In the first article of this two-part series on sell-side opportunistic engineering in the CDS market, we surveyed a number of strategies that could be used by sellers of CDS protection to create sell-side gains. In this second part, we analyze two recent situations where a proposed refinancing dramatically affected the CDS market for the reference entity because of the reduction in the sell-side risk. Although these cases may or may not have been driven by CDS considerations, they illustrate how sell-side CDS strategies may be effectively implemented.

The McClatchy Refinancing

Background

McClatchy Co. is a publisher of newspapers and online content and owns a number of widely distributed publications across the United States. Through Q1 2018, the company had approximately $800 million in debt outstanding and $1.5 billion in assets, a little under half of which was goodwill. McClatchy has been suffering losses for some time, and a sizable CDS market has developed on its name, reaching almost $500 million of net notional outstanding in March 2018.

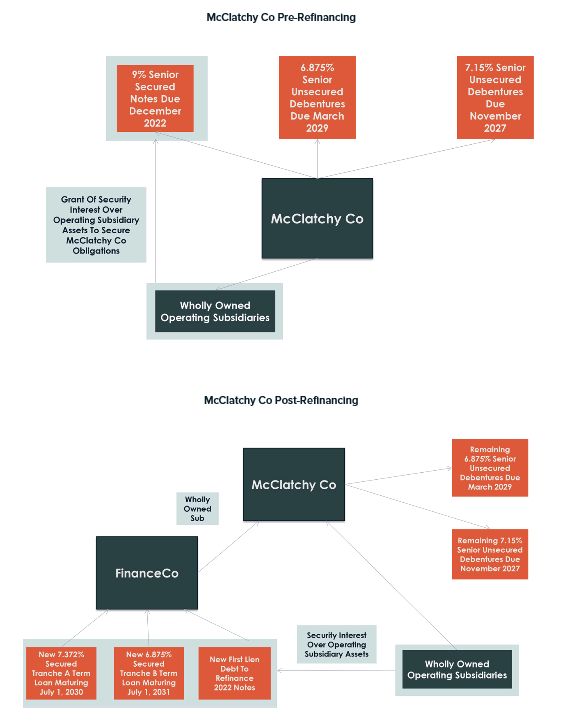

McClatchy's outstanding debt obligations consist of $344 million of 9% secured notes due 2022, $89 million of 7.150% unsecured debentures due 2027 and $276 million of 6.875% unsecured debentures due 2029. The 2027 and 2029 Debentures appear to be held almost entirely by Chatham Asset Management. This circumstance seems to have been factored in by the CDS market, with the result that McClatchy's CDS contracts have been priced more in line with the 2022 Notes. Chatham also appears to be a seller of CDS protection on McClatchy.

On April 26, 2018, McClatchy announced a refinancing sponsored by Chatham in which Chatham would provide McClatchy with $418.5 million in new secured term loans, on the condition that the new financing was incurred at a new entity (New FinanceCo), and the proceeds of the new term loans would be used to repurchase the 2027 and 2029 Debentures held by Chatham. It was also announced that, as a condition to the term loan refinancing, the 2022 Notes would also be refinanced with the issuance by New FinanceCo of new first lien debt.

McClatchy Co Pre-Refinancing

Succession Events and Orphan CDS

There would be no succession event under the proposed McClatchy restructuring, because New FinanceCo would not be assuming debt issued by McClatchy or exchanging its debt for debt issued by McClatchy. Rather, the existing debt at McClatchy Co would be repaid with the proceeds of the New FinanceCo debt. From a practical standpoint, the result is the same either way; the refinancing leaves the McClatchy parent company on a consolidating basis with substantially less debt. But from a CDS perspective, the difference is substantial: (i) the risk of McClatchy defaulting on its own debt would be materially reduced, seemingly resulting in the creation of an orphan CDS; and (ii) the CDS contracts on McClatchy could become difficult to settle due to the relatively small amount of debt remaining at the reference entity.

As the market learned of the proposed refinancing, the CDS spread narrowed dramatically. Almost 70% of the value of protection evaporated in a matter of hours,1 indicating that the market internalized the possibility of an orphan CDS.

Subordination and Deliverable Obligations

The specter of an actual orphan CDS has since dissipated, because, as disclosed in subsequent public filings, McClatchy intends to guarantee the debt issued by New FinanceCo. Under the proposed refinancing, as currently disclosed, McClatchy would guarantee both the New FinanceCo term loans and its new first lien debt, with the former being guaranteed on a subordinated basis. Assuming the remaining debentures at McClatchy Co. are ultimately retired, the subordinated guarantee may very well not be considered a deliverable obligation for purposes of the settlement of the McClatchy Co. CDS contract. However, the guarantee on a senior basis of the New FinanceCo first lien debt should be taken into account for settlement purposes, precluding the creation of an orphan CDS.

Despite the subsequent clarification of the structure of the McClatchy refinancing, the spread for the CDS contracts on McClatchy has not returned to its prior levels. This may be a function of the market's pricing in the subordination of the guarantee of the term loans, which may be fully disregarded for purposes of settling the CDS contracts, and the only remaining deliverable obligation for CDS settlement purposes being the guaranteed new first lien debt. In any event, as a result of the refinancing, Chatham will have a more valuable book of CDS positions. It will also enjoy flexibility to sell out of the new term loans that it is extending to McClatchy without negatively impacting the value of its CDS contracts. For McClatchy, the upside is the ability to slightly de-lever and push out maturities of key obligations by three years without significantly increasing its costs of funding.

It is unclear whether the McClatchy refinancing was designed to impact the CDS market, or whether the impact is an unintended collateral effect. Nonetheless, the interplay of the economics of the refinancing and its effect on the CDS market cannot be overlooked. With or without the orphan CDS, McClatchy appears to be receiving better-than-market refinancing terms in a transaction that seemingly results in a creditor realizing a significant windfall on CDS protection it has sold.

Sears

Background

Sears has been in well-documented financial difficulty for some time. For the past several years, the CDS market has traded on the basis that a default on Sears' debt was almost inevitable.

On April 23, 2018, Sears announced a refinancing proposal from ESL Investments Inc. ESL has been involved with Sears for a number of years both as a significant and even controlling shareholder — it has two seats on the board, one of which is the Sears CEO — and as a creditor.

The proposed refinancing includes (i) a purchase of certain Sears real estate by ESL, and an assumption by ESL of approximately $1.2 billion of the debt secured by that real estate, with Sears continuing to operate its stores under a sale-leaseback arrangement with ESL; (ii) an exchange by ESL of $600 million second lien debt for equity in Sears; and (iii) a purchase by ESL of the Kenmore brand and related business units for $500 million. The proposal requires that the proceeds of the refinancing be used by Sears to tender for certain long-dated unsecured bonds issued by its subsidiary, Sears Roebuck Acceptance Corp., the reference entity for CDS purposes, at a discount to par, reflective of current trading prices.

Bond Rally and CDS Spread

Following the announcement, the unsecured bonds traded up to around 70 cents on the dollar, approximately double the trading price for the bonds prior to the announcement. With the jump in bond prices came the narrowing of CDS spreads. From a CDS perspective, a default appears less likely in the short term, and the cheapest to deliver obligation now trades at a far smaller discount to par.

Whether the ESL proposal will materially change the credit outlook for the retailer struggling with cash flow issues remains to be seen. But in the short term, the proposal has resulted in a significant price swing that favors CDS protection sellers. If the tender offer is consummated and the unsecured bonds are retired, the market for Sears CDS should remain, at least for some time, in its now seller-friendly state.

As with McClatchy, the impact on the CDS market may not be a motivating factor in the Sears refinancing. However, the Sears situation illustrates how a sponsor that is long the reference entity via CDS protection may be incentivized to make certain arrangements with a reference entity that favor its CDS positions. CDS protection buyers should therefore be wary of reference entities in which investors both have substantial degrees of control or influence and have also sold significant CDS protection.

State of the Market

The McClatchy and Sears cases provide road maps for opportunistic strategies available to CDS protection sellers as a counterweight to the strategies available to CDS protection buyers. By moving the price of the cheapest to deliver obligation and driving the probability of default, both CDS protection buyers and sellers can generate substantial gains on their CDS investments, using a portion of the economic benefits to incentivize the cooperation of the reference entities. One can envision a situation in which the CDS protection buyers and sellers compete with CDS strategies on a reference entity, with the prevailing party being the one that can generate economics justifying the better financing package for the issuer.

As discussed in prior articles Hovnanian, questions have been raised regarding the viability of the CDS product if these opportunistic strategies were to proliferate. Both ISDA and the CFTC have stated that they are looking into such strategies and how they comport with existing rules and regulations.

It remains unclear whether the market has an appetite for changes or, indeed, whether the regulators can get ahead of sophisticated market participants and their creative strategies without undermining the utility of the product they are trying to protect. Also, the market has now likely come to the realization that CDS is not an arena reserved for parties hedging commercial relationships or taking passive investment exposure. It is clearly also frequented by investors actively using CDS as well as other investment products such as equity and debt securities to achieve specific outcomes with respect to their holdings in a particular reference entity. In that worldview, both regulators and participants may have to contend for the foreseeable future with the presence of peer activism in the CDS market.

Footnote

1 5yr CDS Spread: 4/26/2018: 903, 4/30/2018: 360, 5/30/2018: 385.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.