. Overall, HM Government must be willing to make some difficult decisions around both the supply of and demand for power, and set a clear path for the next generation. The importance of the energy debate should not be underestimated – future policy will directly affect the welfare and security of our country, our people and our economy. This is a time for clarity of thought and analysis. Let the debate begin – but not take too long to reach a conclusion.

In order to unlock their potential, a significant amount of effort and investment will be needed to overcome the existing technical, commercial and other barriers facing their widespread adoption. In arguing that renewables and CCS are the future, it is notable that CCS particularly could bring long term competitive advantage to the UK through the interaction of the power sector with the North Sea Continental Shelf (carbon ‘sinks’ and enhanced oil recovery) and through the ability to continue to access significant, indigenous coal reserves.

Developing an energy policy which is sufficiently flexible to allow inclusion of these key, low carbon technologies will be critical to optimising the power generation mix going forward. In the meantime, managing the general public’s low level of awareness as to the realistic level of contribution from renewables to the generation mix3, and the consequential views on nuclear, will be an important matter to address.

"A substantial element of nuclear new build will be required for the next generation as other low carbon technologies will not be sufficiently developed for the UK to rely on them alone in order to secure adequate power supplies and to achieve meaningful emissions reductions by 2020."

Where is the UK now?

In recent years, the UK’s ability to utilise indigenous fossil fuels (coal and North Sea gas) in combination with nuclear power for electricity generation, has resulted in a sufficient level of supply to meet demand. The UK’s current position on the mix of electricity generated is approximately: coal 37%, gas 35%, nuclear 21% and renewables (predominantly hydro-electric and on-shore wind) 4%, with the remaining 3% being provided by oil, other fuels and electricity imports.

Recently, however, a number of factors have created uncertainty over how the UK will meet future electricity demand including:

- Declining gas reserves – The UK’s gas reserves are in decline to the extent that the UK has become a net importer of gas (through pipelines and LNG terminals) sooner than expected. Further, the UK has limited domestic gas storage capacity;

- Reducing civil nuclear capacity – The decommissioning of aged civil nuclear capacity is expected to lead to the majority of the existing facilities being retired by 2020 (assuming no additional life extensions);

- Renewables growth – Despite investment in renewable sources of energy, including wind and marine technologies, renewables currently constitute just 4% of the UK’s total generation mix. This is acknowledged to be short of the growth rates required to meet HM Government’s stated targets for 2010 and 2020 of 10% and 20% respectively;

- Climate change – Environmental concerns associated with greenhouse gas emissions have been elevated up the political agenda. Many existing coal-fired power stations may become uneconomic due to their emissions profile;

- Reversing emissions reductions – The emission reduction benefits achieved through the replacement of coal with gas-fired generation will be progressively lost if retiring nuclear plant is replaced with carbon emitting gas fired plant; and

- Rising and volatile gas prices – The increasing reliance on gas and the intrinsic link between the price of oil and gas have exposed the UK to significant price volatility. These issues influenced HM Government to announce an energy policy review at the end of 2005.

Although the options available for electricity generation appear finite, key stakeholders in the energy policy debate maintain conflicting views on a number of contentious issues such as the potential role for renewable energy in filling the energy gap, and the possibility of civil nuclear new build. Developing an appropriate degree of consensus on the UK’s future energy mix is thus likely to prove challenging.

How has this position come about?

The UK’s current power generation portfolio has been built up over a long period of time in response to specific economic and policy drivers. These trends have resulted in a legacy power generation mix which will not respond to the requirements of the energy policy objectives of today. Many events and drivers have brought the UK to the current situation, including:

- The oil crises and miners’ strikes of the 1970s – HM Government developed an objective of diversifying the sources of fuel used in power generation away from oil and coal;

- Discovery of economic gas reserves in the North Sea – The development of the North Sea gas fields provided a low price and reliable supply of gas for the UK market;

- Changes in EU regulation to repeal restrictions on use of gas by the power sector – Provided impetus to increase the use of North Sea gas through the building of significant capacity in Combined Cycle Gas Turbine (‘CCGT’) facilities;

- Large scale privatisation of the UK power industry – Privatisation provided the commercial driver to improve efficiency of power generation, transmission and distribution assets, and to replace inefficient assets;

- Global ‘dash for gas’ – The inherent efficiency and flexibility of CCGT provided the economic and technological incentive to initiate large scale gas-fired capacity building;

- Changes to the electricity pricing mechanism and expenditure control – The decision to move away from a ‘pooling’ approach to pricing on a more competitive basis under New Energy Trading Arrangements (NETA) for England and Wales resulted in falling electricity prices, and made certain types of generation, operators and plant uneconomic; and

- Corporate failures – Market changes resulted in domestic power prices falling to historically low levels which pushed a number of operators and plant into administration.

Taken together these drivers caused fundamental changes to the power generation portfolio of the UK over the last three decades providing a number of inherent benefits during the 1990’s including:

- Relatively low capital investment and operating costs, coupled with focused investments on transmission and distribution networks, providing reliable generation capacity;

- Lower investment and generation costs of gas-fired plant meant that consumer electricity prices overall fell in real terms;

- Energy security was not perceived as an issue as the majority of fuel could be sourced locally; and

- Greenhouse gas emissions were steadily reduced as aged and more polluting coal-fired power plant was systematically replaced with lower emission-rated gas-fired plant.

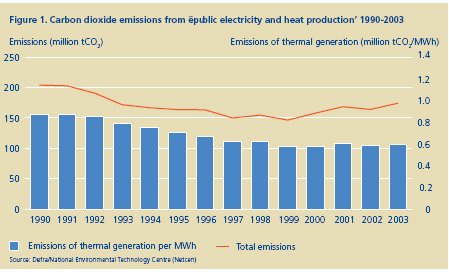

The impact of these trends is illustrated in Figure 1, which shows that carbon dioxide emissions from the power generation sector fell during the 1990’s by 30%, thus delivering a major contribution to the overall UK reduction in greenhouse gasses.

Where is the UK now?

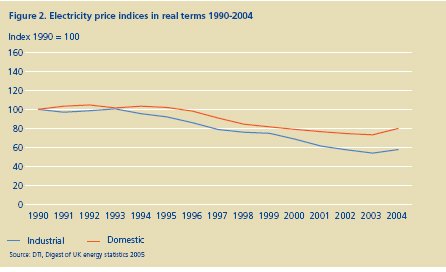

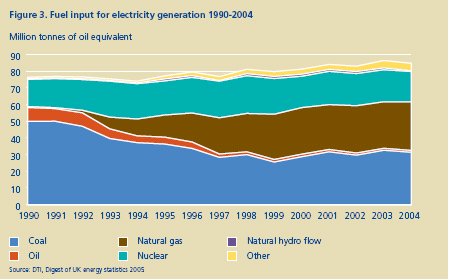

Figure 2 shows how electricity prices to consumers fell during the same period and Figure 3 illustrates how fuel diversity increased.

All good things come to an end

However, the same figures also show how the positive aspects of certain trends have begun to reverse in recent years. The historic decreases in carbon dioxide emissions have slowed and in certain cases have even showed signs of increasing as:

- The rate of entry of new CCGT capacity has slowed as a consequence of increasing gas prices and low spark spreads;

- Gas prices have risen relative to coal prices, with more coal used to fuel power generation; and

- Some nuclear plant, which is non-carbon emitting from a generating perspective, has been retired.

In addition, as the proportion of gas used for electricity generation has generally risen, so the availability of UK-produced gas has systematically been decreasing, at least since 2000, and this trend is expected to continue in the future. Also, increases in input fuel prices have led to an increase in the price of electricity to consumers, particularly in the latter part of 2005.

It would now appear that market forces on their own will be inadequate in achieving the UK’s objectives. On the contrary, they are delivering:

- Increasing reliance on a single fuel, in this case gas, which in turn gives rise to risks to security of supply by increasing import dependence;

- Lack of control over any rises in fuel prices due to a substantial degree of commodity speculation as a consequence of growing traded markets; and

- An inadequate rate of reduction in carbon dioxide emissions despite increasing urgency on this key issue. In this context, HM Government has started to intervene in the energy sector in recent years in order to try to deliver its objectives by providing additional incentives to supplement market forces. However, these interventions alone are unlikely to deliver the greater environmental protection now required.

In summary, the electricity generation mix in the UK is changing and the emerging energy gap will need to be filled with new capacity as existing plant retires to enable demand to be met. This situation has created a critical dilemma for policy makers and all those affected by their decisions.

The emerging energy gap can be characterised as follows:

- The average age of electricity generating plant in the UK is 28 years;

- Within the next eighteen months, construction will need to begin on between 2,000 and 5,000 MW of new or extended plant, to meet existing demand needs in the near term; and

- By 2020, over 50 GW of new generation capacity will need to have been added, extended or refurbished, which represents approximately two-thirds of current capacity.

While a contribution to narrowing the emerging energy gap can undoubtedly be made by intensifying efforts around demand management initiatives, the majority of the UK’s response will necessarily be through managing supply and the addition of new generation capacity.

The Government has now resolved to undertake a full review of the possibility of nuclear new build, and the introduction of other low carbon technologies, with the announcement of an energy policy review in December 2005. In formulating a revised UK energy policy, HM Government will need to consider challenging issues around the technical solutions available, such as civil nuclear new build, the development of carbon capture and storage (‘CCS’) and the use of renewable technologies.

Practical introduction of these technologies on a commercial scale could take up to a decade or more to plan, build and commission. Accordingly, HM Government and other key stakeholders need to recognise that action is required now in order to deliver a robust solution to address the energy gap and achieve our environmental objectives. A review of current UK energy policy is set out in Appendix 1.

In the next section, we set out our approach to providing a fresh perspective on these complex issues.

Gas

Where will gas supply be sourced and what issues does importing gas present? What proportion of the required gas can be regarded as secure?

As the UK becomes a net importer of gas again, the risks associated with sourcing and transporting it in appropriate quantities at an acceptable price will be key in assessing the appropriate CCGT contribution to the future power mix.

What is the required level of gas storage capacity?

The low volume of gas storage capacity in the UK will need to be addressed to mitigate the risk of future fuel supply failure.

What are the issues around using LNG in the gas mix?

The transportation of gas to the UK as LNG imposes different fuel supply risks from those associated with pipelines, since there is an inherent reliance on shipping and additional competition from overseas countries for adequate supplies.

Demand management

Who will take responsibility for demand management?

The emerging energy gap may not only be closed by supply side activity but also through making significant impact on the demand side. Though future energy prices will be influential, HM Government policy will also have a large part to play in reducing demand, through appropriate incentives and policies to initiate/encourage demand side responses. Demand management 11 "The Government has now resolved to undertake a full review of the possibility of nuclear new build and the introduction of other low carbon technologies."

What needs to be achieved?

In the context of the developments and challenges presented by the UK’s current energy position, we have undertaken a considered review of the potential level and mix of power generation in the year 2020 and beyond. We have chosen this timescale for a number of reasons:

- Working to a time horizon of 15 years is consistent with the significant generation capacity which will come off-line in this period. This means that decisions about policy will need to be made imminently to fill the emerging energy gap, given the expected lead time for the delivery of new facilities;

- The technologies available for delivery over this period are relatively well defined at the present time implying that the scope of policy choices is relatively clear; and

- HM Government made a commitment in the 2003 Energy White Paper to reduce carbon dioxide emissions by 60% by the year 2050 and to make ‘real progress’ towards meeting this target by the year 2020.

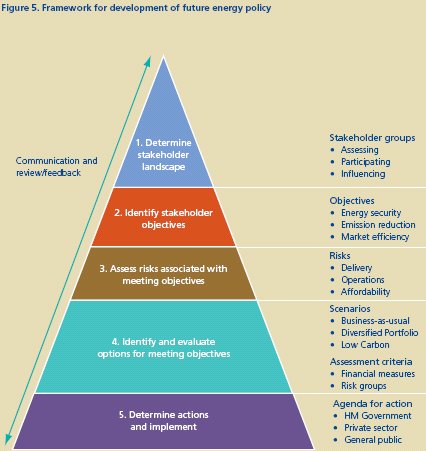

We have undertaken our review using a structured approach, outlined in Figure 5, for assessment of the options available.

Our aim is to provide a coherent framework for decision making within which all stakeholders can contribute meaningfully to the debate which will follow in 2006 and beyond. The purpose of this approach is demonstrably to connect stakeholders interests with the key choices made regarding our future energy needs.

In this way, the risk of making decisions which are not consistent with the overall objectives is reduced and stakeholder engagement is improved.

Determine the stakeholder landscape

In order to understand the context for decisions on future power generation policy, we have considered the stakeholder groups who are contributing to the debate and who have a primary interest in the form of future energy policy and electricity generation.

We have categorised the stakeholders into three groups, defined as follows, although these roles are not necessarily mutually exclusive:

- Assessing Stakeholders – These stakeholders are instrumental in determining whether the future power mix achieves the desired outcomes. They include the national and international Government organisations who have a say in the policies and objectives set and the wider institutional bodies which take an holistic view of energy policy development;

- Participating Stakeholders – These stakeholders participate in the arrangements for delivering the power mix. Participating stakeholders are important because if their primary objectives are not met (for example, creating profits for shareholders) they could reduce or ‘withdraw’ their co-operation, making the proposed solution undeliverable; and

- Influencing Stakeholders – These stakeholders are able to influence both assessing and participating stakeholders and their views need to be taken into account when choosing the most appropriate direction for future energy policy. Influencing stakeholders do not directly affect the success of the proposed solution, although their indirect influence can have an important effect. Understanding the role played by stakeholders in the debate is key to establishing an open dialogue and interpreting their comments – success is very much in the eye of the stakeholder.

Define stakeholder objectives

We carried out a review of publicly available information. The stated objectives of the key stakeholders can be summarised as follows: energy security, reduction in carbon dioxide emissions and demand for efficient markets.

Energy security

Objective: Ensure that the supply, generation and distribution of electricity is continuously able to meet demand, so that physical supply is not interrupted. Contributing objectives include ensuring:

- Robust infrastructure – All aspects of the infrastructure are sufficiently robust to minimise disruption due to physical or technological supply, generation or distribution failures;

- Adequate capacity – The capacities for fuel supply, fuel storage, power generation, transmission and distribution are all sufficiently large to meet the required demand;

- Technology diversity – The technologies used to generate the required electricity or fuel supply are sufficiently diverse that shortfalls in one area can be made good by another;

- Reliance on overseas markets – Reliance on specific nations for the supply of fuel and / or electricity is both diverse and optimised; and

- International relations – Those nations from whom fuel and electricity is imported have, where possible, strong relations with the UK and are politically secure and stable.

Emission reduction

Objective: Ensure that the environmental impacts of fuel supply, generation and distribution activities are kept to a minimum, without competitively disadvantaging the UK in the global market. Contributing objectives include ensuring:

- Meeting emissions targets – The UK targets associated with climate change and pollution are met;

- Compliance – There is a high level of compliance with environmental governance standards;

- Market framework – The market framework is appropriately structured to promote actions to minimise the impact of electricity generation, transmission and distribution activities on the environment;

- Technological innovation – Research, development and demonstration of new low carbon and environmental pollution abatement technologies is adequately funded and delivered;

- Commercial viability – The timely availability of commercially viable, low carbon dioxide and environmental pollution abatement technologies is facilitated; and

- Health & Safety – Electricity is supplied, generated, transmitted and distributed safely.

Market efficiency

Objective: Ensure that fuel supply, electricity generation, transmission and distribution markets operate efficiently, that appropriate capital investment is encouraged and that the affordability of energy is optimised. Contributing objectives include ensuring:

- Reliability – The operational reliability and efficiency of the generation, transmission and distribution systems are effective in balancing the market for electricity supply and demand;

- Low barriers – Technical, economic and regulatory barriers that could impede technological advancement are minimised;

- Effective competition – Competition within the UK and international supply, generation and distribution markets is effective, with transparent and consistent regulation ensuring there is a ‘level playing field’ across the European Union;

- Adequate investment – Effective and appropriate private sector investment from UK and overseas investors is encouraged;

- Fuel price exposure – The effect of changing fuel prices across the electricity production cycle is minimised; and

- Affordability of electricity – The affordability of electricity to the end consumer is optimised and ‘energy poverty’ is eliminated.

Meeting these objectives along with the Government’s fourth objective, which includes eliminating energy poverty, reflecting the Government’s social and public policy responsibilities, is key to delivering stakeholder needs.

Key risks associated with meeting objectives

To assess how effective a potential energy mix would be in achieving stakeholder objectives, it is important to understand the risks associated with an inability to meet the objectives.

We have taken an holistic view of the possible generic risks and their potential impact on particular energy mix options and the delivery of objectives. In total, we have analysed over 40 individual risks, grouping each according to its ability to affect 1) delivery of the mix, 2) on-going operations of the mix or 3) affordability. The risks and risk groups are itemised in Appendix 3.

Risk is defined as an event or action (or inaction) which impairs or prevents the achievement of stakeholder objectives. Understanding the nature and potential impacts of risks is an important part of the debate to allow key decisions to be made in an informed manner, and allow mitigating strategies to be developed.

The consequences of failing to mitigate the impact of risks will vary depending on the nature of the risk concerned, its relationship with the objectives, and its significance (of impact) and likelihood (of occurrence). For example, the consequences of failing to manage properly the risks associated with energy security could result in the UK becoming overly reliant on a small number of technologies, and suffering electricity shortages if fuel supplies are not adequate to meet demand. The knock-on effects of such a situation could theoretically include rationing of power, interruption to energy intensive commercial and industrial activities, transfer of orders to overseas locations for fulfilment and ultimately UK job losses. Avoiding or limiting the impact of such undesirable consequences is a key driver behind the analysis which supports decision making.

The detailed risk analysis provides a comprehensive framework against which stakeholder interests can be referenced and challenged in order to determine the potential impact of energy policy decisions.

Delivery

With respect to the delivery of objectives, the principal risks are considered to be:

Availability – Lack of availability of proven technology, skills and/or labour to deliver and operate the necessary generation capacity, specifically in low carbon technology. In particular, the technology will need to be economic and will have to take account of geographical constraints, such as the availability of suitable sites and the planning requirements that apply to certain types of technology, for example wind and nuclear;

- Markets – Markets that are not effectively designed to promote the development and delivery of new technology, specifically low carbon dioxide generation capacity. For example, the risk that the carbon price does not find a high enough level or lacks sufficient certainty over time to stimulate and sustain appropriate capital investment in low carbon generation; and

- Political – Political issues such as the importance of energy security, role of nuclear new build and climate change on the political agenda and the willingness, or otherwise, of HM Government to commit to implementing or sustaining a long-term policy and regulatory regime which encourages appropriate actions.

Operations

The principal risks associated with operating the future energy mix are considered to be:

- Failure – Failure to meet the demand for electricity caused by either a mechanical defect or a technology failure. This could include failure of the fuel supply and/or electricity transmission and distribution systems caused by adverse weather or a catastrophic event. These risks could materialise, for example, as a result of a major pipe leakage, unforeseen plant shut down, an interconnector failure or a major transmission failure;

- Capacity – A lack of capacity in the fuel supply infrastructure or generating portfolio, leading to an under-supply of electricity and failure to meet the required demand at a particular time or in a particular place; and

- Supply – Supply risks associated with the availability of required fuel for generation, both in terms of the amount and quality of fuel needed and the political stability of, and our relationships with, overseas fuel supplier nations and individual suppliers.

Affordability

With respect to affordability the principal risks are considered to be:

- Cost – Issues associated with insufficient capital investment due to an inadequate level of ‘bankability’ of projects, volatile fuel prices, or a lack of shareholder value; and

- Competition – Issues affecting the competitiveness of UK plc in global markets due to the scale and cost of imports of labour, materials and fuel, or the cost of meeting environmental targets. In the next section, we set out the scenarios developed to inform our analysis.

Carbon capture and storage

What financial incentives, if any, are needed for the technology to become commercially attractive?

Efforts to develop new energy sources, such as carbon capture and storage, can easily be thwarted by cheaper electricity from other sources. Effective mechanisms that promote investment in new technologies, and which help to drive down the cost of generation, should be sought.

Will there be appropriate sites for deployment and roll-out of this technology in the UK?

One of the main factors for consideration in the development of carbon capture and storage facilities in the UK is the proximity of suitable sites for development.

Footnotes

1 CCGT – Combined Cycle Gas Turbine

2 CCS – Carbon Capture and Storage

3 Survey by YouGov commissioned by Deloitte – November 2005

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.