Originally published March 2011

Keywords: budget, tax, G20, competitive tax system, chargeable equity, chancellor,

The Chancellor has attempted to deliver a budget which stimulates growth – and which gives the UK the most competitive tax system in the G20 - but which at the same time keeps UK plc on track to reduce the deficit. Of course, only time will tell whether the Chancellor's ambitions are met. However, some significant changes have been made, and given that his stated objective is that the Budget changes should be fiscally neutral through 2015, then the changes mean that he is giving in some areas, and taking in others.

Some of the more interesting announcements are as follows.

- The drop in the main rate of corporation tax to 26% (and to 23% by April 2014) is very welcome. Unfortunately for the banks to some extent this will be compensated for by an increase in the bank levy to 0.078% (short term chargeable liabilities) and 0.039% (long term chargeable equity and liabilities) from 1 January 2012.

- The Chancellor acknowledged that the UK tax system (which has the longest tax code in the world) is far too long and needs simplification. The abolition of 43 minor (and in many cases obsolete) reliefs is welcome, but far more significant is the heavily predicted proposal (subject to consultation) to merge the income tax and national insurance systems.

- However, there is a contradiction in the Budget, since the Chancellor also announced a raft of new anti-avoidance measures (further increasing complexity) and the retention, subject to amendment, of the notorious IR35 legislation aimed at personal service companies.

- Entrepreneurs, and what might be called entrepreneurial activity, are the winners in this year's Budget. The capital gains tax entrepreneur's relief lifetime limit (which gives an effective 10% tax rate) is doubled to £10m. R&D tax credits for SMEs are also to be increased, as is the lifespan of short life assets (from 4 to 8 years) that benefit under the capital allowances short life assets regime. Increases in EIS and VCT relief are also announced, subject to EU state aid approval.

- Oil and gas companies are the losers in this years Budget. Oil and gas companies face a substantial increase in the supplementary charge (applied to their ring fenced production activities) from 20% to 32% (an eye watering net tax rate of at least 62% when added to their corporation tax rate). The supplementary charge will be scaled back once oil goes below the "trigger price" (expected to be about $75 per barrel).

As always, the devil will be in the detail in relation to many of the announced measures (particularly those dealing with anti-avoidance) and thus we await publication of the draft Finance Bill 2011 on 31 March. Nonetheless, there follows a summary of the main Budget announcements.

Business

In support of the Government's stated aim to make the UK the "most competitive tax system in the G20", the Chancellor used the Budget to confirm a further reduction in the main rate of corporation tax. This comes alongside the already published plans to revamp the 'controlled foreign company' (or "CFC") and taxation of foreign branch profits rules, both of which have generally been well received by the business community. However, certain business sectors - notably, the financial and oil and gas sectors - have not escaped unscathed and indeed may feel that they are 'footing the bill' for the Government's more popular tax reforms.

Corporation tax rates: with effect from 1 April 2011, the main rate of corporation tax will fall from 28% to 26% - this represents an additional 1% reduction compared to the reductions announced in the June 2010 Budget. Three further annual reductions of 1% are scheduled, bringing the main rate of corporation tax down to 23% from April 2014. The 'small profits' rate of corporation tax will also reduce on 1 April 2011 from 21% to 20%, in line with previous announcements.

Interim CFC reform: following on from the discussion documents and draft legislation published last year, Finance Bill 2011 will include interim CFC reform provisions, which will have effect for accounting periods beginning on or after 1 January 2011. The main interim change to be introduced is a new exemption for certain intra-group transactions with a minimal UK connection. There is also a new exemption for CFCs with a main business of IP exploitation with a limited UK connection. Finally, the new rules introduce a three year statutory exemption for foreign subsidiaries that have not previously been subject to the UK's CFC rules (e.g. as a result of a reorganisation, acquisition or corporate groups migrating into the UK); the conditions of the existing de minimis exemption are to be amended, mainly increasing the minimum chargeable profits requirement (in a 12 month accounting period) to £200,000 from £50,000 for groups including 'large' companies; and transitional rules introduced under Finance Act 2009 for 'superior' and non-local holding companies – permitting such entities to rely on the 'exempt activities' exemption – are to be extended until July 2012 (in line with the completion of 'full' CFC reform scheduled for Finance Bill 2012). A consultation document on the full CFC reform programme is to be published in May 2011, with draft legislation due in autumn 2011 for subsequent inclusion in Finance Bill 2012.

Foreign branch tax exemption: again a continuation of measures discussed and draft legislation made available last year, Finance Bill 2011 will include an 'opt-in' tax exemption regime for foreign branch profits, to take effect in relation to accounting periods commencing on or after Royal Assent. The essence of this new elective regime is that, once an election has been made and subject to transitional rules to require the matching of tax losses of a foreign branch against profits, the qualifying profits of a foreign branch will be deducted from a UK company's worldwide profit calculation to establish a net amount which is subject to UK corporation tax. Potentially exempt foreign branch profits are to be quantified by reference to individual double tax treaties between the UK and the relevant branch jurisdiction where such treaties contain a 'non discrimination' clause. In other cases (including where there is no applicable treaty, except in relation to branches of 'small' companies in non-treaty countries, to which the regime will not apply), exempt profits are to be determined as if the treaty were a full treaty incorporating the OECD Model Tax Convention. This measure is designed to help achieve greater consistency of tax treatment between foreign branches and foreign subsidiaries.

Oil and Gas taxes: with effect from 24 March 2011, the rate of the supplementary charge levied on profits from oil and gas production in the UK and on the UK continental shelf will be increased from 20% to 32%. However, the new rate will apply in conjunction with a 'fair fuel stabiliser', the effect of which is that if in future years the price of oil falls and stays below a set trigger price (expected to be US $75 per barrel, subject to ongoing consultation with affected parties), the Government will reduce the rate of the supplementary charge back towards 20% in proportion to the prevailing price of oil.

The Government has also announced its intention to introduce rules in Finance Bill 2012 (with effect from the 2012 Budget) to restrict tax relief for decommissioning expenses to the 20% rate of the supplementary charge. Finally, with effect from 23 March 2011, new rules will apply to ensure that the intangible fixed asset regime does not permit a company to obtain a debit in calculating its profits where it acquires an oil licence or an interest in an oil licence from another company. Oil licences and interests in them are already excluded assets under the intangible fixed asset rules – this exclusion is now being extended to cover all goodwill and any other intangible asset which relates to, derives from or is connected with an oil licence or an interest in an oil licence.

Bank levy: the bank levy rates will be increased from 1 January 2012 to 0.078% for short term chargeable liabilities and 0.039% for long term chargeable equity and liabilities. The Government has partly explained this rate increase as a means of offsetting the further corporation tax rate reductions described above. The bank levy is due to be formally reviewed in 2013 to ensure it is operating efficiently.

Funds: new rules will apply from the date on which Finance Bill 2011 receives Royal Assent which will ensure that a UCITS fund that is established and regulated in another EEA state is not treated as UK tax resident simply because it has a UK tax resident fund manager.

Disregard regulations: the Loan Relationship and Derivative Contract (Disregard and Bringing into Account) Regulations 2004 (the "Disregard Regulations") broadly allow companies to defer the bringing into account of certain foreign exchange gains and losses on loan relationships or derivative contracts. Changes to the Disregard Regulations will be introduced in relation to accounting periods beginning on or after 1 July 2011, allowing companies to ignore foreign exchange gains and losses on loan relationships and derivative contracts where these reduce the company's foreign exchange exposure in relation to its own foreign currency preference shares which are issued to nonconnected entities and are accounted for as liabilities.

For accounting periods beginning on or after 1 January 2012, a company will be able to: (i) defer its foreign exchange gains and losses on loan relationships and derivative contracts which reduce the company's foreign exchange exposure in relation to foreign currency assets held in a partnership, until the partnership disposes of those assets or the company disposes of its interest in the partnership; and (ii) to defer foreign exchange gains and losses where the company disposes of foreign currency shares with deferred sale proceeds. Draft regulations are to be published shortly on the HMRC website, with informal consultation scheduled for May 2011.

Capital allowances: businesses investing in qualifying plant or machinery will be able to elect for short life asset ("SLA") treatment on an extended basis. Currently, plant and machinery subject to a SLA election is allocated to a single asset pool for a cut-off period of four years – items which are sold or scrapped within four years may generate a further allowance (or charge) depending on the difference between any disposal proceeds and the written down balance of expenditure applying to those items. If plant and machinery under a SLA election is not disposed of within four years, it is transferred to the main capital allowances pool. From 1 April 2011, the four year cut-off period is being increased to eight years – this is likely to benefit businesses making substantial investments in qualifying plant and machinery.

The enhanced capital allowances rules – which provide for 100% first year allowances for expenditure on certain energy-saving technologies – are to be revised to with a view to including certain energy efficient hand dryers within the scope of the rules. This change is subject to state aid approval, but is scheduled to take effect on a date to be specified before the Summer 2011 parliamentary recess.

R&D tax credits: subject to state aid approval, the Government will legislate to: (i) increase the additional tax deduction (payable tax credit) available to SMEs for qualifying R&D expenditure from 75% to 100%, with effect from 1 April 2011; and (ii) increase the additional tax deduction available to SMEs further from 100% to 125%, with effect from 1 April 2012. Alongside the increased R&D tax credits, the Government will consult on plans to simplify the R&D tax rules, including proposals to abolish the rule restricting an SME's R&D payable tax credits to the amount of PAYE and NICs it pays and abolishing the minimum £10,000 expenditure requirement for all companies (not just SMEs).

Individuals

There are no major changes in the Budget to individual taxation, although there are some measures – in particular in relation to EIS/VCTs, entrepreneurs' relief and the remittance basis – aimed at promoting growth. The following is not an exhaustive list of the proposed changes.

Income Tax/NIC rates and allowances: no changes in the headline rates, although the chancellor confirmed that the 50% tax rate for those earning over £150,000 is a temporary measure, without indicating when it would end. There is a little tinkering with annual allowances, which will benefit the lower paid, but it appears that the majority of the cost of this will eventually be recovered from changing the basis of indexation for NIC limits and thresholds from RPI to CPI (which HMRC state will generate more than £1 billion in 2015/16).

EIS/VCTs: one area of the tax code which evolves at a much faster rate than much of the rest is that dealing with the Enterprise Investment Scheme (EIS) and Venture Capital Trusts (VCTs). The trend recently has been to restrict these reliefs, and this had got to the stage where they were of limited attraction to investors. However, this may now change, with proposals to extend the reliefs significantly.

For EIS, income tax relief will be available at 30% rather than 20%, for shares issued on or after 6 April 2011, and the maximum amount that an individual can invest will be raised from £500k to £1m for shares issue on or after 6 April 2012, in each case subject to state aid approval.

For both EIS and VCTs, the following changes are proposed for investee companies: (i) employee limit to rise from 50 to 250; (ii) gross assets threshold to rise from £7m to £15m before investment (and it appears that the current £8m limit on gross assets after investment will be abandoned); and the maximum amount which can be invested in a company to rise from £2m to £10m. These changes are intended to take effect for shares issued after 6 April 2012, subject to state aid approval.

Entrepreneurs' relief: another relief which is subject to frequent change, even in its short life (it was introduced in 2008) is entrepreneurs' relief, which gives qualifying disposals a capital gains tax rate of 10%. Here the changes have all been in the direction of extending the relief, and this year's budget is no exception, with the lifetime limit for qualifying disposals being increased to £10m from £5m, for disposals on or after 6 April 2011.

Employee transport: the Government is to increase the level of Approved Mileage Allowance Payments from 40p to 45p per year for the first 10,000 miles per year of business travel in the employee's own vehicle. Reimbursements of costs up to this level by the employer will not be taxable. However, another of the proposed changes, under the banner of "tax simplification", is to remove the relief for reimbursement to employees of taxi fares for late-night travel home.

Disguised remuneration: one of the main anti-avoidance provisions being implemented at present is the new rules on "disguised remuneration", aimed in particular at closing down tax avoidance arrangements using employee benefit trusts and loans. The budget documentation primarily recapped what had already been announced in this area, but there was confirmation that the measures would be contained in the Finance Bill 2011: there had been speculation that this would be deferred.

Non-domiciles: the Government intends to increase the annual charge from £30,000 to £50,000 for non-domiciles who have been UK resident for 12 or more years. The £30,000 charge will be retained for those who have been resident for at least seven of the past nine years and fewer than 12 years. Also, they intend to remove the tax charge when non-domiciles remit foreign income or capital gains to the UK for the purpose of commercial investment in UK business. These measures are intended to be adopted from April 2012 after consultation.

Anti-avoidance

Last year, the Government was simply looking to put sticky plaster on the issue of anti-avoidance. This year they have sought to outline a strategic plan to deal with perceived avoidance on both a macro and micro level.

Hallmarks: the Government is seeking to ensure that there is no cash flow benefit from participating in certain tax avoidance structures. Subject to consultation this year (and legislation in 2012), schemes which have been struck down by the courts or which (based on independent advice) have been identified as failing to deliver the desired tax advantages will be listed in regulations, with 'statutory consequences' (late payment penalties) for their use.

In addition, an informal consultation will take place this year to look at a number of changes which were made to the disclosure of tax avoidance schemes regime which took effect from 1 January 2011. These included two new hallmarks with respect to income into capital schemes and employment schemes, but the draft legislation for these proposed hallmarks was seen as too wide and their introduction was deferred.

New approach: the Government has published a document which summarises its proposed strategic approach to tackling tax avoidance. It outlined strategies with regard to prevention, detection and counteraction. The document makes reference to certain areas which have been previously discussed, including principles based legislation, the recently announced study group on a general anti-avoidance rule and an update on HMRC's litigation strategy. The Government has also announced a programme of reviews of high risk areas of taxation policy, which include income tax losses and unauthorised unit trusts, with legislation in these areas expected in Finance Bill 2013. The document also outlines a protocol for the introduction of unscheduled changes in tax law where there is a significant risk to the tax take and significant new information has recently become available. The Government will consult on these proposals going forward.

Leasing: new legislation will be introduced and will potentially apply to any group that has entered into a sale and leaseback arrangement involving reacquisition of assets in which a long funding lessee claims relief for residual value guarantee payments more than once.

The Budget's announcements include further amendments to capital allowances legislation which ensures that the sale of lessor companies rules operate as intended. The changes target a range of planning ideas intended to enable a group to avoid the effect of the legislation. HMRC are also withdrawing the option to elect provisions introduced in 2009 (which allow lessor companies to choose to ring fence the future profits of the leasing business following a sale as an alternative to suffering an immediate tax charge and a subsequent deduction under previous changes), as they consider that this deferral mechanism has been exploited.

Tax treaties: subject to consultation and legislation in 2012, the Government will introduce anti-avoidance rules to ensure that treaty relief or exemption is not given where arrangements have been made in relation to a claim to avoid UK tax. Whilst there are limited details provided, the Government is targeting UK residents that engage in 'tax avoidance schemes' and non-residents (primarily based in countries with which the UK does not have a tax treaty) who enter into arrangements to obtain benefits under the UK's double taxation treaties. Taxpayers will need to await further details of the proposal in order to assess the impact. Typically such issues are dealt with in the treaties themselves by way of 'conduit', 'treaty-shopping' or 'limitation on benefits' provisions. Alternatively, some jurisdictions take the approach of using domestic law to deny treaty reliefs in abusive situations.

Loan relationships and derivatives: numerous anti-avoidance changes have been made. The Government has made certain clarifications and changes regarding the derecognition of amounts in respect of loan relationships and derivative contracts. It has clarified that the anti-avoidance provisions will not apply where a party does not itself have a tax avoidance purpose. It will also revise the legislation to make clear that the anti-avoidance provisions do not apply where a company is no longer party to the loan or derivative following derecognition. These changes will have effect from 6 December 2010.

With effect from Budget Day, the legislation will also be amended to deal with circumstances where, if a derivative is caught by the anti-avoidance rule, a credit is to be brought into account to the extent that its fair value exceeds its carrying value at the start of the accounting period in which avoidance arrangements are entered into. This is to deal with situations where an off balance sheet derivative is transferred as part of tax avoidance arrangements and it is an "in-the-money" derivative.

Group mismatch rules: in response to comments received on the technical note and draft legislation published on 6 December 2010, the following clarifications will be made to the proposed rules: (i) changes will be made to clarify that the group mismatch scheme rules take precedence over the worldwide debt cap rules, the transfer pricing rules and the arbitrage rules; (ii) the legislation will be amended to make clear that the group mismatch rules do not apply where an asymmetry arises because one group company is outside the scope of UK corporation tax; and (iii) where a group mismatch scheme exists, a de minimis tax saving threshold of more than £2m (assuming that the scheme is designed to produce a 'relevant tax advantage') will be introduced. Aligned with this will be changes to the purpose condition to focus on situations where there is more likely to be a tax advantage, so as to avoid catching certain commercial arrangements.

Capital gains: changes intended to simplify three areas of the chargeable gains rules will be introduced in Finance Act 2011. These were proposed last year and draft legislation has previously been published. There are specific rules which restrict the use of certain capital losses where a company is acquired by another group. The rules are intended to prevent "loss buying" schemes (whereby a group buys a company pregnant with capital losses with a view to sheltering its own capital gains).

The "value shifting" legislation is to be replaced by a simpler, motive-based rule. Under the new rule, there would be a just and reasonable adjustment of the consideration received on a disposal of shares where there are arrangements that have reduced the value of those shares with the purpose of avoiding a liability to corporation tax on chargeable gains. There are important changes to the de-grouping rules, the main one being that the conditions for the substantial shareholding exemption are to be changed so that it may be possible for the seller to "hive-down" a target business into a new company and sell that new company without a de-grouping liability arising and without the seller paying tax on the disposal. Further detailed changes to these reforms have been announced in response to comments raised during the consultation and the Government also announced amendments to the de-grouping rules designed to close a loophole which may have allowed assets to be transferred intra-group followed by a sale of the transferee without a de-grouping liability arising.

Indirect taxes

SDLT

Preventing avoidance: HMRC has been concerned for some time about SDLT avoidance in both the commercial and residential sectors. A case of SDLT avoidance in the First-Tier (Tax) Tribunal was decided last month in favour of the taxpayer (DV3 RS Ltd Partnership v HMRC). This case exploited the use of sub-sale relief and the SDLT partnership rules, but it is far from clear that HMRC argued avoidance in that case or whether HMRC will appeal that decision. In any event, HMRC has decided to shut down a number of structures exploiting: (i) the relationship between the sub-sale rules and Alternative Finance reliefs; (ii) the use of a consumer credit licence so as to be a "financial institution" for Alternative Finance reliefs; and (iii) the way consideration is determined where land is exchanged.

These changes have almost immediate effect (from 24 March 2011) subject to certain transitional provisions where contracts were entered into prior to 24 March 2011. It remains to be seen whether new viable SDLT structures will continue to be developed.

VAT

Low Value Consignment Relief ("LVCR"): concern has been expressed by some UK retailers (often, it seems, those with struggling businesses) about competitors who deliberately locate outside the EU (e.g. in the Channel Islands) in order to supply UK consumers with products such as CDs, DVDs and contact lenses free of UK VAT. The reason for this relief is to ease administration for businesses, HMRC, Royal Mail and other carriers as well as consumers themselves. At present the EU Directive has a £9 LVCR threshold, but permits Member States to increase the limit to £20. The UK LVCR threshold is currently £18.

As an interim measure, in order to create a more level playing field and to stem the loss of VAT revenues, the Government has announced that it will reduce the LVCR threshold to £15 with effect from 1 November 2011. At the same time, it will explore options with the European Commission to produce a workable solution, or (failing that) to reduce the LVCR threshold further next year.

Registration and deregistration thresholds: with effect from April 2011, the VAT registration threshold will increase to £73,000 (from £70,000). The VAT deregistration threshold will increase to £71,000 (from £68,000). VAT registration/deregistration and notification of changes must be done online from 1 August 2012 which (we are told) will "improve processing time and reduce contact with HMRC". Any businesses that are currently filing paper VAT returns (namely those with turnovers of less than £100,000) will have to file online and pay electronically from 1 April 2012.

Administration and consultations

Cross border enforcement: Finance Bill 2011 will include legislation to enable the UK to implement the Mutual Assistance Recovery Directive. From 1 January 2012, EU Member States will provide each other with assistance in the recovery of tax and duty debts.

Time to pay: the TTP regime will continue to enable businesses in financial difficulty to defer some of their tax debts. This is a welcome (albeit expected) announcement given the continuing difficult economic climate.

Data-gathering: as previously announced and following consultation, new draft legislation will be published (for inclusion in the Finance Bill 2011) that enables HMRC to issue notices requiring "relevant data holders" to provide HMRC with "relevant data". It will be interesting to see how widely these powers are used in practice once introduced.

Consultations

Integrating income tax and NIC: the Government will publish a consultation document later this year on the options for, and challenges posed by, integrating the operation of income tax and NIC. Whilst this may take years to implement, it is hugely significant in terms of cutting the compliance burden and to be strongly welcomed.

Reviewing non-domicile taxation: the Government has said that it will introduce the measures referred to earlier in relation to non-domiciled individuals from April 2012. A consultation document will be published in June 2011 which details how the measures will be achieved. It is welcome that the Government announced that no further changes to the taxation of non-doms will be made in this Parliament.

Statutory residence test: with the intention of introducing legislation in Finance Bill 2012, the Government will publish a consultation in June 2011 on a statutory residence test. There is considerable difficulty, and scope for avoidance, in having a hard and fast rule for residence. It will be interesting to see how the Government proposes to tackle this difficult area.

REITs: an informal consultation with REITs and their advisers will take place shortly, with a view to making the REIT regime more attractive. The proposals include the abolition of the entry charge on conversion for companies joining the REIT regime, and the ability to be a private (i.e. unlisted) REIT.

Tax transparent funds: legislation will be introduced in April 2012 establishing a new tax transparent fund vehicle, and a consultation document should be published in June 2011. This measure, previously announced, will be welcomed by the UK fund management industry.

IR35: it will come as a disappointment to some that the Government has decided against scrapping the IR35 legislation aimed at personal service companies. Instead, they will aim to "achieve simplification" by "making improvements" to the administration of IR35. Thus, after a considerable review and much debate, this particular part of the UK's very long and very complex tax code remains unchanged, despite the obvious need for reform.

Patent box: the Government will continue to consult on this measure, which is part of the "corporation tax roadmap" process. A consultation document is due to be published in May 2011 and it is expected that legislation will be included in Finance Bill 2012.

Capital allowances: The Government has announced a number of consultations in relation to capital allowances. In conjunction with the Government's announcement of the creation of 21 new Enterprise Zones, the Government will consider introducing enhanced capital allowances to support Enterprise Zones in areas where there is a strong focus on high value manufacturing. Further, the Government will publish a consultation document in May 2011 (with a view to introducing legislation in Finance Bill 2012) covering its proposals to amend the capital allowances anti-avoidance legislation. Few details are available at present, but it has been suggested that the "sole or main benefit" rule will be replaced with a wider anti-avoidance test as seen "elsewhere in the Taxes Acts". Finally, the Government will, in a document to be published at the end of May 2011, announce details of a consultation on proposals to introduce changes to the capital allowances fixtures rules, which stipulate that businesses must pool their expenditure on fixtures in a building within a short period of acquiring the building in order to qualify for capital allowances.

Worldwide debt cap: the Government has reported that ongoing consultation on the application of the worldwide debt cap rules (which entered into force on 1 January 2010) has identified certain practical issues with the rules that it feels need to be addressed, including in relation to the £3m de minimis amount. Further details are not available at this stage, but the Government will consult on the issues informally through the debt cap working group and through the HMRC website in June 2011. It is anticipated that draft legislation will be published in autumn 2011 for inclusion in Finance Bill 2012.

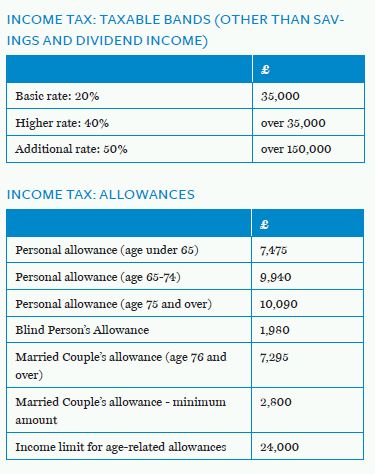

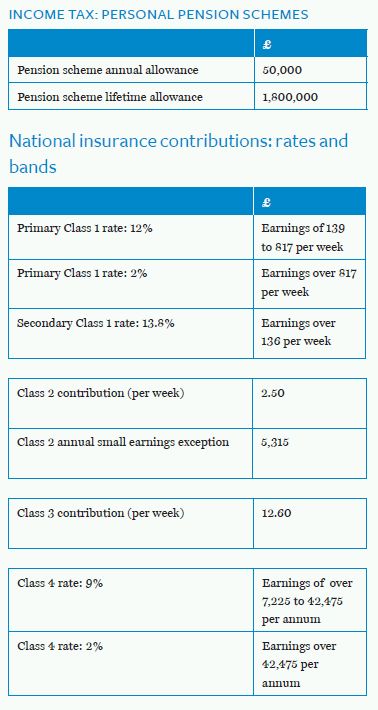

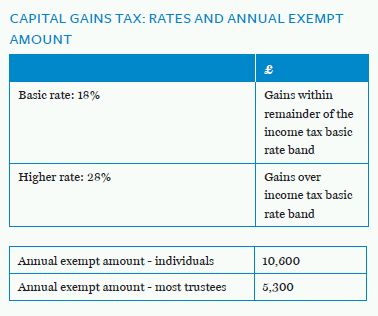

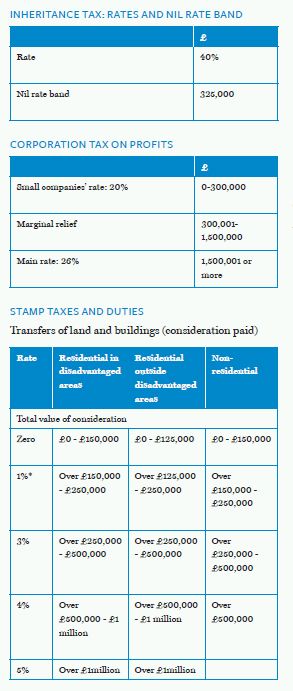

Tax rates and allowances 2011/12

The personal allowance will be reduced where income is in excess of £100,000 by £1 for every £2 of income over £100,000 until the allowance is reduced to nil.

*From 25 March 2010 until 24 March 2012, no Stamp Duty Land Tax will be due on purchases of residential property where the consideration is less than or equal to £250,000 where the purchaser (or all of the purchasers, if applicable) is a first time buyer and intends to occupy the property as their only or main home.

Mayer Brown is a global legal services organization comprising legal practices that are separate entities ("Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP, a limited liability partnership established in the United States; Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales; and JSM, a Hong Kong partnership, and its associated entities in Asia. The Mayer Brown Practices are known as Mayer Brown JSM in Asia.

This Mayer Brown article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein.

Copyright 2011. Mayer Brown LLP, Mayer Brown International LLP, and/or JSM. All rights reserved.