REVIEW

The IPO market produced 98 IPOs in 2016, the second down year in row, coming in 36% below the tally of 152 IPOs in 2015. In the 12-year period preceding 2015, which saw an annual average of 138 IPOs, there were only three years in which IPO totals failed to reach the 100-IPO threshold.

The year started slowly, with the first quarter producing only eight IPOs, but the pace of new offerings subsequently improved and steadied, with the succeeding three quarters producing 30, 31 and 29 IPOs, respectively. The quarterly average of 31 IPOs that has prevailed over the past two years is less than two-thirds the quarterly average of 53 IPOs produced during 2013 and 2014.

Gross proceeds in 2016 were $18.54 billion, 66% below the $25.17 billion raised in 2015 and the lowest annual tally since the $15.05 billion raised in 2003. Average annual gross proceeds for the 12-year period preceding 2016 were $35.73 billion—93% higher than the corresponding figure for 2016.

IPOs by emerging growth companies (EGCs) accounted for 84% of the year's IPOs, down from 93% in 2015. Since the enactment of the JOBS Act in 2012, 85% of all IPOs have been by EGCs.

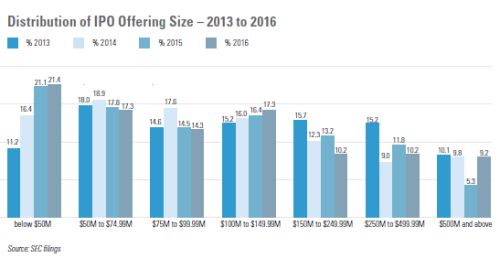

The median offering size for all 2016 IPOs was $94.5 million, or 3% above the $91.7 million figure for all 2015 IPOs, but 6% lower than the $101.0 million median for the five-year period preceding 2015.

The median offering size for life sciences IPOs in 2016 was $55.5 million, or 23% below the $71.8 million figure for life sciences IPOs in 2015 and 11% below the $62.4 million median size for life sciences IPOs in the five-year period preceding 2015. By contrast, the median offering size for non–life sciences IPOs in 2016 was $131.6 million—up 2% from the $128.5 million median in 2015 and up 3% from the $128.1 million median for the five-year period preceding 2015.

In 2016, the median offering size for IPOs by EGCs was $77.5 million, compared to $368.6 million for IPOs by non-EGCs— both tallies representing the lowest annual levels since 2012. From 2012 to 2015, the median EGC IPO offering size was $87.0 million, compared to $425.5 million for non-EGC IPOs.

The median annual revenue of all IPO companies in 2016 was $66.5 million, or 76% above the $37.8 million median figure for 2015, but well below the $92.7 million median figure for the five-year period from 2010 through 2014. The median life sciences IPO company in 2016 had annual revenue of $2.3 million, compared to $205.8 million for all other IPO companies.

EGC IPO companies in 2016 had median annual revenue of $39.2 million, compared to $1.54 billion for non-EGC IPO companies. The median annual revenue for non–life sciences EGC IPO companies in 2016 was $113.8 million, 5% above the $108.2 median that prevailed from the enactment of the JOBS Act through 2015.

The percentage of profitable IPO companies increased to 36% in 2016 from 30% in 2015. Only four life sciences IPO companies in 2016, or 10% of the total, were profitable, matching the percentage over the five-year period preceding 2016. In 2016, 53% of non–life sciences IPO companies were profitable, down slightly from 55% for the five-year period preceding 2016.

In 2016, the average IPO produced a first-day gain of 12%, compared to 16% for the average IPO in 2015. The 2016 figure is the lowest since 2010. The average life sciences IPO company gained 6% in first-day trading in 2016, compared to 16% for the year's non–life sciences IPO companies. This represents a reversal from 2015, when the average life sciences company rose 18% on its first trading day—3% higher than the gain achieved by non–life sciences IPO companies. There was a solitary "moonshot" (an IPO that doubles in price on its opening day) in 2016—down from an annual average of six moonshots between 2013 and 2015.

In 2016, 24% of IPOs were "broken" (IPOs whose stock closes below the offering price on their first day). This figure is down from 26% in 2015. Life sciences company IPOs were twice as likely as other IPOs to be broken in 2016, with 35% of life sciences company IPOs closing first-day trading at a loss, compared to 17% of non–life sciences company IPOs.

At year-end, the average 2016 life sciences IPO company was trading 16% above its offering price and the average non–life sciences IPO company was trading 34% above its offering price. Overall, the average 2016 IPO company ended the year 26% above its offering price. The year's best performers were a pair of tech companies, Acacia Communications (trading 168% above its offering price at year-end) and Impinj (up 152%), followed by life sciences companies Novan (up 146%) and AveXis (up 139%).

At the end of 2016, 30% of the year's IPO companies were trading below their offering price—life sciences companies faring worse than their non–life sciences counterparts, with a figure of 45%, compared to 19% for non–life sciences IPO companies—while 44% of all 2016 IPOs were trading at least 25% above their offering price.

Individual components of the IPO market fared as follows in 2016:

- n VC-Backed IPOs: The number of IPOs by venture capital–backed US issuers declined 38%, from 63 in 2015 to 39 in 2016, but VC-backed IPOs still accounted for 50% of all US-issuer IPOs in 2016. The median offering size for US venturebacked IPOs declined 4%, from $77.9 million in 2015 to $75.0 million in 2016. The median deal size for non–VC-backed companies was $147.0 million in 2016, up 30% from $113.3 million in 2015. The average 2016 US-issuer VC-backed IPO gained 30% from its offering price through year-end. The median amount of time from initial funding to an IPO increased from 6.3 years in 2015 to 7.7 years in 2016—the highest annual level since 2010—while the median amount raised prior to an IPO, at $97.9 million, was the second-highest figure since 1996.

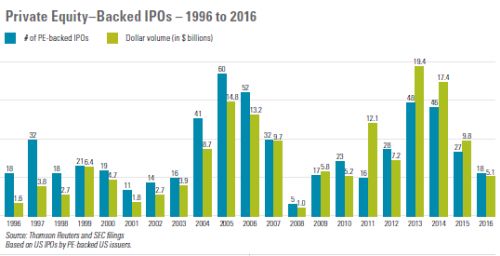

- n PE-Backed IPOs: Private equity–backed IPOs by US issuers declined by one-third, from 27 in 2015 to 18 in 2016, accounting for 23% of all US-issuer IPOs in each year. The median deal size for PE-backed IPOs in 2015 was $250.0 million—more than triple the $75.0 million figure for all other IPOs. The average PEbacked IPO in 2015 gained 34% from its offering price through year-end.

- n Life Sciences IPOs: There were 40 life sciences company IPOs in 2016, compared to 72 in 2015 and 98 in 2014. Although the portion of the IPO market accounted for by life sciences companies declined to 41% from 47% in 2015, this market share compares favorably to the 40% figure in 2014 and is well above the 17% figure for the five-year period preceding 2014. The average life sciences IPO company in 2016 ended the year up 16% from its offering price, compared to a 34% year-end gain for non–life sciences IPO companies.

- n Tech IPOs: Deal flow in the technology sector declined by 29%, from 35 IPOs in 2015 to 25 IPOs in 2016—the lowest annual number since 2009—but the sector's share of the US IPO market increased from 23% to 26%. The 2015 figure was a low point for the sector, reached after five consecutive years of decline from the 46% US market share achieved in 2011. The average tech IPO ended the year with a gain of 37% from its offering price, compared to 23% for non-tech IPOs.

- n Foreign-Issuer IPOs: The number of US IPOs by foreign issuers declined by 43%, from 35 in 2015 (23% of the market) to 20 in 2016 (20% of the market). Among foreign issuers, Chinese companies led the year with six IPOs, followed by Bermuda companies (three IPOs) and companies from Switzerland and the Netherlands (each with a pair of IPOs). The average foreign issuer IPO company ended the year trading 12% above its offering price.

In 2016, 40 companies based in the eastern United States (east of the Mississippi River) completed IPOs, compared to 38 for western US–based issuers. California led the state rankings with 19 IPOs, followed by Massachusetts (with 12 IPOs), Texas (with six IPOs) and Georgia and Illinois (each with five IPOs).

OUTLOOK

IPO market activity in the coming year will depend on a number of factors, including the following:

- n Economic Growth: The US economy lost momentum over the last three months of 2016 and the year ended with an annual growth rate of 1.6%—its weakest performance in five years. After raising its benchmark interest rate only once in the preceding decade, the Federal Reserve increased the rate in December 2016 and again in March 2017, and further rate hikes are widely expected in the coming year. These factors—together with uncertainty regarding the specific terms and timing of the Trump Administration's tax and economic programs, the bumpy slowdown in China's economic growth, the unknown outcome of Brexit, and political uncertainty in the Eurozone—all contribute to a hazy economic outlook in early 2017.

- n Capital Market Conditions: Following mixed results in 2015, the major US stock indices posted solid gains in 2016, with the Dow Jones Industrial Average up 14% and the S&P 500 and Nasdaq Composite Index each up 9%. Seemingly enthused by the pro-business orientation of the new administration, the major indices rose further, to record levels, in the first quarter of 2017, although the capital markets could begin to cool if economic growth weakens. Sustained strength in capital market conditions would likely contribute to increased IPO activity but, by itself, may be insufficient to restore IPO deal flow to the levels seen from 2013 to 2015.

- n Venture Capital Pipeline: Despite the decline in US venture-backed IPOs for the second consecutive year, the pool of VC-backed IPO candidates remains large and vibrant, including approximately 150 "unicorns" (private tech companies valued at $1 billion or more). While access to plentiful private financing at attractive valuations tends to encourage VC-backed companies to delay their IPOs, investors at some point will seek cash returns as opposed to paper gains. The solid aftermarket performance of VCbacked IPOs in 2016 is likely to generate demand for additional IPOs in 2017.

- n Private Equity Impact: Having increased their fundraising for the fourth consecutive year, private equity firms are now sitting on record levels of committed capital. PE firms are eager to put their reserves to work, but the supply of capital is intensifying competition for quality deals and driving up prices. Despite increases in the level of equity invested in deals, which decreases investor returns, PE firms are facing pressure to exit investments—via IPOs or sales of portfolio companies— and return capital to investors.

- n Impact of JOBS Act: Although it was intended to encourage EGCs to go public, the JOBS Act—combined with other regulatory and market changes—has made it easier for EGCs to stay private longer and has provided them with greater flexibility in timing their IPOs. The result has been a large and growing pool of qualified IPO candidates. The extent to which these companies decide to pursue IPOs, and the timing of these decisions, will have a substantial effect on the overall IPO market.

The IPO market has begun 2017 on a hopeful note, with 20 IPOs in the first quarter of the year—more than double the tally in the first quarter of 2016. In January, the impending AppDynamics IPO was poised to test investor appetite for IPOs by tech unicorns, until Cisco agreed at the last minute to acquire the company for $3.7 billion in cash. Snap's very successful IPO in early March could jump-start the market and inspire other qualified companies to follow suit.

To view the full article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.