摘要:2018年,国际投资争端解决中心(ICSID)新案数量再创新高,外国投资者与东道国的投资争端凸显。与此同时,一带一路建设推进之下,中国海外投资展现出前所未有的广度和深度。相比较改革开放前四十年以吸引外资为主,此后中国的全球投资者角色将日益突出。历史的转身之下,投资者海外投资期待获得充分地投资保护、跨境法律服务队伍需要紧跟提升服务保障水平、国家需要迭代完善相应的双边、多边投资协定。国际投资争端中,投资者的所谓投资行为是否属于相关投资法的"涵盖投资",是一个重要的、首当其冲的问题。本文就国际投资认定的实体法渊源、国际投资的概念及文本定义、国际投资认定的仲裁实践等方面展开阐述,展现对"国际投资认定"全面理解场景。

关键词:国际投资争端、ICSID、BIT、投资认定、仲裁实践

2018年7月26日,ICSID仲裁庭对Georg Gavrilovic and Gavrilovic d.o.o. v. Republic of Croatia (ICSID Case No. ARB/12/39)作出裁决。案件历时5年8个月的时间,仲裁庭对争端的诸多方面作出裁断。其中一个最为主要的争议方面,即为Georg Gavrilovic和Gavrilovic d.o.o.两原告是否进行了BIT(Croatia- Austria 1997)和ICSID公约所保护的"投资"。裁决中,仲裁庭对被告方(克罗地亚)援引的"Salini Test"进行了否定,支持了原告方的投资主张。此案一出,国际投资争端中的投资认定问题再次引起广泛关注。

一、何为投资认定

投资可以是一个经济的概念、国内的概念,但是在国际投资实践中、在投资者与东道国之间发生争端后诉诸投资者--东道国争端解决机制(主要是投资仲裁)语境下,"投资"是一个特定的国际法概念,有特定的定义,以及相应的内涵和外延。更为重要的是,"投资"的认定是关乎东道国、投资者母国、投资者切身利益,因此也是国际组织、投资争端仲裁庭(仲裁员)、律师需要谨慎应对的一个问题。"投资"的范围,影响到东道国承担国际义务的范围,"涵盖投资" 1范围越广,东道国承担的对于投资者、投资者母国的国际义务越广。投资者进行的经济活动是否属于"涵盖投资",直接意味着其权益是否获得相关国际投资法的保障,其利益遭遇损害时投资者是否可以诉诸相关争端解决机制进行维权。投资争端仲裁庭(仲裁员),更是在争端解决程序中直接基于"投资"认定结论做出是否具备管辖权的裁定。因此,国际投资争端中,投资者的所谓投资行为是否属于相关投资法的"涵盖投资",是一个重要的、首当其冲的问题。

二、国际投资认定的实体法

这里涉及一个更加上位的范畴,国际投资法的渊源。举例来说明,2017年6月21日立案的德国企业Hela Schwarz GmbH 在ICSID诉中国案2,后续的案件处理的主要法律依据是什么?

首先,德国投资者在中国境内进行的投资,中国外商投资相关法律法规要遵守。

其次,中国与德国1983年10月7日签署双边投资协定(1985年3月18日生效),其后两国于2003年12月1日重新签署双边投资协定,并于2005年11月11日生效。双边投资协定一方的公司或公民,在另一缔约国的投资相关事项,受双边投资协定约束。中国需要按照双边投资协定约定的范围和标准给予德国投资者以投资保护,中国也籍此吸引投资者进行投资。

再次,中国和德国,都是《关于解决国家和他国国民之间投资争端公约》(即"华盛顿公约")的缔约国,德国投资者与东道国中国之间的争端,即有了提交国际投资争端解决中心(简称ICSID)进行仲裁的可能。

由此看来,东道国涉外投资法(national law)、双边投资协定(BIT,或者是贸易协定中的投资条款)、条约公约等,成为了投资者与东道国间国际投资争端中涉及的国际投资法的主要渊源。下一节,我们将从这几个法律渊源的文本中去挖掘国际投资的概念和定义。

也有观点认为,与国际投资争端直接相关的主要法律渊源有四类,除了双边(多边)投资协定、东道国法律、国际公法之外,还有相关方达成合意的规则或合约条款。 3

在进入下一节之前,有几个相关事项在此做一个交代:

1.仲裁规则均认同当事人选择适用法(applicablelaw)解决其纠纷的意思自治。这是考虑适用法时的一个重要规则,也是对前述法律渊源问题的一个重要补充。

2.随着双边(多边)投资协定的蓬勃发展,其在投资者与东道国投资争端解决中的地位越来越重要,被援引越来越频繁。从东道国的国际义务来讲,其相关国内法的制定、完善,是一个协定规则国内立法化的过程。投资协定规则的发展,对国内法有一个引领作用。

3.不同的双边(多边)投资协定所设定的争端解决机制是有差异的、多元可选的;特定的双边(多边)投资协定设定通过仲裁解决纠纷,诉诸的机构和程序也是多元可选的。

比如,中国与德国BIT:

Article 9 Settlement of Disputes between Investors and one Contracting Party

......

(2) If the dispute cannot be settled within six months of the date when it has been raised by one of the parties in dispute, it shall, at the request of the investor of theother Contracting State, be submitted for arbitration.

(3) The dispute shall be submitted for arbitration under the Convention of 18 March 1965 on the Settlement of Investment Disputes between States and Nationals of Other States(ICSID), unless the parties in dispute agree on an ad-hoc arbitraltribunal to be established under the Arbitration Rules of the United Nations Commission on the International Trade Law (UNCITRAL) or other arbitration rules.

......

Article9(3)约定:除非双方约定按照联合国贸法会仲裁规则设立仲裁庭进行仲裁,或据其他仲裁规则进行仲裁,争议提交ICSID仲裁。

所以,即便投资争端可以诉诸ICSID仲裁,最终是否诉诸ICSID、或是选择依据其他仲裁规则进行仲裁,当事人具有相当的自治。

三、国际投资的概念及定义

在ICSID仲裁中,什么构成投资主要在两个法律渊源下进行考量:(1)、投资协定;(2)、《华盛顿公约》第25条。 4(同理,在非ICSID仲裁中,针对适用实体法逐一核对。)

笔者认为,没有将东道国相关国内法作为重要考量对象的原因之一,即为前文所述:从东道国的国际义务来讲,其相关国内法的制定、完善,是一个协定规则国内立法化的过程。投资协定规则的发展,对国内法有一个引领作用。当然,作为被告方的东道国,完全可以援引国内法对"投资"提出抗辩。

(一)《华盛顿公约》对投资的定义

Article 25

(1) The jurisdiction of the Centreshall extend to any legal dispute arising directly out of aninvestment, between a Contracting State (or any constituent subdivision or agency of a Contracting State designated to the Centreby that State) and a national of another Contracting State, which the parties to the dispute consent in writing to submit to the Centre.When the parties have given their consent, no party may withdraw itsconsent unilaterally.

......

第25条位于《华盛顿公约》第二章管辖首条。第25条将ICSID管辖的范围仅限于直接产生于投资的法律争端(legaldispute arising directly out of aninvestment),但公约对投资(investment)这个核心概念并没有给出定义。 5

在对投资(investment)无任何阐述下,公约赋予当事人充分的自由裁量,公约将何谓投资这个问题,留给了当事人商定合意,以及仲裁庭的最终辨析认定。 6当事人的商定合意,既可以是投资协定的形式,也可以是特许协议的形式。

所以,下文我们进一步讨论投资协定对投资的定义,并在第四节讨论相关的仲裁实践。

(二)投资协定对投资的定义

1.开放式定义--早期BITs的普遍模式

早期的BITs,比较明显地表现出,缔约一方侧重于吸引外资促进本国经济发展和缔约另一方侧重于保护本国海外投资利益,所以在涵盖投资的范围上采取了比较开放的宽泛标准。

比如,中国与德国BIT第一条约定:

the term"investment"means every kind of asset invested directly or indirectly by investors of one Contracting Party in the territory of the other Contracting Party, and in particular, though not exclusively,includes:

(a) movable and immovable property and other property rights such as mortgages and pledges;

(b) shares,debentures,stockand any other kind of interest in companies;

(c) claims to money or to any other performance having an economic value associated with an investment;

(d) intellectual property rights, inparticular copyrights, patents and industrial designs, trade-marks,trade-names, technical processes, trade and business secrets,know-how and good-will;

(e)business concessions conferred by law or under contract permitted by law, including concessions to search for, cultivate, extract or exploit natural resources; any change in the form in which assets are invested does not affect their character as investments.

以上条约文本中的"every kind of asset"、"directly or indirectly"、"not exclusively,includes"等措辞,是资本输入国最大限度吸引外资、资本输出国最大限度保护对外投资的缔约意图在协调统一后的体现。

2.封闭式定义--北美自由贸易协定(NAFTA)对投资定义

宽泛和开放的投资定义是一把双刃剑,它给予投资者以信心而促进跨国投资,同时也给东道国带来不合理的投资法义务负担,以及东道国在经济主权和市场监管等方面作出的权力减损。在投资定义的明确清晰方面,北美自由贸易协定(NAFTA)做了有益的尝试。

NAFTA Article 1139

investment means:

(a) an enterprise;

(b) an equity security of an enterprise;

(c) a debt security of an enterprise

(i) where the enterprise is anaffiliate of the investor, or

(ii) where the original maturity of the debt security is at least three years,

but does not include a debt security,regardless of original maturity, of a state enterprise;

(d) a loan to an enterprise

(i) where the enterprise is an affiliate of the investor, or

(ii) where the original maturity of the loan is at least three years,

but does not include a loan,regardless of original maturity, to a state enterprise;

(e) an interest in an enterprise that entitles the owner to share in income or profits of the enterprise;

(f) an interest in an enterprise that entitles the owner to share in the assets of that enterprise on dissolution, other than a debt security or a loan excluded from subparagraph (c) or (d);

(g) real estate or other property,tangible or intangible, acquired in the expectation or used for the purpose of economic benefit or other business purposes; and

(h) interests arising from the commitment of capital or other resources in the territory of a Party to economic activity in such territory, such as under

(i) contracts involving the presenceof an investor's property in the territory of the Party, includingturnkey or construction contracts, or concessions, or

(ii) contracts where remuneration depends substantially on the production, revenues or profits of an enterprise;

but investment does not mean,

(i) claims to money that arise solely from

(i) commercial contracts for the sale of goods or services by a national or enterprise in the territory of a Party to an enterprise in the territory of another Party, or

(ii) the extension of credit in connection with a commercial transaction,such as trade financing, other than a loan covered by subparagraph(d); or

(j) any other claims to money,

that do not involve the kinds of interests set out in subparagraphs (a) through (h).

以上条文中用"means"代替了先前协定所通常采用的"includes",使得随后的列举成为"穷尽式"、"排他式"。尽管,随后的列举名目丰富、且文意本身也具有相当的弹性。但是从开放式概念转化为封闭式概念确实是有益的尝试,从特定角度来看,是实质性的发展。

3.综合式定义--美国2012年BIT范本

美国BIT范本经历了1983年版、1984年版、1987年版、1991年版、1992年版、1994年版、2004版年,以及2012年版等,多次迭代发展。"投资特征(characteristicsof an investment)要求"和"注释修正"是2004年版本以及后期范本的突出特征。其后,美国也基于新版本范本签署了BIT。

2013年7月中美重启BIT谈判工作,美国2012年版BIT范本是中美谈判的美方文本依据。美国2012年版BIT范本,包含了美方对历次中美BIT谈判的焦点和分歧问题的回应,其中对投资定义的限定,是中方应对美方滥用投资自由化要求的有力措施。当然,这是从资本输入国角度所做的一种评价。

2012 U.S. Model BIT Article1

"investment" means every asset that an investor owns or controls, directly orindirectly, that has the characteristics of an investment, including such characteristics as the commitment of capital or other resources, the expectation of gain or profit, or the assumption of risk. Forms that an investment may take include:

(a) an enterprise;

(b) shares, stock, and other forms of equity participation in an enterprise;

(c) bonds, debentures, other debt instruments, and loans;

(d) futures, options, and other derivatives;

(e) turnkey, construction,management, production, concession, revenue-sharing, and other similar contracts;

(f) intellectual property rights;

(g) licenses, authorizations,permits, and similar rights conferred pursuant to domestic law;and

(h) other tangible or intangible,movable or immovable property, and related property rights, such asleases, mortgages, liens, and pledges.

范本还在该条下列注释如下:

1.Some forms of debt, such as bonds,debentures, and long-term notes, are more likely to have the characteristics of an investment, while other forms of debt, such asclaims to payment that are immediately due and result from the saleof goods or services, are less likely to have such characteristics.

2.Whether a particular type of license, authorization, permit, or similar instrument (including aconcession, to the extent that it has the nature of such aninstrument) has the characteristics of an investment depends on such factors as the nature and extent of the rights that the holder has under the law of the Party. Among the licenses, authorizations,permits, and similar instruments that do not have the characteristics of an investment are those that do not create any rights protected under domestic law. For greater certainty, the foregoing is without prejudice to whether any asset associated with the license,authorization, permit, or similar instrument has the characteristics of an investment.

3.The term "investment" does not include an order or judgment entered in a judicial or administrative action.

以上条文的基本逻辑是:第一,列举是非排他性的;第二,投资特征要求是统领性规定;第三,即便在列举名目之内,几类很明显的非投资,注释予以明确除外;第四,除了条文已经明确的投资和非投资,条文本身构成一案一议的标准、为判断是否构成涵盖投资提供了指引。

相比前述北美自由贸易协定(NAFTA)对投资定义这类封闭式定义,美国2012年BIT范本的在投资特征要求介入之下的回归开放性定义,可谓投资定义缔约实践的又一次发展。

4.更多重要细节

前文所述开放式、封闭式、综合式,是投资协定对投资进行定义的模式之分。在模式之下,还有其他较多的细节方面,亦同等重要。如,投资定义有基于财产(asset)的定义和基于企业(enterprise)的定义之分,将在权益内容、国内法的适用、控诉主体等方面形成较大差异。又如,"ownsor controls"的要求,到底是要拥有多少数量、或是达成何种控制?才成为成立投资与否的分水岭。再如,"(ownsor controls,)directlyor indirectly",其中允许的间接,是否给予了多层级投资结构(母公司、子公司、孙公司等直接)无限的规划空间等。

5.我国缔结BITs中投资定义的总体情况

我国目前对外缔结145个双边投资协定(BITs) 7,各协定中对投资的定义文本整体上较为一贯、稳定。我国双边投资协定文本,对投资采取较为宽泛的接纳态度,采取基于财产(asset)的定义,并进行非穷尽式的列举,不另行增加"投资特征"要求。 8

四、投资者与东道国争端中投资认定的仲裁实践

投资仲裁过程中,仲裁庭需要尽量考虑以往仲裁庭对相关事项的裁定意见。但是,这种考量并没有上升到判例法的高度,仲裁庭没有跟随先例仲裁庭决定的义务,更没有据此得出特定结论的责任。甚至除非争端方主张,仲裁庭也没有查阅、研习特定先例的义务。 9这是我们展开讨论"投资认定"仲裁实践前,需要澄清的一个问题。即便如此,先例依然意义重大。仲裁各方,包括仲裁庭在内,都时常选择援引案例来佐证自己的主张和说理。

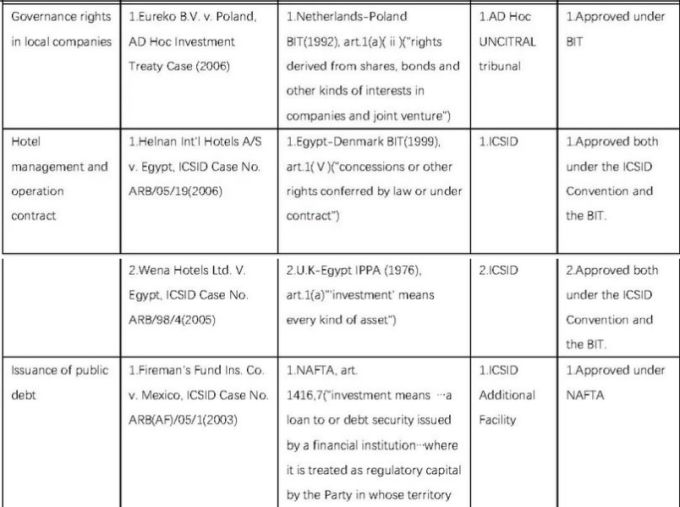

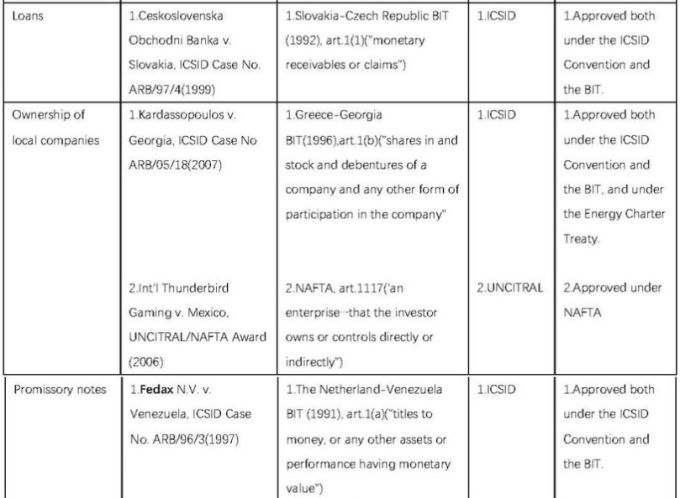

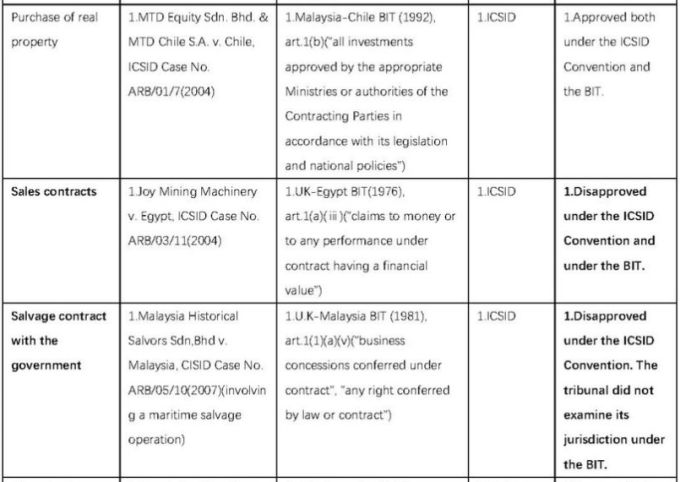

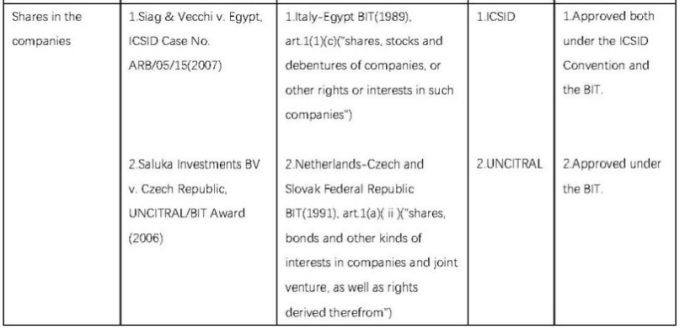

(一)涵盖投资认定的仲裁实践

以下表格10,罗列不同类型的经济活动在ICSID或UNCITRAL等仲裁规则下,被考量是否属于涵盖投资。表内注明了案涉协定及协定对投资的定义措辞,在上一节介绍的投资协定的投资定义模式的基础上,再结合表内具体措辞,投资认定的梳理可得以进一步具体。

其中,Patrick Mitchell v. Democratic Republic Congo, ICSID Case No. ARB/99/7(2006)、Joy Mining Machinery v. Egypt, ICSID Case No. ARB/03/11(2004)、MalaysiaHistorical Salvors Sdn,Bhd v. Malaysia, CISID Case No.ARB/05/10(2007)等案件,仲裁庭均裁定相关经济活动不属于涵盖投资。这些否定性案例在投资认定问题的分析上具有特别参考意义。

在Mitchell案件中,被告方主张原告方的律师事务所(lawfirm)对其本国经济无重要性(贡献),因此也无法成立为涵盖投资。仲裁庭驳回了被告方的这个主张,认为Mr.Mitchell的动产、文件、技术、商誉等使其律师事务所经营活动成立涵盖投资。而在其后的撤销仲裁裁决程序中,委员会得出相反的结论:对东道国经济增长的贡献是构成涵盖投资的重要方面,Mr.Mitchell的律师事务所不构成ICSID定义的投资。

在JoyMining案件中,否定的结论很难简单从案涉协定的定义文本分析中得出,定义措辞简单列举如下:UK-EgyptBIT(1976), art.1(a)(ⅲ)("claims to money or to any performanceunder contract having a financialvalue")。仲裁庭分析后认为,案涉交易仅仅成立销售合同,销售合同是明显区别于BIT和ICSID要保护的投资的。仲裁庭在分析过程中采用了在投资仲裁实践中形成的Salini规则。

在Salvors案件中,独任仲裁员与(仲裁裁决撤销程序)委员会,一前一后作出了两个相反的判断。尽管裁决其后被撤销,独任仲裁员在案件中也是援引Salini标准作出了案涉船舶打捞合同不属于ICSID公约第25条所定义的投资的裁决。

(二)涵盖投资认定仲裁实践的有益成果

《华盛顿公约》制定过程中,关于涵盖投资的定义存在很多不同的看法、且彼此争议分歧较多,直至公约缔结生效,都没有就此问题达成一致意见,这或许是公约本身并未直接给出投资定义的原因之一。其后的仲裁实践,无疑是进一步推进和深化了相关问题的争论、辨析和反思。更有一些标杆性的案例,梳理和建立了所谓的判定投资的标准,如前面提到的Salini标准,就是在案件SaliniConstrutorri S.p.A & Italstrade S.p.A. v. Morocco,(ICSIDCase No.ARB/00/4)中确立的,且其后有很多追随案例。也有恰恰相反的标杆性案例,解构和否定所谓的判定投资的标准,如案件BiwaterGauff (Tanzania) Ltd. v. United Republic of Tanzania (ICSID Case No.ARB/05/22),就对Salini标准提出了质疑,指出其问题并拒绝采取这样的标准直接作出投资认定。

如此众说纷坛的仲裁实践,客观上为BITs的缔约方提供了很好的完善指引。比如,前述介绍的投资协定的投资定义模式,美国引入"投资特征"的选择一定程度受益于案例的启示。另外,毫无疑问,我国的国际投资者也能够在历史案例中找到更好的投资规划思路和纠纷维权方案。

Footnote

参考文献:

1 "涵盖投资",建议读者在实体法规定和争端裁决判定两个方面去理解,前者为国际投资法文本规定指向的经济行为(或资产、或权利等),后者为个案中基于对国际投资法的解读而做出的判定结论。虽然,理想化的情况是,静态的法的规定和动态法的应用是一致和协调的。本文第三节投资的概念及定义,主要论述实体法规定;第四节投资者东道国争端仲裁实践中的投资认定主要论述争端裁决判定的实践,以及衍生出来的规则或理论。

2 案件索引:HelaSchwarz GmbH v. People's Republic of China, ICSID Case No. ARB/17/19

3 See Christopher F. Dugan, Don Wallace, Jr., Noah D. Rubins, BorzuSabahi , Investor-State Arbitration,198 Madison Avenue, NewYork,New York10016,OxfordUniversity Press, 08 March 2012,P.20

4 See Campbell McLachlan, Laurence Shore, Matthew Weiniger,International Investment Arbitration Substantive Principles, 198Madison Avenue, New York,NewYork 10016,OxfordUniversity Press, 07 September 2017,P.217

5 但值得注意的是,这并不意味着《华盛顿公约》本身对投资认定问题是毫无边界的,这点在文内部分案例中有所体现。

6 See Campbell McLachlan, Laurence Shore, Matthew Weiniger,International Investment Arbitration Substantive Principles, 198Madison Avenue, New York,NewYork 10016,OxfordUniversity Press, 07 September 2017,P.218

7 数据采集自http://investmentpolicyhub.unctad.org 。

8 在是否要求"投资特征"上,中国2003年与德国双边投资协定是个例外,该BIT文本提出了三项"投资特征"要求,即"lastingeconomic relations","connectionwith an enterprise","effectiveinfluence in management"。

9 See Catherine A. Rogers, Roger P. Alford, The Future of InvestmentArbitration, 198 Madison Avenue, New York,NewYork 10016,OxfordUniversity Press, 2009,P.67

10 See Christopher F. Dugan, Don Wallace, Jr., Noah D. Rubins, BorzuSabahi , Investor-State Arbitration,198 Madison Avenue, NewYork,New York10016,OxfordUniversity Press, 08 March 2012,P.26

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.