UK groups that are either required to or choose to prepare their financial statements in accordance with IFRS have often elected to present the individual company and subsidiary accounts in accordance with UK GAAP.

There are a number of reasons why companies may have chosen UK GAAP in these circumstances. However, many have found that the absence of any available disclosure exemptions in IFRS resulted in a time and cost burden that outweighed the possible savings from using a consistent set of accounting standards across the group.

Recognising that it would be more cost effective if companies only had to maintain accounting records in accordance with one reporting framework, the ASB has proposed disclosure exemptions that will apply to a large proportion of subsidiaries and parent entities.

Under FRED 47 'Reduced disclosure framework' (draft FRS 101), 'qualifying entities' will be able to take certain exemptions from the disclosure requirements contained in EU-adopted IFRS. The definition of a qualifying entity is straightforward, being a member of a group that prepares publicly available financial statements, which give a true and fair view, and in which the entity is consolidated.

The following additional conditions will need to be met before the exemptions can be taken.

- Shareholders in the entity will need to be notified in writing and not object to the exemptions being taken.

- The financial statements must otherwise apply the recognition, measurement and disclosure requirements of IFRS but formats of primary statements will need to comply with the Companies Act 2006.

- The financial statements will need to disclose the relevant standard and paragraph number of the exemptions taken and the name of the parent in which the entity is consolidated together with where the parent's financial statements could be obtained from.

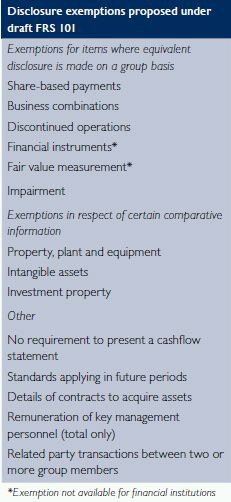

The available exemptions are set out in the table below.

It is currently proposed that the new standard will apply for periods beginning on or after 1 January 2015, with early application permitted for periods that begin on or after the date the final standard is issued.

|

Smith & Williamson commentary We are pleased to see proposals that will make it easier for consistency to be achieved across groups. The option will however still exist for subsidiary and parent accounts to be prepared in accordance with the new Financial Reporting Standard applicable in the UK and Republic of Ireland. The new standard will continue to have some differences from IFRS but will also contain an equivalent reduced disclosure framework. How a company's accounting policies affects tax and distributable profit may still, however, turn out to be the deciding factor in determining which accounting framework to follow rather than the extent and nature of disclosure required. Entities planning to use the proposed exemptions will also have to be mindful of one complicating factor. While the measurement, recognition and disclosure in the financial statements will be in accordance with IFRS, the financial statements will also need to comply with the Companies Act and therefore the primary statement formats required by company law not IAS 1. |

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.