The UK Government has issued a consultation paper on the tax treatment of gains accruing on disposals of non-residential real estate in the UK by non-UK residents, significantly increasing the tax exposure of non-UK owners of UK non-residential real estate in the UK and updating the taxation of UK residential real estate.

The proposals will form the basis of legislation which will take effect from April 2019.

Historically, non-UK residents were not liable to capital gains tax on disposals of UK real estate. This first changed in 2013 for corporate owners of personal use residential real estate (ATED related CGT) and was widened in 2015 to include all direct owners of residential real estate, be they individuals or corporates (non- resident CGT), other than funds or other widely held companies.

Changes to the taxation of direct owners of UK real estate

It is now proposed that all non-UK resident owners of UK real estate (residential and non-residential) will be subject to capital gains tax on gains accruing after April 2019 on both direct and indirect disposals.

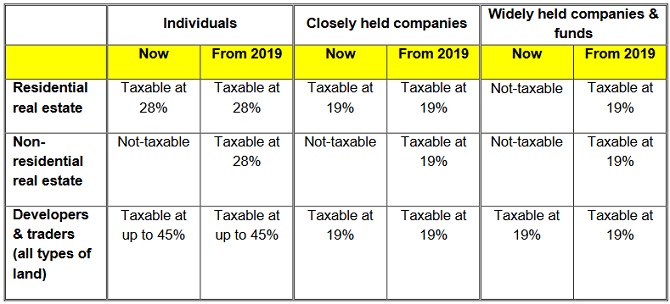

The current and future tax on the gains arising from the direct disposal of UK real estate by non-UK residents can be summarised as follows:

The new rules will apply from 1 April 2019 for corporates and from 6 April 2019 for individuals.

What happens to properties purchased before 2019?

As with the introduction of ATED related CGT in 2013 and non-resident CGT in 2015, it is proposed that for non-residential real estate only gains attributable to changes in value after the introduction of the new rules on 1 April 2019 will be taxable. Effectively therefore the default base cost for any non-residential real estate sale after 1 April 2019 will be the value of the property on 1 April 2019.

There will also be an option for the real estate owner to elect to treat a pre-April 2019 acquisition cost as the base cost where there is a loss over the whole period of ownership.

Changes to the taxation of indirect owners of UK property

Currently, except in rare circumstances, the UK does not seek to tax gains arising on the disposal of interests in entities that hold UK real estate.

From April 2019, in addition to the rules above, indirect disposals of UK real estate (i.e. the disposal of shares in an entity, or the holding entity of such an entity) which holds UK real estate will now be brought within the charge to UK tax.

The base cost for any indirect disposal will be the value in April 2019, it will not be possible to carry forward unrealised losses from before that date (as will be the case with direct disposals).

For this new tax to apply, two tests must be satisfied:

- The entity being disposed of must be 'property rich';

- The non-resident (and any 'related parties') must own, or have owned in the previous 5 years at least a 25% interest in the entity.

What is 'property rich'?

A property rich entity is one which derives 75% or more of its value from UK real estate, both non-residential and residential (on a gross asset value basis at the time of disposal, with no deduction for debt). The test will be applied to groups of companies on a consolidated basis where the group is being disposed of.

What are related parties?

Related parties will be defined to include: companies within the same group or under common control; family members (spouses, children brothers and sisters and ancestors or lineal descendants), partners in partnerships and persons acting together (for example joint ventures).

Funds and life assurance companies

Existing rules provide that for certain types of UK collective investment vehicles and life assurance companies gains on direct disposals by the funds are not charged to tax, either by virtue of their tax status or residence. Further, disposals by non-resident investors of their investment in these funds are not currently charged to UK tax.

From April 2019, disposals of fund interests will be subject to the new indirect disposal rules. These are unlikely to impact holdings in widely held commercial funds due to the 25% test. Further, non-UK collective investment schemes will be subject to tax on disposals of UK real estate (residential and non-residential) from April 2019.

UK resident collective investment vehicles and REITs will remain exempt from capital gains tax or corporation tax where that is the case currently, but distributions of capital gains by REITs to non-UK residents will be subject to the 20% withholding tax that applies to distributions of rental income.

What about Double Tax Treaties?

Where tax treaties reserve taxing rights to a foreign jurisdiction, e.g. Luxembourg, then the indirect disposal rules will not apply. Foreign jurisdictions will primary taxing rights and in high tax jurisdictions, such as the US, the tax payable by US residents will likely be available as a credit against (and may eliminate) the tax payable in the UK.

However, many tax treaties do not provide for this and in particular the tax treaties between the UK and Jersey, Guernsey and the Isle of Man were updated in 2016 to provide for the UK to retain taxing rights in respect of indirect disposals by holding companies in those jurisdictions, which will not offer any protection from the indirect disposal rules.

It is likely that going forward that the UK will seek to update Double Tax Treaties that do not provide for it to retain taxing rights in respect of indirect disposals so that it does so, in line with the OECD model.

Accordingly Luxembourg and other protected jurisdictions may not retain their advantages for long.

Anti-forestalling rules have been introduced to prevent property owners from planning in respect of existing structures with the use of double tax treaties. Where a holding vehicle is relocated to a jurisdiction in order to avoid the application of the indirect disposal rules, any advantage purportedly obtained will be counteracted by HMRC.

Reporting and Enforcement

For transactions under these new rules by non-residents subject to CGT, the reporting process will be the same as with NRCGT, namely a return will have to be submitted within 30 days of the disposal being completed and the tax paid within this time frame. Others will continue to pay tax under the self-assessment regime.

In order to ensure that HMRC is aware of indirect disposals by non-residents, there will be a reporting requirement on certain advisors who are aware of the conclusion of the transaction and cannot reasonably satisfy themselves that the transaction has been reported to HMRC.

What happens to ATED related CGT?

It is the Government's intention that the existing regimes for the taxation of residential real estate (ATED related CGT and non-Resident CGT) should be harmonised and for corporates those gains become subject to corporation tax in the same way as a UK resident or incorporated company from 1 April 2019. Similarly, individuals would be brought within the main capital gains tax regime.

Rental income

There are no changes proposed to the taxation of rental income from UK real estate.

Register of beneficial ownership of UK property

Separate, but linked to the new tax proposals is the proposal to introduce a public register of 'overseas entities' that own UK real estate. This was first announced in 2016 and an update was issued in December 2017 stating that a draft bill would be published setting out how the register would be created and what information would be publically available in 2018.

This register will assist with the enforcement of the new tax rules, in particular allowing for the identification of indirect disposals of UK property.

What does this mean and what should I do now?

- Direct and indirect owners of UK real estate will need to take advice on their individual circumstances and structures and all UK property investments should be reassessed for profitability in light of the new tax rules.

- Where a decision is made to retain a real estate investment post April 2019, it is unlikely to be necessary to carry out any restructuring in order to ensure that only post April 2019 gains are taxable as this will be the case under the automatic rebasing rules.

- Where properties may be subject to exceptional increases in value in the future, for example on the release of a restrictive covenant, or the grant of planning permission, steps should be taken to crystallise that value in advance of the April 2019 rebasing, so that it is not taxable on a future disposal.

- Closely held companies should be reviewed to assess their liability for indirect disposals by reference to the 'property rich' and related party' tests.

- In particular where intra family transfers are contemplated as part of estate planning arrangements, which will be treated as indirect disposals and become taxable after April 2019, they should be completed in advance of that date. In some cases it may be appropriate to transfer property rich family entities into trust to allow for a flexible class of beneficial ownership in future.

- Families owning property rich entities may also wish to consider introducing non-real estate assets (or non-UK real estate) into those entities to ensure

- For future purchasers, investors with commercial reasons for doing so may wish to consider using entities established in jurisdictions which do not allow for the indirect charge.

- Finally, the arbitrage between the taxation of UK property owning entities and non-UK owning ones will narrow considerably and in many cases be eliminated from April 2019 and from that point, it may well be more efficient for foreign investors to establish vehicles to own UK property in the UK, rather than outside and for existing structures to be relocated to the UK.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.