Assets under management of Irish alternative investment funds (AIFs) are at an all-time high. The strategies being pursued by Irish AIFs continue to expand, hand in hand with the introduction of additional legal structures, particularly the Irish collective asset management vehicle (ICAV). Work is also currently ongoing on reforming the Irish investment partnership structure (ILP) and, once complete, there is scope for the further expansion of the strategies being pursued by Irish AIFs, particularly private equity (PE) and real economy investment strategies.

In this article, we highlight what makes the ICAV such an attractive legal structure for AIFs and how its introduction has seen the expansion of strategies being pursued. We also introduce the ILP and highlight the proposed enhancements that are designed to make it a "best of breed" partnership structure.

What is the ICAV?

The ICAV is a corporate vehicle tailored specifically for Irish investment funds, established by way of a registration and authorisation by the Central Bank of Ireland (CBI). It has a distinct and separate legal personality, (i.e. it may enter into contracts itself, can own property itself etc.) and is represented by its board of directors which retains overall responsibility for managing the business of the ICAV.

The ICAV is similar to existing Irish funds established as investment companies but with the significant advantage that the ICAV was specifically created for the Irish funds industry, enabling it to be more flexible than the investment company. The ICAV legislation essentially drew upon the best and most successful aspects of Irish company law, improving it in several material respects. The advantage of this is that with its own specific legislative code, the ICAV will not be impacted by amendments to European/Irish company law (which are targeted at ordinary companies and not funds), protecting the ICAV from any unintended consequences of such legislative changes. The result of this tailored legislative code is a more straightforward set of legal rules applicable to the ICAV, and lower administration and operating costs.

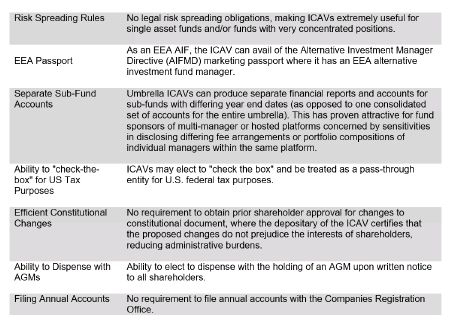

Key Features of the ICAV

Structuring flexibility

The ICAV can operate as a standalone fund or as an umbrella fund with multiple sub-funds which automatically enjoy segregated liability between each sub-fund under the ICAV legislation.

The ICAV can be structured to suit all major investment strategies and can accommodate traditional as well as alternative investment policies. It can also avail of a full suite of liquidity options making it suitable for mutual funds, hedge, real estate, infrastructure, credit, loan origination, PE, managed accounts and hybrid funds. ICAVs can also be established as part of global masterfeeders, co-investment or joint-venture structures and use a full range of underlying special purpose vehicles and subsidiaries to hold investments. The flexibility of the ICAV can be seen through its use to facilitate closed ended PE style strategies that typically would be undertaken through a partnership structure.

Mirroring the global trend of hedge funds engaging in the provision of private credit, ICAVs, established to pursue credit strategies have been the stand out trend since 2017. The relaxation of regulatory rules on origination of loans by Irish loan origination qualifying investor AIFs (L-QIAIFs) in February 2018 now allows L-QIAIFs to undertake a comprehensive mixed asset credit strategy, whereby investment in debt securities, including asset backed securities, primary and secondary lending can all be carried out by the L-QIAIF. This further product development has been welcomed by fund sponsors who to-date have achieved a mixed credit strategy indirectly by pooling L-QIAIF and non-LQIAIF sub-funds of the same umbrella into fund of fund or master-feeder structures.

Success of the ICAV

The ICAV has quickly established itself as the most popular vehicle for asset managers. As of 31 July 2018, 271 ICAVs have been registered with the CBI. More impressively, 80% of all Irish AIFs authorised by the CBI since its introduction have been established as ICAVs. In addition, approximately 12% of ICAVs have converted from investment companies into an ICAV, most notably the conversion of an umbrella scheme with over £43 billion of assets under management and comprising 154 sub-funds in April 2018.

The Investment Limited Partnership 2.0

While the ICAV is sufficiently flexible to accommodate many PE strategies and PE-centric features (such as capital commitment/drawdown mechanisms, distribution waterfalls, carried interest and "excuse and exclude" allocation of assets), historically global asset managers have preferred the limited partnership as the legal form for a PE fund. The ability to establish regulated ILP structures has been possible in Ireland since the implementation of the ILP legislation in 1994, however only a handful of asset managers have chosen to do so, with the general consensus being that this legislation had its limitations.

Against this backdrop, the Irish funds industry has made proposals to the CBI and the Irish Department of Finance (DoF) to enhance the attractiveness of the ILP, through a series of legislative changes to the ILP legislation.

What is the ILP?

The ILP is a regulated common law partnership structure, tailored specifically for Irish investment funds. It is established on receiving authorisation by the CBI and is constituted pursuant to a limited partnership agreement (LPA) entered into by one or more general partner(s) (GPs), who manage the business of the partnership on the one hand, and any number of limited partners (LPs) on the other hand.

Partners

Typical to common law partnerships, the GP is the operative legal entity, responsible for managing the business of the ILP and is ultimately liable for the debts and obligations of the ILP to the extent the ILP do not have sufficient assets. The GP must: (i) be authorised by the CBI to act as a GP; or (ii) avail of the right to manage an Irish AIF on a crossborder basis under AIFMD.

There are no restrictions on the number of LPs that may be admitted to an ILP. The liability of a LP for the debts and obligations of the ILP is limited to the value of their capital contributed or undertaken to be contributed, except where it becomes involved in conducting the business of the ILP. The ILP legislation helpfully includes a non-exhaustive list of 'safe harbour' activities that can be carried out by LPs without being deemed involved in conducting the business of the ILP. This safe harbour list provides additional legal certainty when considering Irish ILPs.

All of the assets and liabilities of an ILP belong jointly to the partners in the proportions agreed in the LPA. Similarly, the profits are directly owned by the partners also in the proportions agreed in the LPA.

Strategies

Like the ICAV, the ILP can be structured to suit all major investment strategies and can avail of a full suite of liquidity options, making it a highly flexible product.

Enhancements

The Minister for Finance announced that the Irish Government has approved the legal drafting of the amendment to the ILP legislation and it is understood that the Heads of Bill (Heads) will be published later this year. Upon making the announcement of the proposed ILP reform, the Minister confirmed that the intention was to enhance and reform the existing legislation in order to align it with international standards for PE funds and certain requirements of AIFMD and ensuring that Ireland remains one of the leading funds domiciles in Europe.

The exact changes included in the Heads will not be known until it is published. However, given ongoing dialogue between the Irish funds' industry, the CBI and the DoF, it is anticipated that the key enhancements shall include: (i) features which improve the operation of ILPs by clarifying the rights, obligations and status of investors, (ii) align the structure fully with AIFMD and other Irish fund structures, (iii) allow for the establishment of umbrella ILPs and (iv) the migration of ILPs. It is also hoped that such enhancements will incorporate "best-of breed" features found in other leading fund jurisdictions that offer partnership structures.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.