- within Government, Public Sector, Energy and Natural Resources and Real Estate and Construction topic(s)

- with readers working within the Law Firm industries

The Reserve Bank of India vide its circular No. RBI /2013-14/117 A.P. (DIR Series) Circular No 01, dated 04th July 2013, has issued guidelines pertaining to Foreign Investment in Indian Companies for calculation of foreign investment, transfer of ownership/ control of Indian Company and downstream investment by Indian Companies (hereinafter referred to as the "guidelines/new guidelines"). Major Highlights of the guidelines are discussed hereunder.

APPLICABILITY OF GUIDELINES

The said guidelines are to have a retrospective effect, where all foreign Investment made in Indian companies after 13th February 2009, will fall under the preview of the said guidelines. Any foreign investments made before 13th February 2009, as per then existing guidelines are outside the ambit of new guidelines. The Indian companies shall intimate the RBI within 90 days of this circular (i. e. up to 2nd October 2013), through their Authorized dealer bank, the detailed position on non compliance of issue/ transfer of shares/ downstream investment as per new regulatory framework.

SCOPE OF GUIDELINES

The Guidelines issued by the RBI provides the following:

- Concept of direct and indirect foreign investment;

- Method of calculation of total foreign investment in Indian Companies;

- Guidelines for establishment of Indian Companies;

- Guidelines for transfer of ownership and control of Indian Companies from resident to non-resident;

- Downstream Investment by Indian Companies, which is not owned/ controlled by resident entities;

Further RBI has introduced certain definitions by the said guidelines which are discussed hereunder:

- "Company Owned by resident Indian Citizen": Any Indian Company, in which more than 50% of the capital in the company is beneficially owned by resident Indian Citizen / Indian Companies (i.e., ultimately owned & controlled by Indian Citizens), such company shall be termed as Company Owned by resident Indian Citizen.

- "Company controlled by resident Indian Citizen": Any Indian Company, wherein resident Indian Citizen have the power to appoint majority of directors will be treated as company controlled by resident Indian citizen for the purpose of these guidelines.

- "Company Owned/ Controlled by Non-resident": Any Indian Company, wherein more than 50% beneficial interest in the capital is owned by non -resident shall be termed as Company Owned by Non-resident and the Company, in which, non-residents have power to appoint majority of the directors.

- "Foreign Direct Investment": FDI means investment received by Indian Company from Non-resident entities.

- "Downstream Investment": Downstream Investment means indirect foreign Investment by one Indian Company in another Indian Company either by way of subscription or acquisition.

- "Indirect Foreign Investment":Indirect Foreign Investment means Investment in one Indian Company by another Indian Company, (a) which is having foreign Investment (b) which is not owned/ controlled by resident Indian citizen/ Indian Company owned/ controlled by Resident Indian Citizen, (c) which is owned/ controlled by non residents. However indirect foreign investment in 100% owned subsidiaries of operating- cum investing/ investing companies will be limited to foreign investment in operating- cum investing/ investing companies.

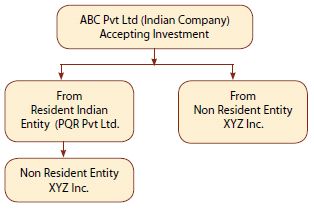

DIFFERENCE BETWEEN DIRECT & INDIRECT FOREIGN INVESTMENT

- Investment by Non- resident Entity directly in Indian Company will be termed as Direct Foreign Investment

- Investment by Non Resident entity through Indian Resident entity owned / controlled by it will be termed as Indirect Foreign Investment.

CALCULATION OF TOTAL FOREIGN INVESTMENT

- Computing of Direct Foreign Investment: All Investment made directly by non-resident entities in Indian Company shall be counted under Direct Foreign Investment.

- Computing of Indirect Foreign Investment: All indirect investment made by investment company in Indian company shall be counted under Indirect Foreign Investment.

Exception: indirect foreign investment in 100% owned subsidiary of operating cum investing/ investing company shall be limited to foreign investment in operating cum investing/ investing company. This exception, is limited to only situations where the entire capital of the downstream subsidiary is owned by the holding company.

Every Indian Company shall ensure compliance with this method of calculation at every stage of investment in the company.

FURTHER OBLIGATIONS

- Indian Company are required to furnish full details of foreign investment/ ownership details/ control over company information to Government of India while seeking approval for accepting foreign investment under approval route.

- Details regarding inter-se agreement between shareholders having effect on change in constitution of Board of Directors and voting rights etc. shall be informed by the Indian Companies operating in sector requiring prior approval of Government for accepting Foreign Investment.

- Indian Company having sectoral cap, shall ensure that balance equity (beyond sectoral cap) shall be beneficially owned in the hands of resident Indian Citizens and Indian Companies owned & controlled by Resident Indian Citizens.

- Companies operating in Information & Broadcasting and

Defence Sector, wherein sectoral cap is less than 49%, shall ensure

that

- The Company shall be owned & controlled by resident Indian citizen and Indian Companies owned & controlled by resident Indian Citizen;

- Largest Indian Shareholder shall hold at least 51% total equity;

- While counting the shareholding of largest equity shareholding, equity holdings of sector banks, Public Financial Institution shall be excluded;

- Here the word largest Indian shareholder means and includes (i) an Indian shareholder, which encompasses (a) his relatives, (b) Company/ Group of companies in which he or his HUF have management & controlling interest and (ii) Indian Company / Group of Indian Companies under same management where Indian Company refers to company in which resident Indian/ his relative/ his HUF jointly or singly holds at least 51% shares.

- Resident Indian shall enter into an agreement to act as single unit for the purpose of satisfying all the conditions of the above clause.

- Where the beneficial interest is held by non resident entity in terms of section 187 of Companies Act, 1956, such investment shall be treated as Foreign Investment.

- Calculation method discussed above shall not apply to Insurance companies.

ESTABLISHMENT OF INDIAN COMPANIES/ TRANSFER OF OWNERSHIP & CONTROL OF INDIAN COMPANIES

Companies operating in sectors/ activities with cap including defence production, air transport services, ground handling services, asset reconstruction companies, private sector banking, broadcasting, commodity exchanges, credit information companies, insurance, print media, telecommunications and satellites are required to obtain prior Government/ FIPB approval in following situation:

- For establishing a company ( not owned/ controlled by a resident entity) in above referred sector with foreign investment;

- For transfer of ownership/ control of said company from resident Indian Citizens/ Company owned & controlled by resident Indian Citizen to non-resident entity through amalgamation/ merger/ demerger/ acquisition etc;

- Companies operating in sector, where 100% foreign investment is allowed under automatic route are excluded from the preview of this clause;

- Following shall be considered for calculating Indirect Foreign

Investment under this clause:

- Downstream investment by Indian Company not owned/ controlled by resident entity;

- Portfolio investment by FII, NRI, QFI as on 31st march of Previous year;

- Investment in Form of Foreign Direct Investment, Foreign Venture Capital Investment, Investment in ADR/ GDR/ FCCB.

DOWNSTREAM INVESTMENT BY INDIAN COMPANY NOT OWNED & CONTROLLED BY RESIDENT ENTITY:

- Indian Company not owned & controlled by resident Entity

shall comply with all relevant entry route sectoral conditions

alongwith following conditions, before making any downstream

investment in another Indian company:

- Indian Company shall intimate Department Of Industrial Policy & Promotion and Foreign Investment Promotion Board within 30 days of such investment

- Downstream investment shall be supported by its board resolution and shareholders agreement, if any.

- It shall comply all applicable SEBI/ RBI guidelines pertaining to issue/ transfer/ pricing/ valuation of shares.

- For making downstream investment, Indian Company shall use the funds brought from abroad.

- Only an Indian investment Company may use the internal funds for making downstream investment, subject to compliance with following conditions:

- It shall obtain prior requisite government/ FIPB approval regardless of amount & extent of foreign investment.

- In addition to this, Core Investment Companies (CIC) shall follow RBI regulatory framework for CICs.

- Prior Government/FIPB approval is required for making foreign investment in Indian Company which does not have any operation or downstream investment and on initiating the downstream investment; it will have to comply with the relevant sectoral condition on entry route, conditionality and caps.

- W.e.f. 31st July 2012, Investment by Banking Company incorporated in India and owned by non-resident entity/ies under corporate Debt Restructuring, or other loan restructuring mechanism, or in trading books, for acquisition of shares due to defaults in loans shall not be counted as Indirect Foreign Investment. However their strategic downstream investment, in their subsidiaries, joint ventures and associates shall be treated as Indirect Foreign Investment.

RESPONSIBILITY FOR COMPLIANCE

At the first instance FDI recipient Indian Company is responsible for ensuring compliance with all applicable FDI rules/ regulations/ guidelines. It shall obtain a certificate from its statutory auditor on annual basis on status of compliance with FDI legal framework and mention the same in its Directors Report in Annual Report. If the auditor has given qualified report, the Company shall immediately intimate Foreign Exchange Department, Regional Office of Reserve Bank of India in whose jurisdiction the Registered office of the Company is located and obtain an acknowledgement from the Regional Office of having intimated it of the qualified auditor report.

CONCLUSION

Adoption of common calculation method in all the sectors can be considered as one of the effective steps taken by the RBI, which has simplified and rationalized the computation process. However, the guidelines, has not discussed the issue of "difference between Foreign Investment & Economic interest of non-resident" and it remains subject to open interpretation.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.