- within Family and Matrimonial, Strategy and Privacy topic(s)

- with readers working within the Law Firm industries

INDIRECT TAX

Sabka Vishwas (Legacy Dispute Resolution) Scheme, 2019

- The budget proposes a dispute resolution-cum-amnesty scheme titled 'The Sabka Vishwas Legacy Dispute Resolution Scheme, 2019' (Scheme) for faster settlement of litigation pending inter alia under the erstwhile Central Excise and Service Tax regime.

- Depending on the amount of tax dues involved, the relief under the Scheme varies from 40% to 70% of the tax dues. The Scheme provides relief from payment of interest and penalty and the person discharged under the Scheme shall not be liable for prosecution.

- The amount under the Scheme has to be mandatorily paid in cash and the amount paid shall not be refundable under any circumstances.

The table below captures the relief available to a declarant under the Scheme:

Persons shall not be eligible for making a declaration under the Scheme, if they have:

- filed an appeal before the appellate forum and such appeal has been heard finally on or before 30 June 2019;

- been convicted for any offence punishable under any provision of the indirect tax enactment for the matter for which they intend to file a declaration;

- been issued a show cause notice, under any provision of the indirect tax enactment and the final hearing has taken place on or before 30 June 2019;

- been issued a show cause notice under any provision of the indirect tax enactment for an erroneous refund or refund;

- been subjected to an enquiry / investigation / audit and the amount of duty involved in the said enquiry / investigation / audit has not been quantified on or before 30 June 2019;

- made a voluntary disclosure:

-

- after being subjected to any enquiry or investigation or audit; or

- having filed a return under the indirect tax enactment, wherein he has indicated an amount of duty as payable, but has not paid it;

- filed an application in the Settlement Commission for settlement of a case; or

- are seeking to make declarations with respect to excisable goods set forth in the Fourth Schedule to the Central Excise Act, 1944.

Central Excise Law

The change in excise duties pertain primarily to the tobacco and petroleum sector.

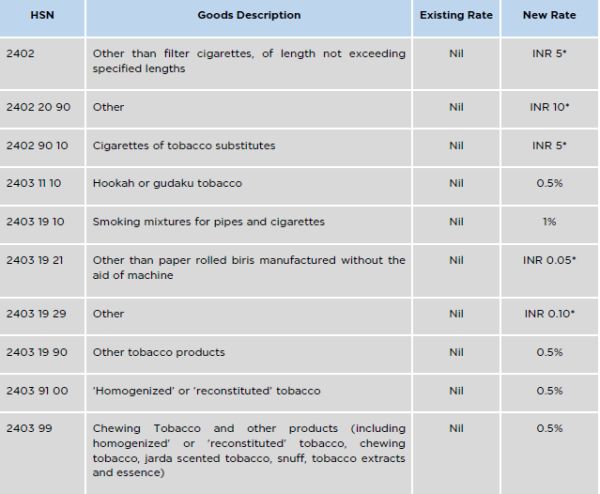

Rate Changes in Tobacco Products

- The Government has increased the effective rate of Basic Excise Duty on tobacco products such as cigarettes, hookah tobacco, smoking and pipe mixtures, chewing tobacco, jarda etc. classified under Chapter 24 of the Fourth Schedule to the Central Excise Tariff Act, 1985, as follows:

Rate Changes in Petroleum Products

- The Government has increased the effective rate of Special Additional Excise Duty and the Road and Infrastructure Cess imposed under the provisions of the Finance Act, 2002 and the Finance Act, 2018, respectively, for petroleum and diesel products.

- The Government has further introduced Basic Excise Duty of INR 1 per ton on manufacture of petroleum crude classified under Tariff item 2709 20 00 of the Fourth Schedule to the Central Excise Tariff Act, 1985. Simultaneously, the Government has exempted petroleum crude produced from blocks under the New Exploration and Licensing Policy or under production sharing contracts from the following notified fields:

-

- Panna and Mukta

- Ravva

- Kharsang

- Mid and South Tapti

- Hazira

- Bhandut

- Matar

- Sabarmati

- Asjol

- Allora

- Unawa

- Modhera

- North Kathana

- Cambay

- Indrora

- Bakrol

- Lohar

- Dholka

- Wavel

- Baola

- PY-1

- North Balol

- Dholsan

- Kanwara

- Amguri

- Sanganpur

Customs Law

Legislative changes

- Aadhaar based identity verification: Failure to comply with verifications by the stakeholders may lead to suspension of transactions with customs.

- Extra-territorial power to arrest Customs authorities are empowered to arrest offenders beyond India or Indian customs waters.

- Expansion of Customs offences:

-

- Cognizable offences: Fraudulent availing or attempting to avail benefits of drawback or exemption exceeding INR 5,000,000 (Indian Rupees Five million).

- Cognizable and non-bailable offences: Fraudulent procurement of duty credit scrips / authorization / license / certificate under Foreign Trade Development Regulation Act 1992, (Instrument) of value more than INR 5,000,000 (Indian Rupees Five million), and utilization thereof.

- Penalty for fraudulent procurement: Penalty not exceeding face value of the Instrument on person obtaining such Instrument by fraud, wilful misstatement or suppression of facts.

- Redemption fine: In respect of cases covered under deemed closure proceedings under Section 28 of the Customs Act, 1962 no fine in lieu of confiscation shall be imposed on the infringing goods.

- Attachment of bank accounts: Provisional attachment of bank account for a period of 6 months (further extendable to 6 months) for the purpose of protecting the revenue or preventing smuggling.

- Amendment of documents: Time limits and other conditions would be prescribed for the amendment of documents post clearance of goods.

- Penalty for contravention of rules: Maximum penalty for contravention of rules and regulations enhanced from INR 50,000 (Indian Rupees Fifty thousand) to INR 200,000 (Indian Rupees Two hundred thousand).

- Anti-circumvention of countervailing duty: Extension of countervailing duty on articles imported in unassembled or disassembled condition or change in the name or composition to circumvent countervailing duty on such articles.

- Statutory appeal against Safeguard duty orders: Statutory appeal against imposition of Safeguard duty shall be with Customs, Excise and Service Tax Appellate Tribunal (CESTAT).

- Printed books: Chapter Notes to Chapter 98 are amended to impose customs duty on the Import of printed books for personal use.

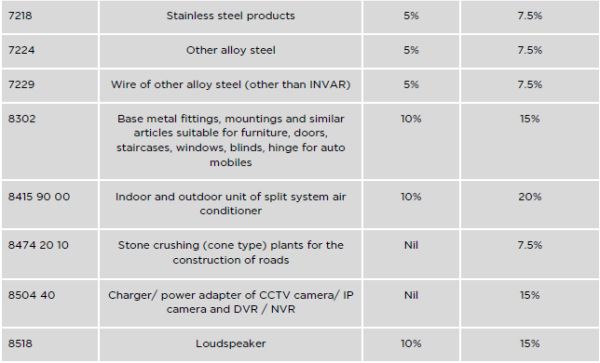

Change in rates of Customs Duty for major items:

This exemption shall cease with effect from 1 July 2024

The customs and central excise rate changes shall take effect immediately, i.e. from 6 July 2019. The legislative changes shall take effect from the date when the Finance Bill, 2019 receives presidential assent.

Goods and Services Tax law

Legislative changes

- For the purpose of computing the threshold of services under Section 10 (1) of Central Goods and Services Tax Act, 2017 (CGST Act), the value of exempt supply of services provided by way of extending deposits, loans or advances (in so far as the consideration is represented by way of interest or discount) shall not be taken into account, for determining the value of turnover in a state or union territory.

- The benefit of composition is not extendable to a casual taxable person or a non-resident taxable person.

- A person not eligible for composition but whose turnover is below INR 5,000,000 (Indian Rupees Five million) may opt to pay in lieu of the tax payable by him, an amount of tax calculated at such rate as may be prescribed, but not exceeding 3%. This option will not be available to persons:

-

- engaged in supplying goods or services which are not leviable to tax under the CGST Act;

- engaged in any inter-state outward supplies of goods or services;

- engaged in supply of goods or services through electronic commerce;

- who are operators required to collect tax at source under Section 52 of the CGST Act;

- engaged in manufacture of such goods or supply of such services as may be notified by the Government on the recommendations of the Council; and

All registered persons having the same Permanent Account Number issued under the Income-tax Act, 1961 must apply to avail of the benefit proposed in the above scheme.

- For the purposes of determining the eligibility of a person under the composition levy scheme, the aggregate turnover of such person:

-

- shall include the value of supplies made by such person from the 1st day of April of a financial year upto the date when he becomes liable for registration under the CGST Act; and

- shall not include the value of exempt supply of services provided by way of extending deposits, loans or advances in so far as the consideration is represented by way of interest or discount.

- For the purposes of determining the tax payable by a person under this section, the expression 'turnover in state or turnover in union territory' shall not include the value of following supplies, namely:

-

- supplies from the 1st day of April of a financial year upto the date when such person becomes liable for registration under the CGST Act; and

- exempt supply of services provided by way of extending deposits, loans or advances in so far as the consideration is represented by way of interest or discount.

- The power to increase the threshold turnover for registration from INR 2,000,000 (Indian Rupees Two million) to INR 4,000,000 (Indian Rupees Four million) in case of suppliers engaged exclusively in the supply of goods has been introduced subject to certain conditions and limitations. For the purpose of this proviso, in case a person is engaged in exempt supply of services of extending deposits, loans or advances (in so far as the consideration is represented by way of interest or discount), the said person shall continue to be considered as an exclusive supplier of goods.

- Provisions relating to usage of Aadhaar as an alternative method of authentication have been prescribed for registration under GST.

- The Government, on the recommendations of the GST Council, has identified a class of registered persons who shall provide prescribed modes of electronic payment to the recipient of supply of goods or services or both made by him. Such recipient of goods and services has been given an option to make payments through the digital modes provided by the supplier. Such digital payments shall be subject to certain conditions as prescribed.

- The provision for filing of quarterly returns by a class of registered persons introduced by the Government on recommendation of the GST Council, has been prescribed. Provisions for making quarterly payments in case of such registered persons have also been prescribed.

- The Commissioner of CGST to be empowered for extending the time limit for furnishing the annual return for a class of registered persons as may be specified. A notification by the Commissioner of state or union territory shall be deemed to be notified by the Commissioner.

- Provision for transfer of any amount of tax, interest, penalty, fee or any other amount available in the electronic cash ledger under the CGST Act to the electronic cash ledger for integrated tax, central tax, state tax, union territory tax or cess, has been created. Such transfer shall be deemed to be a refund from the electronic cash ledger under the CGST Act. The Government is liable to transfer such amounts to state / Union tax account. A similar provision has been introduced under Section 17A of the Integrated Goods and Services Tax Act, 2017.

- Interest to apply only on the amounts paid through electronic cash ledger in cases for which the return for the said period is furnished after the due date in accordance with the provisions of Section 39.of the CGST Act. This benefit shall not be available when such return is furnished after commencement of any proceedings under Section 73 or Section 74 of the CGST Act.

- Section 54 of the CGST Act to empower the Government for disbursing the refund of state tax in the prescribed manner.

- The Commissioner is empowered to extend the time limit for filing of Tax Collected at Source (TCS) return.

- National Appellate Authority for Advance Ruling (NAAAR) to be constituted under Section 101A of the CGST Act. The NAAAR shall consist of the following members:

-

- The President, who has been a Judge of the Supreme Court or is or has been the Chief Justice of a High Court, or is or has been a Judge of a High Court for a period not less than 5 years;

- A Technical Member (Centre) who is or has been a member of Indian Revenue (Customs and Central Excise) Service, Group A, and has completed at least 15 years of service in Group A; and

- A Technical Member (State) who is or has been an officer of the State Government not below the rank of Additional Commissioner of Value Added Tax or the Additional Commissioner of State Tax with at least 3 years of experience in the administration of an existing law or the State Goods and Services Tax Act or in the field of finance and taxation.

Appeal can be filed before the NAAAR when 2 or more states / union territories have provided conflicting decisions. Any person authorized by the Commissioner or applicant being aggrieved by the decision can prefer an appeal. The officers preferring an appeal shall be from the states where advance rulings have been obtained.

An appeal before the NAAAR shall be filed within 30 days further from the date on which the ruling sought to be appealed against, is communicated to the applicants, concerned officers and jurisdictional officers. Such period could be further extended by another 30 days by NAAAR.

- Penalty of 10% of the amount profiteered under Section 171 of the CGST Act has been prescribed. The penalty shall not be payable when the amount determined as profiteered is deposited within 30 days of the date of passing of the order by the authority. Profiteered amount shall mean the amount determined on account of not passing the benefit of reduction in rate of tax on supply of goods or services or both or the benefit of input tax credit to the recipient by way of commensurate reduction in the price of the goods or services or both.

- The legislative changes proposed are to give effect to the notifications and orders issued earlier, basis the GST Council's recommendations.

Tariff Change

The content of this document do not necessarily reflect the views/position of Khaitan & Co but remain solely those of the author(s). For any further queries or follow up please contact Khaitan & Co at legalalerts@khaitanco.com