THE LUXEMBOURG STOCK EXCHANGE

The Luxembourg Stock Exchange (the "LSE") was set up in 1927 and operates two markets, the regulated market "Bourse de Luxembourg" (hereafter the "Regulated Market") and the alternative market, the "Euro MTF". The Euro MTF market is a multilateral trading facility as defined in the Law of 13 July 2007 implementing Directive 2004/39/EU of 21 April 2004 on markets in financial instruments.

"Some 44,500 tradable securities including 29,250 bonds are currently listed on the LSE. This represents more than 40% of all international bonds listed on European markets. These bonds are denominated in more than 54 currencies and issued by over 3,000 private and public issuers in 100 countries around the world.

Investment funds form another important segment with more than 6,400 separate instruments listed. More than 280 depositary receipts, the majority being GDRs, are also listed on the LSE."1

WHICH ISSUERS CAN LIST THEIR SECURITIES ON THE LSE?

The term "issuer" is defined very broadly by the rules and regulations of the LSE (the "LSE Rules") as "any legal entity that has issued Securities admitted to trading or wishing to proceed to such an admission".

Issuers of securities listed on the LSE include Luxembourg and foreign corporate issuers as well as sovereigns and international institutions.

WHICH TYPES OF SECURITIES MAY BE ADMITTED ON THE LSE?

The LSE Rules provide for the possibility to admit:

- shares of companies and other securities equivalent to shares of companies and partnerships, and share depositary receipts;

- bonds and other debt securities including depositary receipts representing such securities;

- any other security giving the right to buy or sell such securities or with a cash settlement, determined by reference to transferable securities, a currency, a rate of interest or yield, commodities or indices;

- shares and units in undertakings for collective investment;

- money market instruments and all other securities which, subject to Luxembourg law, as the LSE may decide, can be traded on a securities market of the LSE.

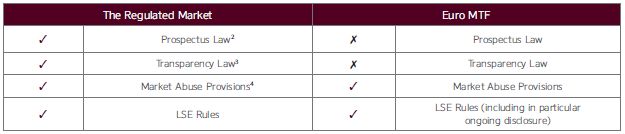

WHICH REGULATIONS APPLY TO WHICH MARKET ?

MAIN DIFFERENCES BETWEEN THE REGULATED MARKET AND THE EURO MTF

- The applicable accounting standards required for the financial statements of issuers to be included in the listing prospectus and to be provided on an ongoing basis: the regulations applicable to the Regulated Market require that the financial statements be prepared in accordance with Regulation (EC) 1606/2002 on international accounting standards as adopted by the EU (IFRS) in case of EEA issuers or in case of third-country issuers, in accordance with accounting standards considered as equivalent5. Issuers listed on the Euro MTF may prepare their financial statements under their national GAAP and IFRS.

- The Euro MTF market is out of scope of the Transparency Law.

- A listing prospectus approved by the LSE in accordance with the LSE Rules for an admission on the Euro MTF does not benefit from the European passport as provided for by the Prospectus Law.

THE LISTING PROSPECTUS

The Regulated Market

- the competent authority for the approval of the listing prospectus is the Commission de Surveillance du Secteur Financier ("CSSF");

- the content requirements for the prospectus are set out in the Prospectus Regulation6;

- the consolidated financial statements of issuers must be drawn up in accordance with IFRS (or equivalent);

- the Prospectus Regulation sets out specific rules regarding the structure of the prospectus and the basic order of the various sections; the Prospectus may be drawn up in English, French or German;

- the prospectus may be used as a public

offer prospectus and for further listings, in the EEA.

2. Euro MTF

- the competent authority for the approval of the listing prospectus is the LSE;

- the content requirements for the prospectus are set out in the relevant schedules of the LSE Rules;

- financial statements can be in IFRS or the national GAAP of the issuer;

- the LSE Rules do not include guidelines regarding a specific structure of the listing prospectus; the prospectus may be drawn up in English, French or German;

- the prospectus may not be used as a public offer document or for further listings in Luxembourg or other jurisdictions.

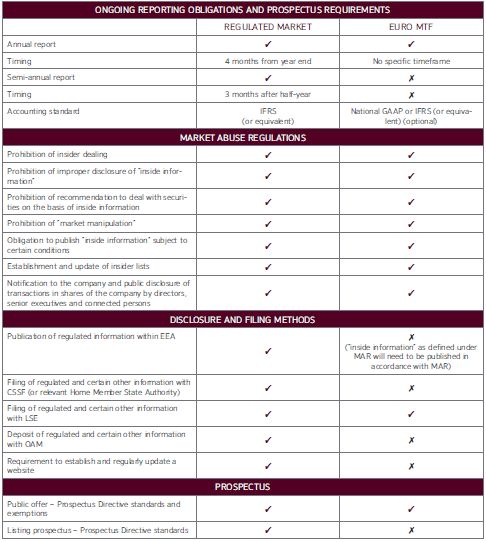

SUMMARY OF THE ONGOING OBLIGATIONS FOR ISSUERS HAVING BONDS LISTED ON THE LSE

1. The Transparency Law

The Transparency Law only applies to the Regulated Market and in summary, provides for the following obligations for an issuer of bonds:

- Periodic financial information:

Issuers are required to publish:

- annual financial reports;

- and semi-annual financial reports.

Certain exemptions may also apply in case the securities have a denomination of at least EUR100.000.

- Publishing without delay any changes in the rights of holders of securities (such as changes in terms and conditions, loan terms or interest rates);

- Ensuring equal treatment of all holders of debt securities ranking pari passu in respect of all the rights attaching to those debt securities.

2. The Market Abuse Provisions

Issuers whose bonds are listed on the Regulated Market or the Euro MTF (or who have requested admittance to any such market) must:

- publish price sensitive inside information as soon as possible (subject to the right with a valid reason and subject to certain conditions to postpone any such publication); and

- keep insider lists.

3. The LSE Rules

The LSE Rules provide for obligations which apply to both the Euro MTF and the Regulated Market. As the Transparency Law does not apply to issuers having bonds listed on the Euro MTF, the LSE Rules include some specific obligations in this respect.

These various obligations under the LSE Rules relate to various notification obligations to the LSE in case of certain securities events and certain publication requirements which are however lighter than the regime applicable pursuant to the Transparency Law.

SUMMARY OF ONGOING REPORTING OBLIGATIONS

(This summary does not include all ongoing reporting obligations which may be applicable and does not take into consideration specific exemptions which may apply in certain cases)

Footnotes

1 The Luxembourg Stock Exchange – Your premium listing destination, Brochure from Luxembourg Stock Exchange and Deloitte as available on the LSE website on 14 January 2014.

2 Law of 10 July 2005 on prospectuses for securities and implementing Directive 2003/71/EC of the European Parliament and of the Council of 4 November 2003 on the prospectus to be published when securities are offered to the public or admitted to trading.

3 Law of 11 January 2008 on transparency requirements in relation to information about issuers whose securities are admitted to trading on a regulated market and transposing Directive 2004/109/EC of the European Parliament and of the Council of 15 December 2004 on the harmonisation of transparency requirements in relation to information about issuers whose securities are admitted to trading on a regulated market and amending Directive 2001/34/EC.

4 Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse ("MAR") and Directive 2014/57/EU of the European Parliament and of the Council of 16 April 2014 on criminal sanctions for market abuse as implemented by the Law of 23 December 2016 (the "Market Abuse Law"and together with MAR, the "Market Abuse Provisions").

5 In this context: In accordance with Regulation 1289, the standards applicable in Japan and in the United States are to be considered as being equivalent to IFRS as from 1 January 2009; In accordance with Delegated Regulation 311, the generally accepted accounting principles of Canada, South Korea and the Republic of China are to be considered as being equivalent to IFRS as from 1 January 2012. Moreover, issuers of third-countries are authorised to draw up their consolidated and semi-annual accounts in accordance with the generally accepted accounting principles of the Republic of India for the financial years starting before 1 January 2015.

6 Regulation (EC) No 809/2004 of 29 April 2004 implementing Directive 2003/71/EC as regards information contained in prospectuses as well as the format, incorporation by reference and publication of such prospectuses and dissemination of advertisements (as amended).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.