1. EXECUTIVE SUMMARY

2012 is a big year for the UK, with the Diamond Jubilee, the Olympic and Paralympic Games and the continuing economic challenges. For preparers of half-yearly financial statements, it should be a relatively quiet year with only one amended accounting standard to admire and to implement. Flurries of activity from government, regulators and standard setters may result in further amendments to consider. But, for the moment, the forecast is fair. So, after devoting some time to those big 2012 stories, the theme in reporting will be polishing previous periods' precedents to produce perfect, or at least perfectly acceptable, publications. Unlike that sentence, some things are easier said than done. The third finding requires a little more explanation.

The aim of this Deloitte annual publication is to help those preparing and approving half-yearly financial reports by providing:

- an illustrative report for a UK listed company with subsidiaries and associates reporting in accordance with the relevant accounting standard, IAS 34, and the FSA's Disclosure and Transparency Rules. This is at Appendix 1;

- a Disclosure Checklist for such entities, at Appendix 2; and

- in the main sections, a survey of current practice in half-yearly financial reports, which highlights the areas of current weaknesses where improvements in reporting may be needed or desirable.

As with other Deloitte corporate reporting surveys, the population is split between investment trusts (see Section 7) and corporates. For corporates, the most interesting findings are around going concern disclosures. In 2010 the revised UK Corporate Governance Code introduced the provision, at C.1.3, that directors should report in their half-yearly financial statements that the business is a going concern and should provide supporting assumptions or qualifications as necessary. In 2011, the Financial Reporting Council announced its inquiry, led by Lord Sharman, into going concern and liquidity risk (the final report originally being expected at the end of February 2012). Prompted by this change and this interest, it might have been expected that the survey results would be one directional. There would be more from more companies. But this is not the case.

Results are split:

- 11% of corporates (2010: 5%) made no reference to going concern or financial resources considerations;

- 79% (2010: 61%) used the magic words "going concern"; and

- Three (2010: 0) auditors' review opinions included emphasis of matter paragraphs drawing attention to uncertainty over the companies' ability to continue as a going concern.

The third finding requires a little more explanation. Auditors' reviews are not mandatory but 68% of companies now choose to include such. That means that for the other 32% of corporates in the sample there can be no auditors' amber flags, being those easily spotted emphasis of matter paragraphs. There may be significant going concern uncertainties in some of these companies. What is clear is that economic challenges continue.

The other main findings include that:

- 48% (2010: 48%) of corporates met or exceeded the required information on principal risks and uncertainties;

- while not required, key performance indicators are provided by 98% of corporates; and

- one corporate and one investment trust did not meet the two month reporting deadline but both missed it by only a couple of days.

Finally, only 13% of corporates and 3% of trusts clearly complied with all of the requirements for the interim management report, being the narrative element of the half-yearly financial report.

Put together, all these findings indicate that opportunities abound for polishing the 2012 reports.

2. REGULATORY REQUIREMENTS

This section summarises the regulatory requirements for half-yearly financial reports of UK listed companies, covering:

- the timing and dissemination of half-yearly financial reports;

- the content of an interim management report (IMR);

- the inclusion of a responsibility statement in half-yearly financial reports;

- the content of a condensed set of financial statements;

- the provisions for single companies reporting under UK GAAP; and

- the application of these requirements to companies with securities listed or admitted to trading on the various exchanges operating in the United Kingdom.

The requirements stem from section 4.2 of the Disclosure and Transparency Rules (DTR) contained within the Financial Services Authority (FSA) handbook. The UK Listing Authority (UKLA) has periodically issued additional guidance to clarify the requirements of the DTR.

Going concern in half-yearly financial reportsIn October 2009, the Financial Reporting Council (FRC) published revised guidance for the directors of UK companies on going concern assessment and disclosures1. For the first time this provided detailed guidance on the assessment of going concern expected to be undertaken in preparing half-yearly financial reports and the disclosures arising from that assessment. The UK Corporate Governance Code provision C.1.3 became applicable for periods commencing on or after 29 June 2010, and requires that "The directors should report in annual and half-yearly financial statements that the business is a going concern, with supporting assumptions or qualifications as necessary". The equivalent provision of the 2008 Combined Code did not refer to half-yearly financial statements. Assessment of going concernThe FRC guidance requires directors to exercise judgement on the nature and extent of procedures undertaken in assessing going concern for the purposes of half-yearly financial reports. It also suggests that the following issues may trigger a need to re-examine the going concern assumption:

These examples are not intended to be exhaustive and directors should be alert to any other potential going concern issues. The FRC guidance also states that where going concern has become a significant issue, directors should undertake procedures similar to those that would be carried out for annual financial statements to ensure that all relevant issues have been identified and considered. Where no new issues have been identified, the FRC guidance recommends that procedures are undertaken to roll forward the previous budgets and forecasts by the length of the half-yearly period. The review periodThe FRC guidance makes clear that the review of going concern should cover a period of at least 12 months from the date of approval of the half-yearly financial report. Disclosures in respect of going concernThe FRC does not suggest that the same level of disclosure on going concern that is included in annual reports should routinely be given in half-yearly financial reports. What is recommended is that additional explanation should be given of any new events and circumstances arising subsequent to approval of the previous annual report. Where no new issues have arisen, a short statement confirming the use of the going concern basis should suffice. This is illustrated in Appendix 1 to this publication. Where the review period for going concern has been limited to a period less of than 12 months from the date of approval of the half-yearly financial report, the FRC guidance requires disclosure of that fact and the directors' justification for not complying with the guidance in this respect. |

A half-yearly financial report should cover the first six months of the financial year. It should contain, as a minimum, a condensed set of financial statements, an IMR and a responsibility statement, each of which is discussed in further detail below.

Timing of half-yearly reporting and dissemination of information

The half-yearly financial report must be published within two calendar months of the end of the six-month period and disseminated in unedited full text (including the auditor's review report where applicable) via RIS2. The UKLA has clarified this requirement, noting that inclusion of required information on a company's website but not in a RIS announcement is not considered to fulfil the requirements of the DTR3.

Further clarification was offered in March 2009, with the UKLA making clear that a link to a PDF is not considered an acceptable method of disseminating regulated information4. The announcement relating to the publication of the half-yearly report must also include an indication of which website the document is available on.

Interim management report

The IMR is the narrative report which includes, as a minimum:

- an indication of important events that have occurred during the first six months of the financial year and their impact on the condensed financial statements;

- a description of the principal risks and uncertainties for the remaining six months of the financial year; and

- information on related party transactions.

Principal risks and uncertainties in half-yearly financial reportsThe UKLA has given further guidance5 on the extent of disclosure of principal risks and uncertainties expected to be included in half-yearly financial reports. In particular, where those risks are deemed to be consistent with those disclosed in the previous annual report, it is acceptable for a company to:

Where risks and uncertainties have changed since the annual report, a full description of the new principal risks and uncertainties should be given. |

The following information on related party transactions should be disclosed in the IMR:

- related party transactions that have taken place in the first six months of the financial year which had a material effect on the financial position or performance of the company/group; and

- any changes in the related party transactions described in the latest annual report which could have a material effect on the financial position or performance of the company/group in the first six months of the financial year.

There is, perhaps, a lack of clarity around the latter requirement. There may be few instances of a change in a previously reported related party transaction which would not in itself be a new transaction (and therefore already be disclosed under the first point above). An example of such a situation may be sales made to a related party in the previous financial year where the absence of these in the current period has had a material impact on the group's financial performance. Given this apparent ambiguity, it may be advisable for companies either to give comparative information from the last annual report for any material related party transactions or to state explicitly that no such changes have occurred.

Companies not preparing consolidated AccountsIn respect of related parties, companies subject to DTR 4.2 that are not preparing consolidated accounts could be reporting under an accounting framework other than IFRSs. To address the possibility of such a framework lacking guidance on the nature of related party disclosures, DTR 4.2.8R(2) requires companies not preparing consolidated accounts to also disclose the following as a minimum:

if those related party transactions are material and if they have not been carried out under normal market conditions, i.e. at arm's length. The information disclosed may be aggregated according to the nature of the transactions, unless separate disclosure is necessary for an understanding of the financial position of the company. |

Responsibility statement

All companies must provide a responsibility statement in their half-yearly financial report. Such a statement must be made by the persons responsible within the company (usually the board of directors). The responsibility statement should include the name and function of any person making a statement. One or more people are expected physically to sign the responsibility statement, usually on behalf of the board of directors. Each company decides who is considered responsible for the report.

Each person making a responsibility statement must confirm that to the best of his or her knowledge:

- the condensed set of financial statements, which has been prepared in accordance with the applicable set of accounting standards, gives a true and fair view of the assets, liabilities, financial position and profit or loss of the company or the undertakings included in the consolidation as a whole;

- the interim management report includes a fair review of the information required (i.e. an indication of important events and their impact and description of principal risks and uncertainties for the remaining six months of the financial year); and

- the interim management report includes a fair review of the

information required on related party transactions.

|

"True and fair" in half-yearly financial reports The requirement to confirm that the condensed set of financial statements gives a true and fair view will be satisfied if the responsibility statement includes a confirmation that the condensed financial statements have been prepared in accordance with:

In all such cases, the person making the statement must have reasonable grounds to be satisfied that the condensed set of financial statements, prepared in accordance with such a standard, is not misleading. |

Condensed set of financial statements

UK companies preparing consolidated or single company financial statements under IFRSs should prepare their half-yearly condensed set of financial statements in accordance with IAS 34 'Interim Financial Reporting'7. An illustrative half-yearly financial report in accordance with IAS 34 and the DTR is included in Appendix 1 and a disclosure checklist containing all the requirements is in Appendix 2 to this publication.

Condensed half-yearly financial statements should normally be based on accounting policies and presentation that are consistent with those in the latest published annual financial statements.

Where the accounting policies or presentation are to be changed in the subsequent annual financial statements, the new accounting policies or presentation should be followed in the half-yearly condensed financial statements. Such changes, and the reason for these, must be disclosed in the condensed half-yearly financial statements.

If the condensed set of financial statements has been audited or reviewed in line with Auditing Practices Board (APB) guidance, the audit report or review report must, under the DTR, be included in the half-yearly financial report in full. If no audit or review has been performed, the condensed set of financial statements must include a statement to this effect.

Changes to half-yearly financial reporting in 2012 and beyondCompanies reporting under IFRSs have relatively few changes to contend with in 2012. Half-yearly reporters should consider the impact, if any, of amendments to IAS 12 Income Taxes effective for periods beginning on or after 1 January 2012. IAS 12 requires an entity to measure the deferred tax relating to an asset depending on whether the entity expects to recover the carrying amount of the asset through use or sale. The amendments introduce a rebuttable presumption that for investment properties carried at fair value the carrying value will be recovered entirely through sale. At the time of writing, EU endorsement of these amendments was expected in the third quarter of 2012. A more notable change, although only effective for periods beginning on or after 1 July 2012, arises from amendments to IAS 1 and consequential amendments to IAS 34. These amendments require items of other comprehensive income, and the associated tax, to be grouped into those that will and will not be reclassified to profit or loss. New terminology is also introduced in the form of a 'statement of profit or loss and other comprehensive income' and a 'statement of profit or loss', although their use is optional and entities may retain more familiar titles. At the time of writing, EU endorsement of these amendments was expected in the second quarter of 2012. Amendments to IFRS 1, effective for periods beginning on or after 1 July 2011, are due to be endorsed in the third quarter of 2012. Amendments to IFRS 7, also effective for periods commencing on or after 1 July 2011, have been endorsed. Looking further ahead, on adoption of IFRS 13 Fair Value Measurement, which is effective for periods beginning on or after 1 January 2013, additional fair value disclosures on financial instruments will be required by IAS 34. The IASB's Exposure Drafts on Revenue and Annual Improvements also include proposals for new disclosures in interim financial statements. Amendments to IFRS 1, effective for periods beginning on or after 1 July 2011, are due to be endorsed in the third quarter of 2012. Amendments to IFRS 7, also effective for periods commencing on or after 1 July 2011, have been endorsed. If a change in accounting policy is adopted based on a new or amended Standard or Interpretation that has not been endorsed at the end of the interim period but is expected to be endorsed by the date of approval of the next annual report, it would be advisable to include a statement to that effect in the interim financial report. |

Half-yearly financial reports under UK GAAP

UK single companies which continue to report under UK GAAP should follow the ASB statement 'Half-yearly financial reports'. The DTR requirements for non-IAS 34 condensed financial statements8 are set out below.

Minimum content of non-IAS 34 condensed financial statementsThe condensed set of financial statements should include at least a condensed balance sheet, a condensed profit and loss account and explanatory notes on these condensed financial statements. The condensed balance sheet and the condensed profit and loss account should:

The half-yearly financial information contained in the condensed financial statements must include comparatives as follows:

Although not explicitly required by the DTR, the condensed financial statements should also include a statement of total recognised gains and losses and a cash flow statement with their respective comparatives to comply with the ASB statement. In terms of comparative information, the ASB statement goes further than the DTR and IAS 34, requiring comparatives for the corresponding half-yearly period and the previous full financial year for each of the profit and loss account, statement of total recognised gains and losses and cash flow statement. The explanatory notes in the condensed financial statements should contain sufficient information to enable a user to compare the condensed half-yearly financial statements with the annual financial statements. Also, sufficient information and explanations should be included to aid the understanding of any material changes in amounts and any developments in the half-year. |

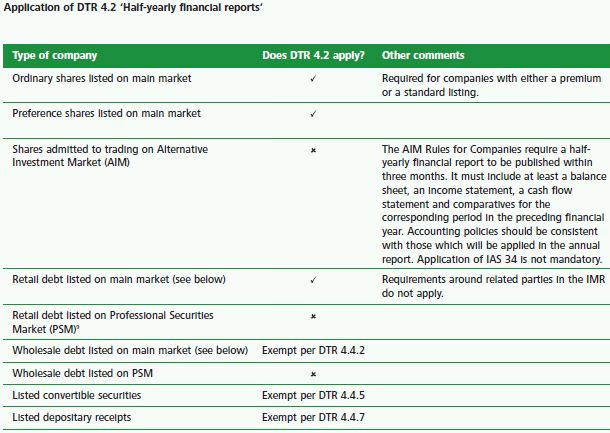

Summary of application

The DTR 4.2 requirements outlined above apply in full to companies with shares listed on a regulated market. Other companies may also be required to follow these requirements. A summary of the application of DTR 4.2 and the AIM Rules for Companies is provided in the table opposite.

Retail and wholesale debt listed on the main marketFrom 1 July 2012 the threshold for categorising debt as wholesale will be increased from denominations of €50,000 to €100,000 (or an equivalent amount). From this date, issuers of debt listed on the main market with a denomination per unit of less than €100,000 (i.e. retail debt) will be required to apply DTR 4.2, whereas those with denominations of at least €100,000 (i.e. wholesale debt) will continue to be exempted by DTR 4.4.2. Transitional provisions will apply as follows:

Both of these transitional exemptions will be lost if debt is issued that breaches the relevant conditions (i.e. debt is issued on or after 1 January 2005 with a denomination less than €50,000, or after 31 December 2010 with a denomination between €50,000 and €100,000). |

To read this article in full, please click here.

Footnotes

1 Going concern and liquidity risk: Guidance for directors of UK companies 2009. Available at www.frc.org.uk/press/pub2141.html. Guidance on half-yearly financial reports is included in paragraphs 47-50 and 86-88.

2 RIS = Regulated Information Service

3 UKLA Technical note: Disclosure and Transparency Rules

4 UKLA Publications Update – March 2009

5 UKLA Technical Note: Disclosure and Transparency Rules

6 As revised and issued by the ASB in July 2007

7 Companies may choose to prepare full financial statements in accordance with IFRSs. However, this is not common UK practice.

9 The PSM is a non- regulated market for listed debt of any denomination. It is Listed for the purpose of the Listing Rules.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.