The Commodity Futures Trading Commission ("CFTC") on October 18, 2011 adopted a comprehensive set of rules addressing the incorporation of over-the-counter ("OTC") derivatives into the CFTC's existing position limit regime for exchange-traded futures and options ("Position Limit Rules").1 The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 ("Dodd-Frank Act") both expanded the CFTC's jurisdiction to include surveillance and enforcement authority in the OTC markets and mandated certain regulatory changes to implement that authority. The Position Limit Rules are largely a response to that mandate.

The Commodity Exchange Act directs the CFTC to set limits on trading in the commodity markets to curb "excessive speculation" and ensure the price discovery function of those markets.2 Because most commodities (especially agricultural, metals, and energy commodities) are of finite supply, it is possible that, if one trader controls a significant portion of the market, that trader could cause "sudden or unreasonable fluctuations or unwarranted changes in the price of such commodity"3 which burden the cash commodity markets whose participants use the derivative markets to manage risk. To that end, the CFTC uses position limits to limit the number of positions any trader can hold in a commodity contract for the same delivery period. Position limits also play a role in the CFTC's efforts to prevent manipulation in the commodity markets.

Although the CFTC finalized the Position Limit Rules under Congressional pressure to do so, some of the provisions will not become effective until after the CFTC and Securities and Exchange Commission ("SEC") jointly further define the term "swap" pursuant to Section 721 of the Dodd-Frank Act, which is not expected until late 2011 or early 2012. As discussed below, asset managers that access the commodity markets for their clients will likely be affected by more limited access, higher costs for such access, and nuanced but potentially important changes to rules governing the aggregation of positions in investment funds and separate accounts.

Prior to the finalization of the Position Limit Rules, the aspects of the proposed rule changes that were viewed as most significant and controversial were the imposition for the first time of position limits on OTC trading and the CFTC's plans for dramatic changes to the principles on which the position aggregation regime is based. Importantly, the CFTC was somewhat responsive to industry concerns regarding the proposal to abolish the long-standing regime that has permitted eligible entities (such as mutual funds) to disaggregate positions controlled by independent account controllers. This arguably could have been the most disruptive aspect of the Position Limit Rules for the asset management industry. Even in their final form, the Position Limit Rules remain controversial, garnering only a 3-2 Commissioner vote after several voting delays over a matter of months. The swing voter, retiring Commissioner Michael Dunn, reluctantly voted in favor of adopting the Position Limit Rules, apparently unconvinced the changes would work as intended and concerned that they might lead to adverse outcomes; but rather, he felt compelled to do so by Congress' mandate that the CFTC set such limits.4

This DechertOnPoint discusses four core areas of the rulemaking: (1) position limits on "Referenced Contracts;" (2) position limits and accountability levels on other contracts traded on or through Designated Contract Markets ("DCMs") and Swap Execution Facilities ("SEFs"); (3) aggregation of accounts; and (4) changes to the definition of bona fide hedging for position limit purposes. This update also addresses the implementation of position visibility requirements, the treatment of preexisting positions, and how the CFTC has decided to deal with commodity indexers and exchange-traded funds.

Position Limits on Referenced Contracts

Relevant Contracts

The Position Limit Rules set position limits on futures and options contracts on 28 exchange-traded agricultural, metals, and energy commodities ("Core Referenced Futures Contracts"),5 as well as on certain contracts with prices that are or should be "economically equivalent" to the prices of the Core Referenced Futures Contracts (collectively "Referenced Contracts"). These other contracts, which include OTC contracts such as swaps, are:

- "look-alike" contracts that either settle off a Core Referenced Futures Contract price or are based on the same commodity for the same delivery location as a Core Referenced Futures Contract;

- contracts whose reference price is based only on the combination of (i) at least one Referenced Contract price and (ii) at least one price in the same or substantially the same commodity as the commodity underlying the relevant Core Referenced Futures Contract; and

- inter-commodity spreads with two components, at least one of which is a Referenced Contract.

In choosing to include the above contracts in the definition of Referenced Contracts, the CFTC abandoned its proposal to include contracts based on "substantially the same supply and demand fundamentals" as a metric, which is currently unmeasurable. The CFTC also declined to expand the rule (as some commenters had requested) to include contracts whose prices historically have been correlated to Core Referenced Futures Contracts, as unworkable due to the constantly changing nature of those correlations.

CFTC-Set Position Limits

In general, the actual limits that the Position Limit Rules will set with regard to Referenced Contracts are not yet available, but the formulas that the CFTC will use to set the limits have been provided and are the same formulas the CFTC currently requires DCMs to use in setting position limits on their exchanges. These are:

- Spot month limits will generally be set at 25% of the deliverable supply of each commodity.

- Single month and all-months-combined position limits will equal 10% of the first 25,000 contracts of the average all-months-combined aggregated open interest in such contracts plus 2.5% of all

- contracts of the average all-months-combined aggregated open interest thereafter. The single month position limit and all-months-combined position limit for any given contract will be the same.

- For NYMEX Henry Hub Natural Gas, traders will be able to hold up to five times the position limit in cash-settled contracts so long as the trader's net position is not greater than the position limit.

For all contracts, spot month limits will be applied separately for physical-delivery contracts and cash-settled contracts in the same commodity. Aside from positions in NYMEX Henry Hub Natural Gas, traders generally will not be able to net physical-delivery contracts against cash-settled contracts.

The CFTC will set position limits on a phased-in schedule involving the following steps:

- Initial spot month position limits and non-spot month legacy position limits6 for futures, options and swaps will become effective 60 days after the term "swap" is further jointly defined by the CFTC and SEC. At that time, traders' OTC positions (i.e., economically equivalent positions) will be added to, and counted with, their futures and options positions for spot month position limit purposes.

- Non-spot month non-legacy limits will become effective after the CFTC has gathered one year of swap data to inform its limit-setting.

Importantly, changes to position limits for the legacy Core Referenced Futures Contracts (e.g., futures and options, but not swaps) will become effective by approximately 2011 year-end.7 Swaps will be subject to the same limits 60 days after the term swap is further defined.

The reason for the staggered timing of the implementation of spot month and non-spot month position limits is that spot month limits are based on the "deliverable supply" of a commodity as determined by the DCMs, whereas non-spot month limits are based on "open interest" in contracts on each commodity. Because the CFTC would not have access to information regarding OTC derivative open interest on non-legacy commodities prior to the promulgation of certain rules under the Dodd-Frank Act, it currently does not have enough data to determine such open interest. When the various position limits become effective, traders will be required to comply with the limits on an intra-day (rather than an end-of-day) basis.

DCM- and SEF-Set Position Limits and Accountability Levels

DCMs and SEFs on which Referenced Contracts trade will be required to set position limits on those Referenced Contracts no higher than the CFTC-set limits; and the Position Limit Rules will require DCMs and SEFs to set position limits on other contracts that trade on their exchanges, but not in all months. DCMs will be required to set position limits in the spot month for Referenced Contracts; however, they will be permitted to implement "position accountability levels" in lieu of position limits for physically-settled contracts that are not Referenced Contracts outside of the spot month if the contract is sufficiently liquid. In order to meet that liquidity standard, a contract would need to have an average month-end open interest of 50,000 contracts, an average daily volume of 5,000 contracts, and "a highly liquid cash market."8

Aggregation of Positions

The Position Limit Rules largely maintain the CFTC's long-standing "control," rather than "ownership," standard for the aggregation of positions for position limit purposes, with some notable changes. The aggregation rules have important implications for asset managers due to the often complex nature of their businesses.9

As a general matter, an asset manager is required to aggregate positions over which it maintains direct or indirect ownership or trading control even if those positions are in different accounts. Control is assumed if an asset manager has a 10% or greater ownership or equity interest in an account or fund, subject to an exemption that recognizes that shareholders, limited partners, or other fund investors may have passive ownership stakes in positions that are 10% or greater, but nevertheless do not control the contract trading. In addition, if an "eligible entity"10 delegates trading authority to an independent account controller ("IAC"), it need not aggregate its own positions with those controlled by the IAC.11

The CFTC had originally proposed to abandon the IAC regime, but ultimately left this portion of the rules unchanged, except that the IAC exemption is no longer self-executing. An asset manager desiring to avail itself of the IAC exemption will now be required to file a notice with the CFTC that: (i) will be effective upon filing; (ii) describes the circumstances that warrant disaggregation; and (iii) certifies that the asset manager meets the criteria to qualify for the IAC exemption. If there are other instances outside the IAC exemption for which the sharing of information in order to aggregate positions would cause a violation of the federal securities laws, affected asset managers may file a notice with the CFTC to that effect; however, that notice must be accompanied by an opinion of legal counsel that the information-sharing would cause such a violation. These new claim filing requirements mean that the CFTC will have notice of the identity of asset managers relying on the IAC exemption and can monitor their activities and perhaps review, consider, and/or challenge the bases on which such asset managers disaggregate positions and accounts.

Bona Fide Hedging

The CFTC made changes to what activity qualifies as "bona fide hedging transactions and positions"12 for purposes of determining which traders may exceed position limits when trading Referenced Contracts. For all other purposes, the definition of bona fide hedging will remain the same. Asset managers would rarely be considered to be bona fide hedging when trading in Referenced Contracts because they do not normally participate in the cash commodity markets underlying the derivatives markets. However, the changes will have an indirect effect on trading by asset managers, because of how the Position Limit Rules will affect swap dealers that act as counterparties to OTC derivative contracts. Since the early 1990s, swap dealers have been able to obtain bona fide hedging exemptions to allow them to hedge their exposure to traders with whom they enter into swaps. Under the Position Limit Rules, a swap dealer's position used to lay off swap risk will only be considered a bona fide hedging position if the dealer's counterparty itself would have been considered to be bona fide hedging if it could have entered into the position directly. This change will likely limit the commodity market exposure capacity that swap dealers will have available to provide to their counterparties and customers. DCMs will still be able to grant risk management exemptions in other contracts, such as equity indices.

Miscellaneous

The Position Limit Rules make changes to various other aspects of the CFTC position limit regime which should have a less significant impact on asset managers but are nonetheless worth noting.

Positions in futures, options, and swaps entered into in good faith prior to the effective date of the Position Limit Rules that exceed non-spot month position limits will not be considered in violation of the Rules. However, spot-month limits apply regardless of any preexisting position entered in good faith.

Traders holding futures, options, and economically equivalent OTC positions in energy (except NYMEX Light Sweet Crude Oil and NYMEX Henry Hub Natural Gas) and metals contracts, equal to or greater than 50% of the projected aggregate position limit, will be required to report their positions to the CFTC under the new "position visibility rule." The position visibility levels for NYMEX Light Sweet Crude Oil and NYMEX Henry Hub Natural Gas will be lower. Position visibility reporting requirements will become effective 60 days after the term swap is further defined jointly by the CFTC and SEC.

Although some commenters (including former Senator Blanche Lincoln) requested that the CFTC exempt commodity index funds from the Position Limit Rules, the CFTC declined to treat this class of traders differently from other traders in the market. However, it should be noted that, whereas components of commodity indices may be subject to CFTC-set position limits, commodity index contracts will only be subject to DCM and SEF-set limits. The CFTC plans to study the effects of commodity index fund trading on the commodity markets along with conducting its other Dodd-Frank Act-mandated studies. The CFTC also declined to implement and coordinate with the SEC a position limit policy that would have prevented traders, whose direct exposure to the commodity markets would be otherwise limited, from seeking additional exposure by investing in exchange-traded funds.

Conclusion

Although the Position Limit Rules will not be as disruptive to asset managers' operations as the rule proposals would have been, the Rules will nevertheless have consequences for the industry. Asset managers will need to carefully consider the bases on which they previously relied under the self-executing exemption for disaggregation and will need to make the appropriate exemption filings with the CFTC. To the extent that the counting together of on-exchange and economically equivalent OTC derivatives might cause an asset manager to exceed estimated position limits in certain funds or accounts, planning and possible adjustments will need to occur to ensure compliance when the Position Limit Rules become effective. Asset managers will also need to consider how, and the extent to which, the bona fide hedging exemption changes will affect the capacity of their counterpart swap dealers to provide commodity market exposure, and ultimately the implementation of their own trading strategies. Additionally, asset managers will need to consider appropriate disclosure for the effects of the Position Limit Rules on their activities.

Footnotes

1 Position Limits for Futures and Swaps, 76 Fed. Reg. ___ (___, 2011) (to be codified at 17 C.F.R. pts. 1, 150 and 151) [the "Position Limit Rule Release"]. At the time of publication of this DechertOnPoint, the Position Limit Rules have not yet been published in the Federal Register. This update is based on a copy of the Position Limit Rules, available at http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/federalregister101811c.pdf, and does not reflect any technical amendments that may be made to the Position Limit Rules before official publication.

2 7 U.S.C. § 6a.

3 Id.

4 Michael V. Dunn, Commissioner, CFTC, Opening Statement, Public Meeting on Final Rules Under the Dodd-Frank Act (Oct. 18, 2011), available at http://www.cftc.gov/PressRoom/SpeechesTestimony/dunnstatement101811.

5 ICE U.S. Cocoa, ICE U.S. Coffee C, CBOT Corn, ICE U.S. Cotton No. 2, CME Feeder Cattle, ICE U.S. FCOJ-A, CME Lean Hogs, CME Live Cattle, CME Class III Milk, CBOT Oats, CBOT Rough Rice, CBOT Soybeans, CBOT Soybean Meal, CBOT Soybean Oil, ICE U.S. Sugar No. 11, ICE U.S. Sugar No. 16, CBOT Wheat, MGE Hard Red Spring Wheat, KCBOT Hard Winter Wheat, COMEX Gold, COMEX Silver, COMEX Copper, NYMEX Palladium, NYMEX Platinum, NYMEX Light Sweet Crude Oil, NYMEX New York Harbor No. 2 Heating Oil, NYMEX New York Harbor Gasoline Blendstock, NYMEX Henry Hub Natural Gas.

The CFTC has previously set position limits on futures and options contracts traded on nine enumerated or "legacy" agricultural commodities, leaving it to DCMs to set position limits on, or employ position accountability levels with regard to, other exchange-traded products within CFTC-set parameters. The legacy contracts will now be a sub-set of the Core Referenced Futures Contracts.

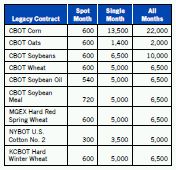

6 "Legacy position limits" refers to non-spot month limits for agricultural contracts currently subject to federal position limits under 17 C.F.R. part 150, as follows:

7

8 Position Limit Rule Release, supra note 1, at 128.

9 17 C.F.R. § 150.4(a)-(b) ("The position limits . . . shall apply to all positions in accounts for which any person by power of attorney or otherwise directly or indirectly holds positions or controls trading or to positions held by two or more persons acting pursuant to an expressed or implied agreement or understanding the same as if the positions were held by, or the trading of the position were done by, a single individual.")

10 17 C.F.R. § 150.1(d). In general, an eligible entity is a commodity pool operator, an operator of a trading vehicle that is excluded from the definition of the term "pool" or who qualifies for an exclusion from the term "commodity pool operator," a limited partner, shareholder, or other fund investor in a commodity pool the operator of which is exempt from registration, a commodity trading advisor, or certain other financial institutions, or affiliates of any of the foregoing entities, that authorizes an IAC (defined below) independently to conduct its commodity trading without day-to-day direction or control by such eligible entity.

11 An IAC generally is a person: (1) who specifically is authorized by an eligible entity independently to control trading decisions on behalf of, but without the day-to-day direction of, such eligible entity; (2) over whose trading the eligible entity maintains only such minimum control as is consistent with such eligible entity's fiduciary responsibilities to fulfill its duty to supervise diligently the trading done on its behalf or as is consistent with such other legal rights or obligations which may be incumbent upon such eligible entity to fulfill; (3) who trades independently of the eligible entity and of any other IAC trading for such eligible entity; (4) who has no knowledge of trading decisions by any other IAC; and (5) who is registered as a futures commission merchant, an introducing broker, a commodity trading advisor, or an associated person of any such registrant, or is a general partner of a commodity pool, the operator of which is exempt from registration.

12 17 C.F.R. § 1.3(z).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.