On April 12, 2018, the Securities and Exchange Commission (SEC) issued a risk alert outlining certain compliance issues identified by the regulator's Office of Compliance Inspections and Examinations (OCIE) related to advisory fee and expense compliance.

The issues detailed in the alert were those most frequently identified by OCIE in deficiency letters sent to SEC-registered investment advisers as part of its examination program. By highlighting the most commonly encountered shortcomings, OCIE encouraged advisers to review their practices, policies and procedures to ensure compliance with their advisory agreements and representations to clients regarding fees and expenses made in Form ADV and other disclosures. Further, OCIE reminded advisers that failing to do so may violate the Investment Advisers Act of 1940 (the Advisers Act) and related rules, including its anti-fraud provisions.

View PDF version here.

Most Frequent Compliance Issues

The most frequently identified deficiencies related to advisory fees and expenses include:

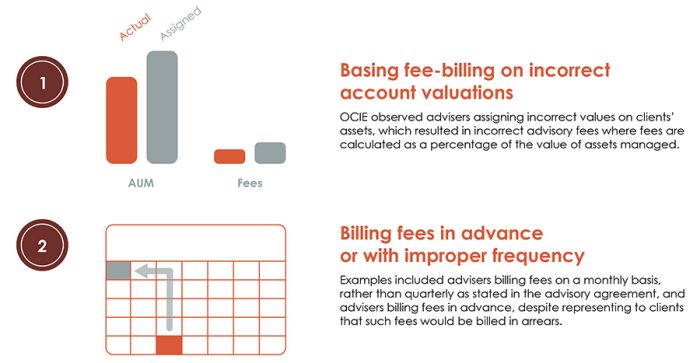

- Fee-Billing Based on

Incorrect Account Valuations – OCIE observed

advisers assigning incorrect values on clients' assets, which

resulted in incorrect advisory fees in instances where fees are

calculated as a percentage of the value of assets managed. This has

included miscalculating assets by using a different metric or

process than that described in the client's advisory

agreement.

- Billing Fees in Advance or

With Improper Frequency – Among the examples

observed by OCIE staff were advisers billing fees on a monthly

basis, rather than the quarterly basis stated in the advisory

agreement or in Form ADV Part 2; advisers billing advisory fees in

advance, despite representing to clients they would be billed in

arrears; advisers billing a new client in advance for an entire

billing cycle, instead of prorating fees for advisory services that

began mid-billing cycle; and advisers failing to reimburse to a

client a prorated portion of their advisory fees when the client

terminated the advisory services mid-billing cycle, despite

disclosing that they would do so in Form ADV Part 2.

- Applying Incorrect Fee

Rate – Advisers were observed, for example, applying

a rate higher than what was outlined in the advisory agreement,

double-billing clients or charging a nonqualified client a

performance fee based on a percentage of their capital gains

inconsistent with Section 205(a)(1) of the Advisers Act.

- Omitting Rebates and

Incorrectly Applying Discounts – OCIE staff

observed advisers failing to apply rebates or discounts as

specified in advisory agreements, including not combining account

values for clients in the same household, when doing so would have

resulted in discounted fees; failing to reduce a client's fee

when their account reached a specified threshold that should have

resulted in a lower fee; and charging additional fees, such as

brokerage fees, to wrap fee program clients who qualified for the

program's bundled fee.

- Disclosure Issues Involving

Advisory Fees – For example, certain advisers'

actual practices were inconsistent with those outlined in their

Form ADV disclosures, such as charging an advisory fee rate higher

than the disclosed maximum rate or not disclosing certain fees or

markups in addition to their advisory fees, such as those from

third-party execution and clearing services.

- Adviser Expense Misallocations – Certain advisers to private and registered funds were observed misallocating expenses to the funds they advise, including allocating distribution and marketing expenses, regulatory filing fees, and travel expenses to clients instead of the adviser, in contradiction of the advisory agreement, operating agreements or other disclosures.

How to Respond

In response to these observations, OCIE staff reported that some advisers elected to "change their practices, enhance policies and procedures, and reimburse clients by the overbilled amount of advisory fees and expenses," while others "proactively reimbursed clients for incorrect fees and expenses that they identified through the implementation of policies and procedures that provided for periodic internal testing of billing practices." All advisers should take the opportunity to reassess their own advisory fee and expense practices and related disclosures to confirm their compliance with the Advisers Act and all related rules and responsibilities, and also review the adequacy and effectiveness of their compliance programs.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.