"In continental Europe, some large groups have built economic capital models for capital management purposes. These will need enhancing".

The solvency regime introduced to the UK life insurance market two years ago under ICA rules anticipates some of the changes that the European Union’s Solvency II project to reform prudential regulation of insurance will impose across all 25 member states in 2010 or later. Although this may mean the UK is ahead of its European peers, we anticipate some differences between the regimes which will necessitate reforms by insurers to ensure compliance.

Like the UK system introduced by the Financial Services Authority, Solvency II seeks to increase policyholders’ protection and to support market stability. Advice from the Committee of European Insurers and Occupational Pensions Supervisors (CEIOPS) to the European Commission provides an insight into how it will affect technical provisions, capital structure, risk management and group capital requirements.

We believe the key developments when current UK rules are replaced by the Solvency II regime will be:

- Unit-linked and non-profit contracts will be fair valued.

- Technical provisions will include a risk margin.

- The risk capital calculation will be moved to Pillar One of the new regime and may therefore be disclosed and subject to audit requirements.

- Diversification effects within insurance groups may be allowed for.

Comparison of regimes

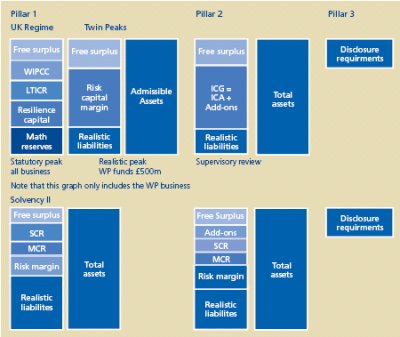

Both regimes are based on a three-pillar approach. The first pillar considers the quantitative requirements of the system, the second pillar deals with the qualitative aspects and the third pillar is concerned with disclosure requirements. The chart over the page provides a comparison:

Technical provisions

Solvency II’s approach towards technical provisions shares many characteristics with the FSA’s approach for the realistic peak. However, as the realistic peak only applies to "realistic reporting firms" holding withprofit funds in excess of £500m, the move to fair values will change the calculation of non-profit and unit linked provisions.

For realistic reporting firms, the main difference is that an explicit risk margin will be added on top of the fair value of future liabilities. This will lead to an increase in the technical provisions that firms need to allow for.

In the fair valuation process the two regimes share the following features:

- Best estimate assumptions are used to project future cash flows, including lapse assumptions.

- No surrender floors are to be applied to the value of the technical provisions.

- Discretionary benefits are to be provisioned for.

- Cost of options and guarantees are to be valued on a market consistent basis.

Solvency II will move the valuation of nonprofit and unit-linked businesses to realistic reporting. Under the current regime, the valuation of non-profit and UL businesses may still contain arbitrary prudential margins. These will be replaced by the Market Value Margin (MVM). CEIOPS is still debating how the MVM will be calculated.

The surrender value has been used as a floor in the valuation of technical provisions to address the risk of insurers not being able to pay out the surrender benefits, should mass surrenders take place. Under Solvency II, this risk is dealt with more appropriately by capital. We will also see the possibility of considering prudent lapse rates in the calculation of the mathematical reserves.

The FSA have introduced1, from December 2006, changes to the minimum levels of Pillar 1 reserves. They reduce the aforementioned differences between the UK and Solvency II regimes in respect of the non-profits and unit linked businesses. The main changes affecting the non-profits and unit linked businesses are that non-policy related expenses can be reserved within the mathematical reserves rather than at a policy level, policies can be valued as assests if surrender values are not guaranteed and that firms will be allowed to make a prudent lapse rate assumption when calculating the mathematical provisions.

These changes can effectively release some of the current margins embedded in the calculation of mathematical reserves and thus move the calculation of these provisions towards a fair value approach. Some margins will be retained and therefore Solvency II will be replacing these arbitrary margins with a defined calculation. The impact of this will depend on the approach that is finally adopted and the extent of current prudential margins which varies by company.

Minimum Capital Requirement

The UK Minimum Capital Requirement is the higher of the base capital resources requirements and the sum of the long-term insurance capital requirement and the resilience capital requirement.

- The base capital resources requirement is €2.25m for a Directive mutual, €600,000 for a non-directive mutual and €3m for any other insurer subject to annual indexation based on the European index of consumer prices.

- The long term insurance capital requirement is the sum of the death risk capital requirement, the health risk capital requirement, the expense risk capital requirement and the market risk capital requirement.

- The resilience capital requirement is calculated on a series of stress tests that consider the effects of falls in the market value of equities and property and the more onerous of either a fall or rise in yields on all fixed interest securities. PS06/14 removes the resilience capital requirement for realistic reporting firms. CEIOPS is considering three ways of calculating Solvency II’s Minimum Capital Requirements. They are:

- A calculation based on existing Solvency I requirements; and

- A simple calculation based on the standard formula of the Solvency Capital Requirement

- As a margin over liabilities.

An absolute minimum floor expressed in Euros will apply and an allowance for investment risk in the MCR is still to be decided. CEIOPS recommends that during a transitional period of up to three years, the calculation of the MCR is based on a specified percentage of the Solvency I requirements. During the transitional period, Solvency II will likely raise the level of the MCR for an average continental European company. This is unlikely to apply to UK companies as most are well within MCR requirements already. After transition, the MCR will become more risk-oriented.

Solvency Capital Requirement

Pillar 1 and Pillar 2 in the UK currently work independently. Whilst Pillar 1 calculations form part of returns provided to the supervisor and are available to the public, Pillar 2 calculations are available exclusively to the regulator. Under Solvency II, the riskbased capital will be calculated in Pillar 1 and will be in the public domain. This may well lead to audit requirements with respect to risk capital calculations and processes. Insurers would face the significant challenge of increasing the quality and documentation of their models and processes.

The UK’s twin peak approach was introduced to complement existing Solvency I requirements. With the move of the riskbased capital calculation to Pillar 1 under Solvency II, there will no longer be a need for a twin peak calculation followed by an additional calculation in Pillar 2.

In continental Europe, some large groups have built economic capital models for capital management purposes. These will need enhancing. Some medium and small firms still need to embrace the risk-based capital concept and develop their models and knowledge. Their biggest challenge will be developing a risk management framework capable of withstanding the new supervisory review process.

CEIOPS’ working hypothesis is that the SCR will be calibrated consistent with a 99.5% confidence level over a one-year timeframe – the level used in the UK. However, firms will be required to have sufficient capital at a chosen confidence level to be able to survive a year and then, at the year-end, hold sufficient reserves so their liabilities could be transferred to a third party, ensuring an orderly run off.

This differs from the UK, where the Individual Capital Assessment (ICA) is determined on the assumption that assets held at the year-end need to be merely sufficient to cover best estimates of liabilities at the chosen confidence level.

In its second Quantitative Impact Study (QIS2) in May, CEIOPS attempted to calibrate the standard formula at a 99.5% confidence level, suggesting stress tests in some cases. We anticipate that a comparison between the stress tests companies use within their internal model calculations and those proposed within the standard formula approach will be inevitable. Companies will need to justify any large differences. This may thrust an additional task upon many UK firms. Our latest ICA survey2 suggests that, for example, there may be a significant gap between the assurance mortality trend stress levels currently being applied in the UK and those CEIOPS is suggesting.

Capital structure

Solvency capital’s main purpose is to protect policyholders against unexpected losses. Therefore, capital requirements are determined by their ability to absorb losses not only on an ongoing basis but in financially-stressed conditions. Under Solvency II, three tiers of capital are proposed. Tier 1 is composed of the highest quality capital.

Tier 2 consists of capital that, despite lacking some of the characteristics of Tier 1, still provides some degree of loss absorbency. Tier 3 considers elements that are subject to regulatory approval. A similar concept is used under the UK solvency framework where capital is divided into two tiers.

Risk management improvement

Although capital acts as a buffer should unforeseeable risks materialise and provides some protection that policyholders’ benefits will be met as they fall due, regulators are increasingly seeking to stimulate corporate structures and risk management frameworks as a key factor of solvency. Both the UK and Solvency II regimes seek to do this.

Under Solvency II, company boards will be responsible for setting risk tolerance limits, with senior management responsible for implementing risk management strategies. Firms will need to establish a risk management function in charge of monitoring, controlling and reporting compliance. In the UK, the FSA also asks firms to demonstrate that the ICA is embedded into their business. The FSA’s view is that the integration of risk and capital management is on the agenda of several firms but only limited progress has been made to date.

Insurance groups

The UK group capital resources requirement is calculated as the sum of the individual capital resources requirement of the parent company and the individual capital resources requirement of each of its regulated related undertakings3.

The calculation under Solvency II is likely to allow for diversification effects, provided that concerns about the assessment and evidence of the existence of such effects are addressed4. The group capital requirement could therefore be lower than the sum of the solo solvency capital requirements of its component entities. CEIOPS also suggests that the diversification effects could be passed down to individual entities of the group by notionally increasing the available capital, rather than decreasing the capital requirements.

Solvency II can be regarded as the natural progression of a process that has already started in the UK and should mean that UK insurers are further along in the process than their European counterparts. However, UK insurers need to enhance and adapt many processes involved in assessing and managing risks. Particular attention needs to be given to fully embedding the new framework into the day-to-day running of insurance businesses. There are also specific technical points to be addressed such as scenario testing and the assessment of operational risk, which still remain sketchy5.

Footnotes

- PSO6/14 was published in December 2006.

- Individual Capital Assessment Survey carried out by Deloitte & Touche LLP in March 2006

- See the Integrated Prudential Sourcebook PRU 8.3.33 R

- See CEIOPS Consultation Paper 14 "Draft Advice to the European Commission in the framework of the Solvency II project on sub-group supervision, diversification effects, cooperation with third countries and issues related to the MCR and SCR in a group context"

- See FSA’s comments on Operational risk in their Insurance Sector Briefing: ICAS – one year on

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.