In brief - The Australian Government has released for consultation the first tranche of the Bill and explanatory materials for the corporate collective investment vehicle (CCIV)

This represents a major step forward for the introduction of the CCIV, which could be on track for a start in (late) 2018. In 2017 and early 2018 Australian Treasury issued consultation papers for a CCIV.

- The CCIV is a worthy step towards increasing the export of Australian funds management services and products. The right regulatory and tax settings are necessary to fulfil this intention.

- The CCIV could be seen as the next Australian financial animal, with a koala fund alongside a kangaroo bond!

What is the international competition?

Europe, the UK and Ireland have the lead with long established and well used corporate investment vehicles.

Within the Asia Paciifc region, Hong Kong and Singapore are both proposing to introduce a corporate investment vehicle or opened ended fund company structure. Other economies in the region may follow the trend.

What about the managed investment scheme?

Implementation of a CCIV will be an addition to the managed investment scheme framework. The managed investment scheme is the dominant domestic fund model. Given the modular flexibility and insolvency protection likely from a CCIV, it may be that we see a gradual favouring of CCIVs over managed investment schemes as the market becomes more familiar with them.

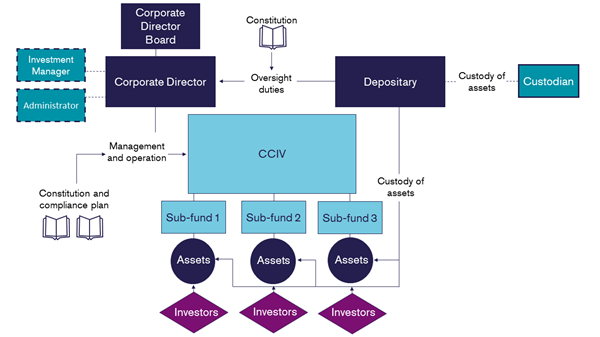

What is the proposed CCIV structure?

Ideally the CCIV will be internationally comparable, competitive and supported by the necessary tax settings. Australian Treasury has issued a draft consultation Bill and explanatory materials for the tax framework. The consultation has made a good starting point of aligning with the Attribution Managed Investment Trust (AMIT) regime.

Australian Treasury prepared the following diagram for the proposed CCIV.

Source: A copy of the original diagram is available on the Australian Treasury website under the CCIV Slides link here.

The CCIV proposes roles and functions familiar to international offerings:

- regulated structure for a corporate fund vehicle

- mandatory licensed fund manager, the corporate director

- mandatory depository, for retail funds

- sub-fund structure

- windup regime

What should industry be thinking about?

Some of the issues we suggest operators, service providers and investors consider when reviewing the CCIV arrangements are:

- Wholesale - The regulatory settings for the wholesale structure

are important

- The licensing framework is still to be proposed

- There are registration obligations for wholesale CCIVs and reduced regulatory requirements proposed in comparison to a retail CCIV.

- The registration of a CCIV as a wholesale or retail CCIV is is an important consideration as a regulated structure can attract wholesale investment. How an investor will be informed of registration of a CCIV as retail or wholesale is not clear based on the Bill. The provisions in the Bill also operate to remove obligations for wholesale CCIV, in which case achieving legal certainty of retail provisions applying for wholesale investors wanting a retail CCIV vehicle requires consideration. Certainty is available for managed investment schemes as all registered schemes must comply with the requirements in the Corporations Act 2001 for registered schemes. The CCIV arrangements for retail and wholesale CCIV may become clearer upon further tranches of the draft law becoming available, ideally a simple registry check.

- Legal standing of sub-fund - A sub-fund does not have legal standing for the provisions in the Bill. In the consultation paper a sub-fund was proposed to have legal standing in limited respects, principally for winding up of the sub-fund.

-

Where a sub-fund does not have legal standing, there is a risk that foreign jurisdictions may not recognise the segregation of sub-fund assets and liabilities. The sub-fund and cell structure is becoming common which may mitigate this.

The different regulatory settings in Australia and other jurisdictions are worth considering for this issue. Except for the Asia Region Funds Passport (Bill recently introduced to Parliament and awaiting assent), Australia does not have a prescriptive rules-based approach for funds, in particular to limit leverage and borrowing as a UCITS type framework does. A separate legal entity status may support the Australian regulatory framework.

Even with this knowledge the development internationally of a protected cell framework and not an incorporated cell framework appears to be more common.

- Compliance plan - For a retail CCIV, ASIC may direct the corporate director to modify, or repeal and replace the compliance plan.

- Company + Depository - The company structure and independent depository with asset holding and oversight functions should sit well with international investors.

- Distribution - For service providers, a change to the existing licensing and distribution obligations have not been identified, although we expect retail client protections to be consistent with those for a retail managed investment scheme.

- Transition arrangements - The ability to transition from a current licence or registered scheme is desirable. If the regulatory framework aligns then there appears to be a reasonable basis to allow for this with appropriate member consideration. Such an approach may also support use of the CCIV.

- ASIC Rules - The regulatory framework provides for ASIC to make CCIV rules for prescribed matters. This approach provides significant flexibility in the requirements that ASIC may impose or remove for a CCIV and is alike to APRA standards. The draft Bill allows for CCIV rules for asset segregation holding arrangements for assets of sub-funds, assets to not be required to be held by the depositary, property that may be considered in determining liquid assets and permitted share capital reduction circumstances. It is possible CCIV rule provisions will be proposed in further tranches.

| Hamish Ratten | Toby Blyth |

| Regulatory and financial services | |

| Colin Biggers & Paisley |

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.