On May 18, 2015, two foreign tax credit ("FTC Generator") cases were argued before the Second Circuit Court of Appeals.6 In both cases, Bank of New York Mellon and American International Group, the taxpayer lost the FTC Generator issue in the lower court. In Bank of New York Mellon, the Tax Court held that a structured trust advantaged repackaged securities ("STARS") deal lacked economic substance (pre-codification under Section 7701). Consequently, the court held BNY could not claim foreign tax credits or deductions for expenses related to the transaction, and income from the transaction was treated as US-source income.

Bank of New York Mellon

The STARS transaction was structured to provide BNY with below market cost financing. The complex transaction structure involved BNY transferring income-producing property into a trust subject to UK tax. As part of the transaction, BNY entered into forward sale agreements, a zero coupon swap agreement, a credit default swap and security arrangements with a British bank. The arrangements created a $1.5 billion secured loan from the British bank to BNY.

As a result of the STARS transaction, BNY claimed foreign tax credits of approximately $200 million and expense deductions of approximately $7.6 million in 2001 and 2002. BNY also reported the income from the assets transferred to the trust as foreign sourced.

The Tax Court shot down the STARS transaction under the economic substance doctrine. Under the objective prong of the doctrine, the Tax Court held that the STARS structure lacked economic substance because BNY did not have a reasonable expectation of making a non-tax profit by using the STARS structure. The court explained that the STARS structure did not increase the profitability of BNY's income-producing assets, and the structure's main activity was circulating income. The Tax Court refused to take into account the profit from the STARS assets when evaluating the transaction, stating that "[e]conomic benefits that would result independent of a transaction do not constitute a non-tax benefit for purposes of testing its economic substance."7

When evaluating the structure under the objective prong, the Tax Court followed its holding in Compaq Computer Corp. v. Commissioner8, which held that foreign taxes are treated the same as any other transaction cost when determining whether the transaction makes economic sense. The Tax Court acknowledged that "the Court of Appeals for the Fifth and Eighth Circuits have ... held that foreign taxes should not be taken into account in evaluating pre-tax effects for purposes of the economic substance analysis."9 Nevertheless, the Tax Court determined that it was not bound by the precedent in the Fifth and Eighth Circuits because the case would be appealable to the Second Circuit and neither the Supreme Court nor the Second Circuit has decided the issue.

BNY appealed to the Second Circuit, arguing, in part, that the Tax Court erred in applying the economic substance doctrine, and focused on the business purpose of the transaction – borrowed funds on favorable terms. The government cross appealed and argued that BNY was not entitled to an interest deduction. The three judge panel (Cabranes, PJ., Chin, Raggi, JJ.) gave BNY's counsel more pushback than government counsel and appeared skeptical of BNY's arguments.

American International Group

The same panel heard oral argument in a separate appeal by AIG, challenging the District Court's decision denying AIG's partial motion for summary judgment that it was entitled to certain foreign tax credits. The District Court agreed with the government that transactions resulting in foreign tax credits are subject to a requirement of economic substance.

AIG entered into the six transactions at issue from 1993 to 1997 by selling a foreign lender preferred shares in an SPV with a commitment by AIG-FP to repurchase those shares after a fixed term of years for the original purchase price. Primarily using the proceeds from the sale of shares, the SPV acquired investments that generated income over time for which it paid taxes to the local tax authority. The income was generally distributed to the lender, which paid little to no taxes on the distribution by characterizing the preferred stock as an equity investment and the distribution as a tax-exempt distribution from a subsidiary to its parent under the tax law in the lender's jurisdiction. AIG then claimed foreign tax credits for all foreign taxes paid by the SPV and applied the credit amounts in excess of its US tax liability on the transactions to other unrelated taxes. AIG argued that the sale of preferred stock was a loan and the SPV remained an AIG subsidiary under US tax law because there was an obligation to repurchase the stock. Accordingly, AIG deducted the amount of the distribution to the lender as interest and claimed foreign tax credits.

The government argued that the transaction lacked economic substance because it allegedly did not have purpose or utility beyond the expected tax benefits. The District Court accepted the government's argument. Accordingly, AIG needed to demonstrate economic substance for its transaction and that "what was done, apart from tax benefits, is what was intended by Congress."10

AIG argued that it anticipated a pretax profit of $168.8 million for the transactions in question. It reached this amount by considering the SPV's investment income and subtracting payments to the purported lender and operational costs. However, the court noted that this calculation took into account the effects of the tax exempt payments to the purposed lender, which in turn provided a more favorable dividend rate to AIG-FP because of its anticipated tax benefit. The government's expert opined that there would be no gain for AIG if the dividend were taxable to the lender. AIG argued that the transaction should not be rewritten by the government as in a fictional "world without taxes." But the court disagreed, stating that the tax exempt status of the dividend wassignificant to the transactions and should be reflected in the profit calculation. The District Court found that the evidence in the record was not sufficient to satisfy AIG's burden for partial summary judgment on the foreign tax credit issue.

At oral argument in the Second Circuit, AIG's counsel argued that the economic substance doctrine should not apply to AIG's transaction, that AIG made a pre-tax profit and increased its tax burden and that no court had ever struck down a similar transaction with a pre-tax profit under the economic substance doctrine. On the other hand, the government explained that the foreign tax had never been paid by the taxpayer, which was inconsistent with the purpose of the credit: to eliminate double taxation. The panel seemed to be more receptive to the government's argument, but reserved decision. Stay tuned.

Salem Financial Inc.

On May 14, the Federal Circuit Court affirmed a decision by the Court of Federal Claims holding that a subsidiary of BB&T Corporation was not entitled to an estimated $500 million in foreign tax credits associated with a STARS foreign tax credit generator transaction.11 The court also upheld penalties for negligence and substantial underpayment of taxes. However, the court held that the taxpayer was entitled to claim interest deductions for the interest it paid on the STARS loan and remanded to the Court of Federal Claims for reassessment of the penalty amount.

The STARS transaction was jointly developed and marketed by Barclays Bank and an accounting firm to generate foreign tax credits for a US taxpayer. Pursuant to BB&T's STARS transaction, in effect from August 2002 through April 2007, BB&T established a trust containing approximately $6 billion in revenue-producing bank assets, the revenues from which were cycled through a UK trustee before returning to the trust. The assessment of UK taxes generated UK tax credits that were shared evenly between Barclays and BB&T. There was also a $1.5 billion loan from Barclays to BB&T, with a higher interest rate than BB&T's normal cost of borrowing. Barclays made monthly "Bx" payments to BB&T, representing BB&T's share of the foreign tax credits, which had the effect of reducing the interest cost of BB&T's loan.

BB&T argued that the STARS transaction should be viewed as a single integrated transaction, whereby the existence of the trust permitted Barclays to offer BB&T a $1.5 billion loan at a favorable rate. However, looking at the economic realities of the integrated transaction, the Court of Federal Claims concluded that the transaction must be disregarded for lack of economic substance.

On appeal, the Federal Circuit Court agreed with the trial court's holding that the loan and the trust transaction must be bifurcated for purposes of economic substance, and not considered as a single integrated transaction. Examining the economic reality of the STARS transaction, the Court concluded that the transaction, which generated tax credits, was "simply a money machine."12 The Circuit Court agreed with the trial court that the STARS transaction was "a contrived transaction performing no economic or business function other than to generate tax benefits," which had no incremental effect on the taxpayer's activities and had no realistic prospect of producing a profit.13. The Court noted that the transaction exposed BB&T to no economic risk. The only risk was that the IRS may challenge the tax treatment of the transaction.

The Circuit Court also found that the STARS transaction had no non-tax business purpose: the STARS Trust was a "prepackaged strategy" created to generate US and UK tax benefits. The Court rejected BB&T's argument that it sought to earn a profit in the form of the Bx payment, and that earning a profit is a business purpose. The Court held that the Bx payment did not represent profit from any business activity; it was simply the way the parties shared in the tax benefits of the trust transaction.

BB&T also argued that it was entitled to deduct interest it paid on the $1.5 billion STARS loan, which the trial court disallowed, holding that the loan, like the trust, lacked economic substance. The Circuit Court agreed with the taxpayer and concluded that the loan resulted in a substantive change in BB&T's economic position. It had "real economic utility to BB&T."14

Accordingly, BB&T was entitled to claim interest deductions for the interest it paid on the loan. On the subject of penalties, the Circuit Court upheld the trial court's decision to impose an accuracy-related penalty under Section 6662(a). The Circuit Court was not satisfied that the taxpayer established reasonable cause for the underpayment by relying on a tax opinion and advice from PWC.

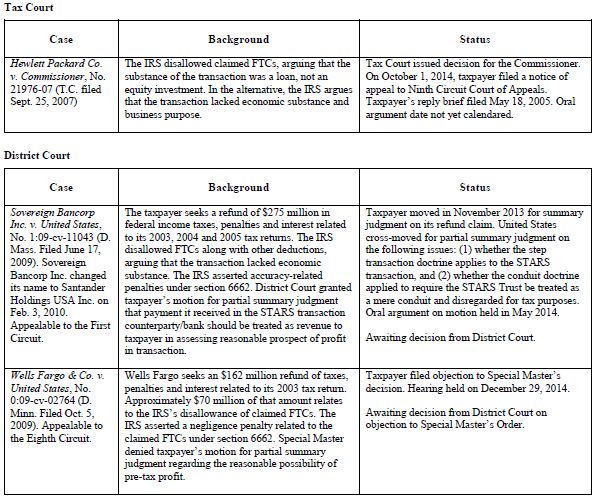

The chart below summarizes the status of other currently-docketed FTC cases.

Footnotes

6 See Bank of New York Mellon Corp. v. Commissioner, 140 T.C. 15 (2013); American International Group, Inc. v. United States, 111 A.F.T.R. 2d 2013-1472 (S.D.N.Y. 2013).

7 140 T.C. 15 at 36.

8 113 T.C. 217 (1999).

9 140 T.C. at 32 n. 9.

10 111 A.F.T.R.2d 2013-1472, at 1473.

11 Salem Financial Inc. v. United States, No. 14-5027 (Fed. Cir. May 14, 2015)

12 Slip. Opn. at 31.

13 Id. at 30.

14 Id. at 43.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.