Stephanie Sanderson, partner at Beesmont Law, breaks down the Common Reporting Standard and explains the impact that the global compliance measure has on captives

The past decade has seen a sharp increase in global compliance measures and international cooperation in tax matters. The Common Reporting Standard (CRS) is a cross border tax information exchange regime, which has been widely adopted and impacts business industries across the globe, including the reinsurance and captive industry. Bermuda continues to be the domicile of choice for this sector and remains at the forefront of international tax transparency.

The Organisation for Economic Co-operation and Development (OECD) created CRS in collaboration with the G20 countries and the EU. Bermuda committed to the early adoption of CRS along with various other jurisdictions, including the UK, with its first exchange of information with participating jurisdictions occurring in September last year.

Bermuda now exchanges CRS information with its international CRS partners automatically on an annual basis. Financial institutions in Bermuda must be compliant with the CRS due diligence and necessary information requirements.

The CRS draws significantly on the US Foreign Account Tax Compliance Act (FATCA) intergovernmental approach and requires regular cross border automatic exchange of information between governments in respect of financial account information reported by financial institutions. The CRS sets out:

- The financial information required to be reported with respect to reportable accounts, including investment income

- The financial institutions that are required to report under the CRS

- Reportable accounts which include accounts held by both individuals and entities as well as 'look through' provisions for passive entities

- Due diligence procedures that must be followed to identify reportable accounts

Although the CRS is similar to FATCA, there are several differences and it is important to assess entities under the separate regimes to ensure the correct classification under each.

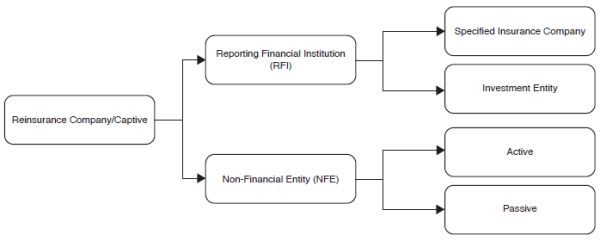

There may be entities that are not Reporting Financial Institutions (RFIs) under FATCA but are RFIs under the CRS. Captives and reinsurance companies will be RFIs under the CRS if they are classified as specified insurance companies or investment entities.

It is important to note that the definition of an 'investment entity' is wider under the CRS than under FATCA and will capture more entities than FATCA. The CRS does not recognise elections made under section 953(d) of the Internal Revenue Code.

Generally, for captives, the following definitions will be relevant in determining the correct classification of an entity under the CRS which largely fall into two categories—'financial institutions' and 'non-financial entities'.

Financial institution

The term 'financial institution' means a custodial institution, a depository institution, an investment entity, or a specified insurance company.

The term 'specified insurance company' means any entity that is an insurance company (or the holding company of an insurance company) that issues, or is obligated to make payments with respect to, a cash value insurance contract or an annuity contract.

The term 'investment entity' means any entity: that primarily conducts as a business one or more of the following activities or operations for or on behalf of a customer: trading in money market instruments (cheques, bills, certificates of deposit, derivatives); foreign exchange; exchange, interest rate and index instruments; transferable securities; or commodity futures trading; individual and collective portfolio management; or otherwise investing, administering, or managing financial assets or money on behalf of other persons.

It can also mean the gross income of which is primarily attributable to investing, reinvesting, or trading in financial assets, if the entity is managed by another entity that is a depository institution, a custodial institution, a specified insurance company, or an investment entity.

The following table may assist with captive entity classification:

Non-financial entity

The term 'non-financial entity' (NFE) means any entity that is not a financial institution. The term 'passive NFE' means any: NFE that is not an active NFE; or an investment entity that is not a participating jurisdiction financial institution.

The term 'active NFE' means any NFE that meets any of the criteria set out in the CRS. The most common type of active NFEs are entities where less than 50 percent of the NFE's gross income for the preceding calendar year is passive income and less than 50 percent of the assets held by the NFE during the preceding calendar year are assets that produce or are held for the production of passive income.

An entity may also be classified as an active NFE if its stock is regularly traded on an established securities market or the NFE is a related entity of an entity that has stock, which is regularly traded on an established securities market.

Understanding classification

Entities should ensure they understand their CRS classification as this will determine whether or not a captive has obligations under the CRS. If so, the RFI must comply with the Bermuda CRS Regulations and Guidance. Bermuda recently updated its regulations to require nil return filings, which means that RFIs in Bermuda must file a return even if there are no reportable accounts for any given reportable period.

Although many captives are NFEs it is important that the proper consideration is given to ensuring the correct classification under the CRS and that any changes are monitored. Financial institutions, such as banks, will require captives to submit self-certifications certifying entity classification and tax status and may impose consequences for failure to cooperate. If a reinsurance company or captive has reporting obligations under the CRS then its directors are responsible for compliance with the relevant laws, and for establishing the correct policies and procedures under the CRS.

Originally published by Captive Insurance Times.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.