EXECUTIVE SUMMARY

Background

The external environment has rarely been more challenging for heads of tax. Governments and tax authorities traditionally seek to increase tax receipts in times of austerity. Public scrutiny has increased for many, particularly in Western Europe.

Looking inwards, changes within businesses are driving an evolution of the tax department. Tax compliance increasingly operates on a current (real‑time) basis. Tax specialists need to combine business and technical expertise to drive value for their organisations.

But how much has this really affected heads of tax? What keeps them awake at night? Which jurisdictions are perceived as the most challenging and where in Europe it is seemingly becoming easier to do business?

In order to help understand this fast-changing landscape, Deloitte undertakes an annual survey to track trends as viewed by heads of tax.

Almost 1,000 companies across Europe participated in the Deloitte Tax Survey in 2013. The responses were often surprisingly unanimous for organisations that vary in size and structure, operating in different economies.

Headline findings

- The Netherlands and the UK were seen as the most favourable of the large jurisdictions, from a tax perspective, for inward investment. Both had worked hard to become more attractive to multinational companies, and this seemed to be working.

- Italy and Russia were viewed as the most challenging of the large jurisdictions, due to rapid legislative changes, ambiguity and different views of how tax positions should be interpreted.

- Above all, heads of tax wanted stable tax legislation. The biggest issue many cited was that already complex tax systems were being further complicated by rafts of new laws. Aside from the burden of keeping up with the changes and educating their teams, this was the main cause of tax uncertainty – frequent law change was also the thing that most would reduce in order to make their own countries more competitive.

- 75% of respondents had been subject to a tax audit in the past three years. More than a third would be likely to litigate if they felt that a tax investigation was unjust, either in terms of the process or the outcome.

- There was a clear divide with regard to the level of public debate around tax. The west of Europe – in particular Luxembourg, Switzerland, the UK, and the Netherlands – were facing media scrutiny, pressure from special interest groups and heated discussion around what constitutes a just and fair tax system. In the first three, this scrutiny was focused on multinationals; in the Netherlands the issue was mainly directed at the government. Eastern European countries, such as the Czech Republic and Hungary, were not recognising tax as a major public issue.

- Contrary to some public perceptions, the measure of success for heads of tax was not lowering the effective tax rate (or ETR), but strongly compliance‑focused: filing of returns in a timely manner and working with the business to ensure there are no nasty surprises around the corner.

- Heads of tax were also changing where they spend their time as they become more integrated with the business and in direct discussion with its operational parts. Tax technical roles may form part of the team, but the communication skills and focus needed by the head of tax these days are much broader.

- Respondents appeared to be stretched. Many had demanding roles but relatively small teams. Most (55%) had global or regional responsibilities and yet were operating with teams of fewer than three people.

- Shared Service Centres (SSCs) are available to support over half of those who responded. Two thirds used SSCs for some or all of their tax compliance work.

OPERATING IN EUROPE

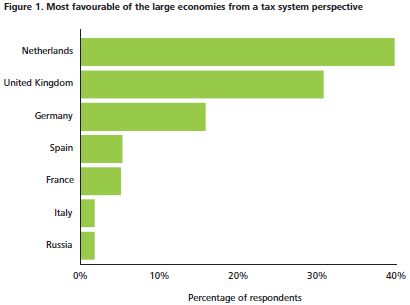

Most favourable jurisdictions from a tax system perspective

Respondents were asked to rate the major European economies – France, Germany, Italy, the Netherlands, Russia, Spain and the UK – in terms of which was deemed to be the most favourable from a tax system perspective. The reason for restricting views to the major economies was to recognise that many organisations do business in those economies and, therefore, their tax regimes affect many multinational groups.

The most favourable major economy to operate in was the Netherlands, closely followed by the UK.

The Netherlands was cited as having an easy and 'professional' tax system. It was seen as predictable, easy to contact the tax authorities and to receive a ruling within a few weeks. Respondents continually referred to the simplicity of its tax system and the ease of dealing with authorities.

For the UK, the tax officials were often praised as being helpful, and many of the respondents viewed it as operating international best practice. The tax authorities were viewed as pragmatic, clear and open.

Most favourable smaller jurisdictions from a tax system perspective

Respondents were then asked to select from the smaller European economies whether there was another country more favourable than the major economy already rated. Luxembourg and Switzerland were viewed as most favourable by the highest number of respondents, followed by Belgium and Ireland.

47% of respondents from the Netherlands picked their own country as the easiest to operate in and only 43% had experienced a tax authority audit in the Netherlands in the past three years. 58% of UK respondents picked their own country as the most easy to operate in, even though 73% had experienced a tax authority audit.

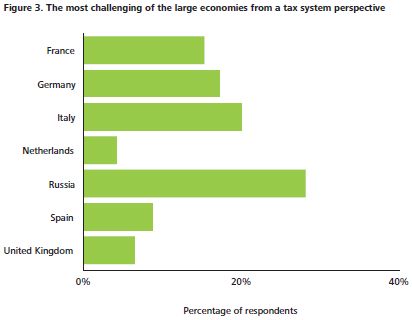

Most challenging large jurisdictions from a tax system perspective

Respondents were also asked to consider which of the major European economies were the most challenging from a tax system perspective. Russia was viewed as the most difficult of the seven largest European economies in which to operate. The main reasons stated were uncertainty and complexity. Comments also included that rules appeared opaque and arbitrary, or difficult to understand.

Italy was also viewed as challenging. Comments from respondents pointed out that the Italian tax system – being subject to frequent changes in tax law – suffered from different interpretations over time. This, combined with a very general anti‑abuse rule and criminal sanctions for tax issues, were the main reasons for its less favourable ranking.

Finally, respondents were asked whether there was a smaller economy that was more challenging than any of the large economies. Here, many respondents stuck with their chosen large economy as the most challenging, particularly Russia. However Greece, Portugal, Poland and Hungary also featured, in that order.

Comments on tax regimes

The reasons given for finding tax regimes favourable were strikingly similar – transparency, certainty, a well‑designed tax system, and the possibility of forming sensible working relationships with the tax authorities.

There was also widespread consensus over why jurisdictions can be challenging from a tax perspective. Respondents did not like uncertainty, legislative change, and tax authorities that are unable or unwilling to find solutions to tax issues created by commercially motivated transactions. Russia, specifically, was cited as having a 'very different tax regime from the rest of Europe' that 'did not mesh well' with other commonly accepted structures for tax systems internationally.

Interestingly, few respondents referred to tax rates in their answers, which suggests that jurisdictions can afford to have relatively high tax rates, provided that their tax systems are uncomplicated and flexible.

Respondents were generally more critical of their own jurisdictions than of foreign jurisdictions. A third of French respondents picked their own country as most challenging versus only 15% overall. 37% of German respondents selected their own country versus 17% overall. This may reflect that, for many respondents, their local jurisdiction is where their group's regional or worldwide headquarters are based, and therefore their local tax affairs are likely to be more complex (for example, due to the need to navigate debt financing complexities or controlled foreign company compliance and reporting obligations) than those of their (often relatively straightforward) subsidiary operations.

To read this Survey in full, please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.