This is the sixth installment in our periodic series on National Instrument 43-101.

One of the most important public documents produced by a mining issuer in Canada is the "technical report." A technical report must be filed by both private and public companies for material mineral projects when "triggered" by National Instrument 43-101 Standards of Disclosure for Mineral Projects (NI 43-101). Therefore, it is very important for every mining issuer to be aware of these triggers, so as to not trigger a technical report when it is not in a position to file a technical report prepared in accordance with NI 43-101.

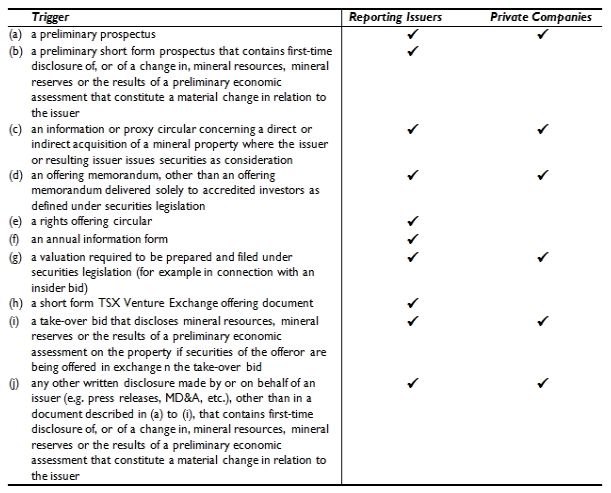

Technical Report Triggers. Upon becoming a reporting issuer in a jurisdiction of Canada, a mining issuer must prepare, and file on the System for Electronic Document Analysis and Retrieval (SEDAR), a technical report for each of its material mineral projects. While this is typically the first technical report for a mining issuer, there are triggers for potential updated or new reports resulting from a mining issuer making disclosures, some of which also apply to private companies. A "current and complete" technical report is required to be prepared and filed at the same time (or shortly after) as a mining issuer makes the following disclosures to the public containing scientific or technical information regarding a material mineral project.

Key Qualification – No Material Change. Triggers (b) and (j) above are qualified in that a new technical report is required only if a company makes a first-time disclosure of, or of a change in, mineral resources, mineral reserves or the results of a preliminary economic assessment and it constitutes a material change in relation to the issuer. If there are no changes to any of these items (or no new disclosure), a technical report would not be required even if the existing relevant report is not current and complete. However, if there is a first time disclosure or a change to any of these items, the issuer must then consider whether the change constitutes a "material change" to the issuer. If the change is a "material change" to the issuer, it will trigger a new technical report. However, if the change is not a "material change" to the issuer but is instead a "material fact", it will only have to be disclosed in a press release and a new technical report will not be required at that time. A "material change," as defined by applicable securities legislations and stock exchange requirements, is generally based on a market impact test where a change that significantly affects or would reasonably be expected to have a significant effect on the market price or value of a company's securities is material. In making materiality judgments, issuers are encouraged to consider a number of factors and the context and circumstances - materiality cannot be captured in a simple bright-line standard or test - including the nature of the information itself, the volatility of the company's securities, and prevailing market conditions.

Key Qualification – No New Material Information Since Last Report. Where an issuer thinks it may have triggered the requirement to file a technical report because of changes and updates to the information regarding its material mineral project, it is possible to rely on a previously filed technical report if it supports the scientific or technical information in the new trigger document, at the date of filing the new trigger document there is no new material scientific or technical information concerning the subject property not included in the previously filed technical report, and the previously filed technical report meets any independence requirements. Items that could affect the currency and completeness of a technical report could, among other things, relate to:

- changes to metal prices

- out of date economic analyses (including mine life, net present value and internal rate of return)

- reinterpretations of the deposit

- reserve and resource estimate updates

- changes to mineral titles, permits or obligations

- changes in mining method

- changes in tax or royalty regime

- new drill results

- new assay results or metallurgic test work

- changes in time frame for development

Individually and in the aggregate, all factors that have changed since the last filed technical report need to be considered to determine whether such changes are material to the property and thus prevent reliance on the qualification that there is no new material information since the last report. Economic analyses in technical reports are based on a number of assumptions and factors and as a result can quickly become outdated as those assumptions and factors depart from reality. It is recommended that an issuer consider ways to extend the life of a technical report by, for example, having a qualified person include sensitivity analyses of the key economic variables.

Now or Later? Not all triggers are created equal with respect to when a technical report must be filed. While most are hard triggers (i.e., the documents described in (a) to (i) above) that require the filing of the technical report not later than the time of the release of the document that contained the trigger, documents described in (j) result in a soft trigger that provides an issuer with additional time to file the report. For instance, if a press release or MD&A is disseminated by an issuer and such document contains new material scientific or technical information, the issuer has 45 days to file the technical report. This delayed filing is subject to accelerated timing if one of the other triggers occurs during this 45 day period, such as the filing of a preliminary prospectus or a directors' circular, in which case the technical report would need to be filed immediately on such later trigger. In addition, if a property becomes material to an issuer less than 30 days before the filing deadline of an annual information form, the issuer will have 45 days in order to complete and file the related technical report.

Who Prepares The Report? A technical report must be prepared by a "qualified person," who may be independent of the issuer (and may be required to be so) or may be an employee of the issuer. In any case, it is the responsibility of the qualified person to determine the materiality of the scientific and technical information to be included in the technical report. In certain cases, the technical report needs to be prepared by an independent qualified person. The technical report prepared upon becoming a reporting issuer must be prepared by an independent qualified person. In addition, technical reports required under (a) and (g) above must be prepared by an independent qualified person. Further, a report must be prepared by an independent qualified person if the disclosure document discloses: (i) for the first time mineral resources, mineral reserves or the results of a preliminary economic assessment on a property material to the issuer, or (ii) a 100 percent or greater change in the total mineral resources or total mineral reserves on a property material to the issuer, since the issuer's most recently filed independent technical report in respect of the property. However, if the issuer is a "producing issuer" an independent report is generally not required. A "producing issuer" is an issuer with annual audited financial statements that disclose (a) gross revenue, derived from mining operations, of at least $30 million Canadian for the issuer's most recently completed financial year; and (b) gross revenue, derived from mining operations, of at least $90 million Canadian in the aggregate for the issuer's three most recently completed financial year.

Conclusion. Overall, it is very important that issuers take the above considerations into account prior to making any disclosure to the public so as to not inadvertently trigger a technical report if the issuer is not ready to file the report on SEDAR in accordance with the timing requirements of NI 43-101. Compliance is simply a matter of coordinating the timing the disclosure with the timing for a technical report if it is expected that a new report will be triggered, to the extent legally possible, or if information is not expected to be able to be held back, ensuring that the appropriate qualified persons begin work on a technical report as early as possible.

The authors of this article gratefully acknowledge the contributions of summer law student Jasmine Qin.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.