EXECUTIVE SUMMARY

Over-the-counter (OTC) derivative markets are subject to significant change as global regulatory commitments originating in 2009 take effect. In Europe, the European Market Infrastructure Regulation (EMIR) requires standardised OTC derivatives to be cleared through central counterparties (CCPs); derivatives which cannot be cleared to be subject to bilateral margining arrangements and a strengthened operational risk framework; and OTC and exchange-traded derivatives (ETDs) to be reported to a trade repository (TR). In addition, the Capital Requirements Directive (CRD IV) and the Capital Requirements Regulation (CRR) increase capital requirements for both cleared and non-cleared OTC derivatives.

The scope of the reform is far reaching and covers the five main asset classes: interest rate, credit, foreign exchange (FX), commodity and equity.1 It is clear that costs will increase as a result of these reforms, but the question is by how much and where the burden will fall. This paper addresses the question of how much more expensive OTC derivative transactions will become as a result of the reforms, and estimates the cost impact of the reform package on transactions in the EU.

The case for these changes is based on the argument that the reforms will increase transparency to the regulator and the market, and reduce risk for market participants. We expect the price for this to be an additional total annual cost of €15.5bn for the OTC derivatives market in the EU. We estimate that the incremental costs for transactions that are subject to the clearing obligation will be around €2.5bn per annum. The estimate for transactions that will not need to be centrally cleared is much higher – totalling €13bn annually.

There are three main elements to the costs that will be incurred by OTC derivatives in future: new margin requirements; new capital charges for exposures; and other compliance costs, mainly resulting from additional reporting requirements. This paper provides estimates for the incremental cost for both cleared and uncleared OTC derivatives for the three cost categories and explores some of the reasons for the differences in costs between cleared and uncleared OTC derivatives. In addition to these increases in costs, the market-making dealers2 may also see revenue fall, e.g. if greater transparency leads to a narrowing of margins.

There are cost implications for all market participants transacting in OTC derivatives: financial counterparties including the market-making dealers; large buy-side customers such as mutual funds, pension funds, hedge funds and insurance companies; and also non-financial counterparties such as industrial companies using OTC derivatives for hedging purposes.

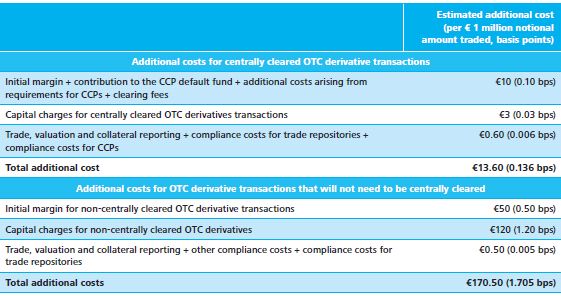

Table 1 – Overview of incremental costs for centrally cleared and non-centrally cleared OTC derivatives transactions

Source: Deloitte calculation based on MAGD (2013), BCBS-IOSCO (2013a), ESMA (2012) and BIS statistics.

The structure of OTC derivative markets is set to change as a result of the reforms. Cost increases will lead dealer banks to review the products they offer and possibly withdraw from certain asset classes which are deemed to be too costly, or look to increase offerings for asset classes where client demand is expected to be greater. This will lead to a shift in the product mix offered by dealer banks and as a result, usage across the market. The increased costs for non-cleared products could move some end-users towards less precise hedges by using cleared/ standardised OTC derivatives in place of a more bespoke (and more expensive) derivative, leaving them with more risk on their own balance sheet.

DATA SOURCES AND METHODOLOGY

A number of studies have attempted to quantify various aspects of the OTC derivative reforms. This paper aims at combining all available quantifications and providing estimates for the average additional costs of the OTC derivatives reform package. The analysis and estimates provided in this paper particularly draw on the following impact assessments, studies and statistics:

|

There are a number of cost factors that we have not considered in the calculation of cost estimates. The reasons for the omission of these factors include the practical challenges of estimating these costs, and uncertainties about the drivers of costs.

Specifically, costs not considered in the estimates provided in this paper are:

|

Table 2 – Assumptions and data sources

To read this Report in full, please click here.

Footnotes

1. Spot FX transactions and certain types of physically settled commodity transactions are excluded from EMIR. In this context, the European Securities and Markets Authority (ESMA) published a letter to the Commission on 14 February 2014, in which ESMA asked the European Commission to clarify 1) the definition of currency derivatives in relation to the frontier between spot and forward and their conclusion for commercial purposes, and 2) the definition of commodity forwards that can be physically settled.

2. The largest derivatives dealers are organised in an industry group referred to as the G15 (G14 until Q3 2011) and account for around five-sixths of the market.

3. Published in the Annex of the Second Consultation Document for Margin requirements for non-centrally cleared derivatives.

4. Contained in Annex VIII of the Final report on draft Regulatory and Implementing Technical Standards on Regulation (EU) 648/2012 on OTC derivatives, central counterparties and trade repositories.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.