A recent article in the Antitrust Law Journal, "A Survey of Evidence Leading to Second Requests at the FTC," by Darren S. Tucker, a FTC attorney advisor who reviewed non-public information on decisions to investigate proposed transactions for the period August 2008 to August 2012, sheds light on the types of evidence the FTC staff considers when determining whether a transaction warrants a "second request" under the Hart-Scott-Rodino ("HSR") Act.

The issuance of a "second request" is a significant event because it prevents the parties to a proposed transaction from closing until after they have substantially complied with the request for additional information and have observed a second waiting period. As the article rightly notes, the "decision whether to issue" a "second request" is "a critical stage of the HSR process."

What evidence does the FTC staff look at to determine whether a transaction warrants a "second request"? Based on the article a number of observations can be made about transactions involving computer hardware, software, and components, including Internet-based services that led to a "second request" (hereafter "technology transactions").

First, according to the article, for those technology transactions receiving a "second request," (1) the size and relative number of the "market" participants played a role 100% of the time, (2) the unlikelihood that competitive entry would deter or offset the anticompetitive effects of the proposed transaction played a role 70% of the time, (3) customer concerns that the proposed transaction would lead to anticompetitive effects played a role 30% of the time, and (4) internal "hot" documents from the combining parties predicting that the proposed transaction will result in anticompetitive effects such as higher prices or a loss of competition played a role 60%of the time.

Second, the change in the number of significant competitors also played a role for technology transactions determined to warrant a "second request," according to the article. (The article identifies a significant competitor as a firm that either offers the products or services demanded by most customers in an area, or exceeds a share threshold, which was often 5 percent.) The table below reports the change in number of "significant competitors" for those transactions that received a "second request."

Significantly, 19 of the 21 technology transactions that received a "second request" resulted in four or fewer "significant competitors" post-transaction.

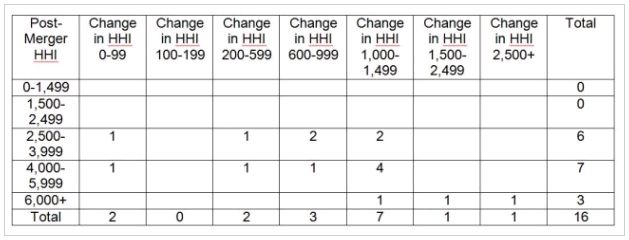

And finally, according to the article, technology transactions that resulted in high concentration post-merger almost always received a "second request." Concentration is measured by calculating the Herfindahl-Hirschman Index ("HHI"), which is simply the sum of the squares of the shares of the competitors in the "market." According to the antitrust agencies' guidelines for horizontal mergers, mergers that result in an increase in the HHI of more than 100 points with a post-merger HHI of at least 1,500 "often warrant scrutiny" whereas mergers resulting in an increase in the HHI of more than 200 with a post-merger HHI above 2,500 "will be presumed to be likely to enhance market power." (A merger enhances market power "if it is likely to encourage one or more firms to raise price, reduce output, diminish innovation, or otherwise harm customers as a result of diminished competitive constraints or incentives.") As noted in the table below, all but two of the technology transactions that received a "second request" resulted in an increase in the HHI of more than 200 with a post-merger HHI above 2,500. In other words, the vast majority of technology transactions receiving a "second request" were "presumed to be likely to enhance market power," based on high concentration after the proposed transaction and a large increase in the HHI.

So, what does all of this mean in terms of predicting whether the FTC will investigate your technology transaction? Antitrust counsel (and an economic expert) should be involved in your proposed technology transaction as soon as possible. Also keep in mind that although a second request can only be issued in connection with transactions that are large enough to require a premerger filing under the HSR Act, the same factors are likely to apply to potential investigations of transactions that are too small to require an HSR filing and may already have been completed. The FTC and the Justice Department regularly investigate mergers even though no HSR filing was required.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.