Introduction

If private equity and other investors were not aware of the power of the secretive Committee on Foreign Investment in the United States (CFIUS, or the Committee), its decision to reach out and quash the potential Broadcom-Qualcomm transaction brought the message home with force.

The decision of the Trump Administration to use CFIUS as a vehicle to halt what would have been the largest tech acquisition of all time is the latest reminder of the considerable power of the President to shape foreign investment in the United States. With President Trump now having rejected three high-profile transactions (all with connections to or concerns related to China), plus reportedly having rejected or substantially curtailed through mitigating measures as many as a dozen others behind the scenes, it is apparent that President Trump's hardline economic team has engineered a marked change in the historic open-investment stance of the U.S. Government. With the National Security Strategy reports labeling China as a "strategic competitor," and with Commerce Secretary promising that there will be further "limitations on foreign investment" – i.e., restrictions on investments by China, the fastest-growing source of investment funds for U.S. transactions – investors in U.S. firms need to take into account potential national security concerns both when investing and establishing their exit strategies.

The Committee's recommendation was unique in that there was no formal joint filing by parties to the transaction requesting CFIUS review. Instead, CFIUS took the unusual step of responding to a unilateral request for review by Qualcomm, thus reaching into a deal that was not even formally before it. This unprecedented use of the CFIUS process provides further proof that the Trump Administration is willing to use all the tools at its disposal to aggressively scrutinize foreign investment into the United States.

This Client Alert provides an overview of the new investment landscape. First, given that CFIUS is the main current hurdle for foreign investment into the United States, it provides an overview of how the CFIUS process functions. Second, it explores the implications of the unusual pre-filing use of CFIUS to block the Broadcom-Qualcomm transaction. Third, it details the ways in which CFIUS has become more aggressive in the new administration and how this trend is likely to continue. Finally, it concludes with a checklist of the types of deals that should strongly consider CFIUS filings as well as some final thoughts regarding the implications of the more aggressive hostility of the Trump Administration to foreign direct investment in the United States, particularly where there is a China connection.

How Does CFIUS Function?

Although post-WWII U.S. policy has been to maintain an open posture for foreign investment, the Exon-Florio amendment in 1988 created CFIUS, which provided a mechanism to scrutinize foreign investments and acquisitions to determine if they have national security implications. After a controversy regarding the proposed acquisition of the commercial operations of six ports by Dubai Ports World, the Foreign Investment and National Security Act of 2007 (FINSA) increased the scope of transactions subject to potential CFIUS review by adding critical infrastructure investments.

The Exon-Florio provision, as amended, gives the Committee the right to review proposed foreign "mergers, acquisition, or takeovers" and to present recommendations regarding whether they should be approved by the President, who has the authority to block proposed foreign transactions that threaten to impair the U.S. national security. CFIUS functions as an interagency committee to review the national security implications of foreign investments in U.S. companies or assets. As per Executive Order 13,456 (issued by President George W. Bush), the Committee consists of nine members, including the Secretaries of Commerce, Defense, Energy, Homeland Security, State, and Treasury; the Attorney General; the U.S. Trade Representative; and the Director of the Office of Science and Technology Policy. The Secretary of Labor and the Director of National Intelligence also serve as ex officio members. The Committee completes its review based upon jointly provided information regarding the proposed transaction, with the information provided in response to a lengthy set of questions as outlined in Section 800.402 and other parts of the CFIUS regulations.

CFIUS filings are voluntary in nature. Parties go to the time and expense of seeking Committee review because, if a voluntary filing is made and the Committee approves it, then the U.S. government loses the ability to challenge a transaction, unwind it, or require mitigating actions. By contrast, any acquisition not reviewed is subject to pestment or other actions designed to address any national security threat inherent in the transaction. Through this carrot and avoidance of a potential stick strategy, parties to M&A activity are encouraged to self-evaluate transactions involving the potential transfer of ownership or control to a foreign person and to seek a voluntary review where national security concerns potentially arise.

CFIUS filings consist of responses to a series of set questions as well as follow-up questions from the Committee. The current list of factors considered by the Committee is established by statute and consists of the following:

- Whether the transaction impacts the domestic production needed for national defense requirements;

- Whether the transaction impacts the capability and capacity of domestic industries to meet national defense requirements;

- Whether the transaction relates to the control of domestic industries and commercial activity by non-U.S. citizens as it relates to national security;

- The potential effect on sales of military goods, equipment, or technology to a country that supports terrorism, proliferates missile technology or chemical/biological weapons, or where there is an identification by the Secretary of Defense that the transaction poses "a regional military threat" to U.S. interests;

- Whether the transaction could impact U.S. technological leadership in areas affecting U.S. national security;

- Whether the transaction has a security-related impact on critical U.S. infrastructure;

- The potential effects on U.S. critical infrastructure, including major energy assets;

- The potential effects on U.S. critical technologies;

- Whether the transaction is a foreign government-controlled transaction;

- In cases involving a government-controlled transaction, additional review of the adherence of the country to nonproliferation control regimes, the foreign country's record on cooperating in counter-terrorism efforts, the potential for transshipment or persion of technologies with military applications, and future U.S. requirements for sources of energy and other critical resources; and

- Such other factors as the President or the Committee determine to be appropriate.

The manner in which these factors are applied in any specific transaction is entirely within the discretion of the Committee. In particular, the view of what constitutes a national security issue is amorphous, allowing for the expansion of review to areas of concern not traditionally covered in prior reviewed transactions.

On November 8, 2017, a bipartisan bill, the Foreign Investment Risk Review Modernization Act (FIRRMA), was proposed in the U.S. Senate to "modernize and strengthen the process by which [CFIUS] reviews acquisitions, mergers and other foreign investments in the United States for national security risks." FIRRMA would expand CFIUS' jurisdiction to include acquisitions of minority interests, certain IP arrangements, and real estate transactions. Notably, the bill would allow CFIUS to charge a filing fee of up to the lesser of 1% of the transaction value and $300,000.

Given the increased focus on foreign investment and bipartisan support in Congress for greater scrutiny of foreign investment (particularly from China), Congress is likely to pass some variant of FIRRMA. The actions of the Committee in dealing with the proposed Qualcomm-Broadcom transaction, however, illustrates that even absent a more robust governing statute, the U.S. government has the tools available to it to reach into any deal with a potential national security angle.

What are the Implications of the CFIUS Rejection of the Qualcomm-Broadcom Transaction?

Qualcomm is a developer of technologies and products used in mobile devices and other wireless products, including network equipment. Qualcomm has been involved in developing digital communications technologies relating to 2G Code Pision Multiple Access (CDMA), Wideband CDMA for 3G, and Orthoganal Frequency Pision Multiple Access 4GE LTE mobile networks. Qualcomm is now involved in the next generation of wireless communication, the 5G standards that are expected to become the wireless norm in the next few years and enable the widespread adoption of the Internet of Things, which will require vastly increased wireless bandwidth.

Qualcomm's competitor Broadcom is co-headquartered in Singapore and San Jose, California. Broadcom was formerly known as Avago Technologies but changed its name after acquiring U.S. Irvine-based chipmaker Broadcom Corporation in 2016. For several months prior to the CFIUS' disposition of the transaction, Broadcom sought to continue its expansion in the U.S. market. If Broadcom's $117 billion bid had been accepted, it would have been the largest merger in the tech industry to date.

On January 29, Qualcomm filed a unilateral notice with CFIUS seeking review of Broadcom's solicitation of proxies to vote on six director nominees, representing a majority of Qualcomm's 11-member Board. In the course of CFIUS' subsequent correspondence with Qualcomm and Broadcom (which included letters to CFIUS submitted by Broadcom on February 21 and March 2), the Committee took the position that that Broadcom's takeover attempt, including the related stock purchase, proxy contest for the election of six directors to Qualcomm's Board, the Proposed Agreement and Plan of Merger, and any other potential merger between the two entities could pose national security concerns.

On March 4, CFIUS issued an agency notice under 31 C.F.R. § 800.401(c) that broadened the scope of its review to cover the proposed takeover of Qualcomm. That same day, CFIUS issued an interim order directing Qualcomm to postpone its annual stockholders meeting and election of directors by 30 days. The delay was unusual, as CFIUS has not usually initiated an investigation before parties to a foreign acquisition have agreed to a plan of merger.

On March 5, CFIUS recommended that the Trump Administration block Broadcom's proposed plan of merger or any other potential merger between the two entities. CFIUS cited Qualcomm's expertise in the semiconductor industry, significant R&D expenditures, and role as a supplier of products to the U.S. government, particularly Department of Defense national security programs. Despite the fact that Broadcom is a Singapore-based company that is in the process of moving its headquarters to the United States, CFIUS expressed concerns over the possibility that the merger could create opportunities for Chinese competitors, in particular Huawei Technologies Co., Ltd. (Huawei):

[A] weakening of Qualcomm's position would leave an opening for China to expand its influence on the 5G standard-setting process. Chinese companies, including Huawei, have increased their engagement in 5G standardization working groups as part of their efforts to build out a 5G technology. While the United States remains dominant in the standards-setting space currently, China would likely compete robustly to fill any void left by Qualcomm as a result of this hostile takeover.

In its recommendation, CFIUS also noted that Broadcom's acquisition could impair Qualcomm's long-term technological competitiveness, citing statements by Broadcom that it would take a "private equity-style direction" upon acquiring Qualcomm, which, according to CFIUS, "means reducing long-term investment, such as R&D, and focusing on short term profitability." CFIUS additionally made reference to the post-acquisition performance of Broadcom's other foreign subsidiaries and noted that the company had secured a record $106 billion of debt financing to support the anticipated Qualcomm acquisition.

This is an important inflection point for CFIUS and has important implications for participants in cross-border private equity transactions. Prior rejections by CFIUS have focused on the particulars of the transaction, particularly the nationality of the acquiring company. Here, the rejection was stated as being based upon economic reasons unrelated to nationality – the potential starving of Qualcomm's ability to invest in R&D. Nationality only came into play on a secondary basis, due to the potential of the transaction to indirectly lead China-based Huawei to leapfrog its way to the forefront of the next generation of wireless technology.

On March 12, President Trump issued an Executive Order adopting the CFIUS recommendations, which, among other things: (1) prohibited the proposed takeover of Qualcomm; (2) blocked Broadcom's 15 potential candidates for director positions; and (3) required written certification of compliance with the order on weekly basis from both parties, including a description of efforts to permanently abandon the proposed takeover attempt.

CFIUS' unprecedented recommendation and the Trump Administration's intervention in a proposed transaction that was not even formally before it spurred fears in the private equity industry of future governmental interference and coincided with generally poor stock market performance in the first quarter, which was influenced heavily by the general and aggressive trade actions begun by the Trump Administration. Qualcomm's stock price immediately dropped by $2.94 (4.7%). Broadcom's stock, which had risen by more than 3%, later fell 4 cents to $262. 0.

The overall impact of the CFIUS disposition of the deal is not yet determined. The first quarter of 2018 represented a sharp increase in international M&A activity. With much of the activity occurring in high-tech areas, the high-profile rejection of what would have been the largest-ever tech merger will likely influence investment and exit strategies for any transaction that presents a potential national security angle.

How is CFIUS Becoming More Aggressive?

It is important to note that the aggressive use of CFIUS is only a part of the efforts of the Trump Administration to re-order the international trade environment, particularly where China is concerned. In just this year alone, the Trump Administration has announced new tariffs on steel and aluminum imports under Section 232 of the Trade Expansion Act of 1962 (which were widely viewed as being a response to Chinese overcapacity in these industries), special tariffs against solar panels and washing machines from China, $50 billion in Section 301 tariffs to combat perceived unfair Chinese trade practices related to U.S. intellectual property, and a 50% increase in antidumping and countervailing duty actions, with the majority being aimed at Chinese exports.

In this context, the use of CFIUS to target Chinese investments into critical U.S. industries is not surprising. Although reviews can arise for any country, in recent years China has been the prime source of CFIUS filings, with other countries (such as the United Kingdom, Canada, Japan, France, Germany, Switzerland, The Netherlands, Singapore, Israel, and South Korea) also being significant.1 Because Chinese investors are aware that the new administration has heightened concerns about Chinese access to U.S. intellectual property and manufacturing know-how, China-related deals are especially like to seek CFIUS review.

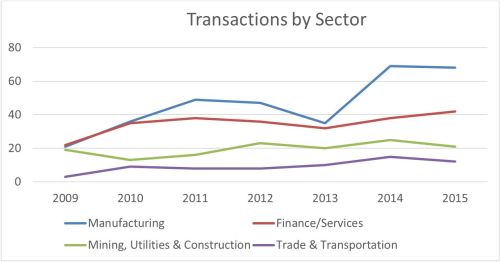

CFIUS activity has been on the rise in recent years, as shown by this chart showing the last full year of fully released statistics. Aggregate statistics released for 2017 show that the Committee accepted nearly 250 submitted cases in 2017 – an increase of nearly 40% over 2016's previous high of 172 cases. (Historically the number of cases has fluctuated between 100 and 120 cases.) The vast bulk of CFIUS filings occur in four sectors that have proven to be of interest to Chinese investors: (1) manufacturing; (2) finance, information, and services; (3) mining, utilities, and construction; and (4) wholesale and retail trade.2

The Obama Administration generally had a hands-off CFIUS approach. As a result, only two transactions were halted or required significant pestments by President Obama (for Aixtron, a semiconductor company, and for Ralls Corp., which was required to pest windfarm assets located near a defense facility). The transactions cleared included controversial transactions, such as the Smithfield Foods acquisition by China's Shuanghui International Holdings Ltd., which raised concerns about a Chinese company taking over 26% of the U.S. hog market and food-processing facilities in more than a dozen states, key U.S. food-processing technology, and Smithfield intellectual property.3 Certain other transactions were abandoned by the parties due to opposition at the Committee level.

By contrast, the Trump Administration has intervened directly at CFIUS' request to block three attempted acquisitions of American firms within a bit more than a year. In addition to the Qualcomm takeover, the White House halted a potential $1.3 billion acquisition of U.S. chipmaker Lattice Semiconductor Corporation by Canyon Bridge Partners, due to connections to China through a Chinese investment vehicle. CFIUS also halted the proposed sale of MoneyGram to China's Ant Financial due to concerns about Chinese interests gaining access to confidential details regarding U.S. persons who transmit money.

In addition to these outright rejections, it has become increasingly common for CFIUS to only approve deals after putting in place mitigating measures or seeking additional information, such as occurred where it put on hold investments by Chinese conglomerate HNA into SkyBridge Capital and miner Glencore until the purchaser provided full disclosure of its share structure. This is a trend that began in the Obama administration but that has accelerated in the new administration. Mitigating measures can include such conditions as restricting which persons can access certain technologies/information, establishing procedures regarding U.S. government contracting, establishing corporate security committees to oversee classified or export-controlled products or technical data, requiring pestments of critical business units, providing periodic monitoring reports to the U.S. government regarding national security issues, or giving the U.S. government the right to review future business decisions that implicate national security.4

The increasing prevalence of mitigating measures, as well as the increased staff time required to monitor the implementation of mitigating measures, is one of the key reasons why increased staffing and resources for the Committee process is a priority under the Trump Administration. The fact that the staff is overburdened is shown by the increasing delays in processing filings. It is also why the pending CFIUS amendments in Congress would fund increased staff.

How are CFIUS Reviews Changing at the Executive Level?

There are a number of ways in which CFIUS reviews appear to have changed at the executive level, based upon the publicly announced outcomes over the first fifteen months of the Trump Administration:

- Appointment of New Members with Heightened National Security Concerns. The Committee is an inter-agency committee composed of key secretaries and other actors, such as the Attorney General, that bring expertise and institutional knowledge regarding national security issues. The appointment of new actors to these positions appears to have led to new Committee members who are less receptive to foreign investment than the more accommodating Obama appointees.

- Tightening Discretionary Reviews. Because the CFIUS process is subject to a high degree of discretion and confidentiality, there is considerable leeway to change the way in which transactions are reviewed. Although there has been no formal expansion of the parameters of review, such as occurred with Executive Order 13,456 (issued by President George W. Bush), which altered the scope of CFIUS reviews in the aftermath of the FINSA passage,5 it appears that the hill has gotten steeper for foreign purchasers, particularly from China.

- Direction and Control from President Trump. The CFIUS statute, as amended, lays out a concrete role for the President only at the end of the process. Nonetheless, given the high degree of confidentiality of the process and the interest of President Trump in national security matters, the President has been in a position to exert influence on high-profile matters as they arise.

- Increasing Scrutiny of China and the Potential Impact of Transactions on Competition with China. The CFIUS review process increasingly is the mechanism through which Chinese M&A activity is vetted, with Chinese companies having overtaken UK companies several years ago as the largest source of CFIUS requests.6 The rejection of certain high-profile transactions, such as the proposed acquisition of MoneyGram by the Chinese company Ant Financial, supports the theme of increasing skepticism regarding Chinese acquisitions. Further, the fact that the perceived national security issue for Broadcom-Qualcomm was based on anticipated and speculative impacts of the deal on future R&D efforts illustrates how far the administration is willing to push the concept of a national security interest.

- Increasing Scrutiny of State Actors. For the last few years, there have been concerns that state-owned entities may be using their foreign commercial enterprises to advance the home country's political agenda. This issue arises not only with regard to Chinese companies but also with other countries where there are company ties to the government (including for countries where the ties may not be known publicly). The proposed legislation in Congress would explicitly allow further probing into ownership to determine the potential national security impact of state ownership.

- Increasing Scrutiny of Sectors of Concern. Certain sectors are viewed as presenting opportunities for foreign governments to treat U.S. acquisitions as supporting foreign policy initiatives or other activities inimical to U.S. interests. For example, acquisitions by Chinese telecom companies have been viewed as problematic due to the risk of potential electronic eavesdropping.7 Both the Obama and Trump Administrations have blocked significant semiconductor transactions.

As shown by the Broadcom-Qualcomm transaction, the definition of what type of industry is considered to be of national security importance – and the impact of indirect impacts on national security – is malleable. If the administration is able to take secondary considerations into account, like whether the transaction will hobble the company with an increased debt load, then the range of ways to block industries will grow.

FINSA added "critical industries" and "homeland security" as categories of economic security subject to a CFIUS review. "Critical infrastructure" is a concept that allows for ready expansion of the scope of review. Although not directly part of the CFIUS authorization, the USA PATRIOT Act of 2001 (Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism)8 provides that the term "critical infrastructure" includes "systems and assets, whether physical or virtual, so vital to the United States that the incapacity or destruction of such systems and assets would have a debilitating impact on security, national economic security, national public health or safety, or any combination of those matters." Sectors identified as potentially meeting this definition include telecommunications, energy, financial services, water, transportation sectors,9 and the "cyber and physical infrastructure services critical to maintaining the national defense, continuity of government, economic prosperity, and quality of life in the United States."10

What Types of M&A Activity are Most Likely to Trigger a Need for a CFIUS Filing?

The type of transactions that will merit consideration of filing for a CFIUS review are in flux, for all the reasons noted above. Nonetheless, there are certain recurring situations that likely will merit serious consideration of a CFIUS filing. These include sales with the following attributes:

- U.S. interests that produce, sell, or broker goods or technical data controlled under the ITAR (U.S. Munitions List products or goods modified to meet military specifications or for military use);

- U.S. interests that produce, sell, or broker goods or technical data controlled under the Export Administration Regulations, especially if 600-series (commercial military) goods are involved;

- U.S. interests that produce, sell, or broker goods or technical data controlled under the nuclear-related export controls;

- U.S. entities that possess a classified facility or some form of top-secret clearance;

- U.S. interests that have significant sales to federal or state governments;

- U.S. interests in sectors of key concern, such as telecommunications, agriculture, food, high-technology, bio-technology, energy, critical infrastructure, semiconductor, software, or pharmaceutical products;

- U.S. interests that possess key intellectual property that is not generally available worldwide;

- U.S. interests that manufacture products where there are few competitors in either the United States or abroad, such that the sale would arguably move control of a limited-supply product to sole foreign control;

- U.S. interests that have property close to U.S. military or other critical national security assets;

- U.S. interests that are part of the defense or police supply sectors;

- U.S. interests that have access to confidential information about U.S. persons (health, financial, etc.); and

- Purchasers from problematic trading partners, especially China.

What are the Implications for Companies Selling to Foreign Interests, Looking Ahead to Exit Strategies, and for Foreign Buyers?

While the contours of how CFIUS reviews will change is still developing, the prospect of change is a self-fulfilling prophecy. As more deals are rejected, filings will increase. High-profile rejections of Chinese investments are leading to a greater willingness of Chinese investors to make protective filings. The Qualcomm decision may encourage other company managements facing a hostile takeover to unilaterally turn to CFIUS for relief. As filings rise, CFIUS acquires increased clout and prominence as a de facto gatekeeper to foreign investments in the United States where there are arguable national security interests in play.

The increasing activism of CFIUS means that there is likely to be a brake on China-linked investors investing in the United States, particularly for energy, high-tech, pharmaceutical and bio-pharma, semiconductor, telecommunications, and other critical industries. But beyond this obvious impact, the elimination of a major source of investment funds will impact the pool of buyers for these types of companies, potentially driving down selling prices. Further, due to uncertainty regarding how far the Committee will extend its reach, even companies close to the periphery of national security concerns may see concerns about sales to Chinese investors.

The Broadcom-Qualcomm rejection also illustrates that potential investors and sellers need to take an expansive view of what constitutes a national security interest, taking into account factors beyond the identity of the purchaser and its nationality. Indirect national security interests, potential upsetting of the competitive balance in favor of non-U.S. companies, and other factors not traditionally evaluated by CFIUS practitioners now are moving to the forefront.

U.S. companies looking to sell to foreign interests, or foreign interests looking to purchase U.S. companies or assets, should closely consider the potential national or economic security aspects of their transactions, with the level of concern and likelihood of seeking a CFIUS review rising as the country of acquisition moves away from the relative safe haven of NATO and similar-level countries. National security needs to be viewed in the broadest possible context.

Also of concern to PE investors is that CFIUS seemed most concerned that the purchaser planned to apply a "private equity focus" to running the combined entity after the deal. What the Committee is clearly telegraphing is its hostility to plans to run a post-review company with financial discipline – at least where critical infrastructure or other types of capital-intensive national security interests are concerned. This suggests a potential hostility to the basic PE model. Potential investors into U.S. companies where there are arguable national security interests need to take this new-found focus on secondary effects into account, not only in determining where and how they will invest in such companies but also in terms of how they might publicly describe their post-transaction plans.

One thing is clear: The CFIUS process is changing to a large degree. Prudent companies will not want to be on the wrong side of the evolving standards for CFIUS clearance. Private equity investors, in particular, need to pay attention to potential CFIUS concerns not only at the time of exiting from deals but at the investment stage at well. Companies that were counting on potential exit strategies involving Chinese investors need to take into account the potential extra scrutiny that such sales might attract. The premiums that some Chinese companies have been willing to pay to get access to U.S. intellectual property and advanced manufacturing know-how are increasingly at risk. Prudent investors need to take this into account at all stages of investment.

Footnotes

1 Id. at 27.

2 See James K. Jackson, Cong. Research Serv., RL33388, Comm. on Foreign Inv. in the U.S. (CFIUS) (2016) at 25-26, https://fas.org/sgp/crs/natsec/RL33388.pdf.

3 Id. at 12.

4 See Cong. Research Serv., RL33388 (2016) at 27-28.

5 See Exec. Order No. 13456, Further Amendment of Exec. Order No. 11858 Concerning Foreign Inv. in the U.S., 73 Fed. Reg. 4677 (Jan. 25, 2008).

6 See CFIUS Annual Report to Cong. (2014) at 19, https://www.treasury.gov/resource-center/international/foreign-investment/Documents/Annual%20Report%20to%20Congress%20for%20CY2014.pdf.

7 See U.S. China Econ. and Sec. Rev. Comm., 2012 Report to Cong., (Nov. 2012) http://origin.www.uscc.gov/sites/default/files/annual_reports/2012-Report-to-Congress.pdf.

8 Pub. L. No. 107-56, Title X, § 1014, October 26, 2001; 42 U.S.C. § 5195c(e).

9 42 U.S.C. § 5195c(b)(2).

10 42 U.S.C. § 5195c(b)(3).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.